Jan 10, 2015, 9:20 pm

Jan 10, 2015, 9:20 pm

Last edit by: NoonRadar

Nov 24, 2015

Dear XXXXXXXXX,

We want to let you know that we are making a change to your Target Prepaid REDcard� by American Express, and you will no longer be able to add money from your debit card at Target stores. As always, you can continue to add money to your Prepaid REDcard by using:

� Your debit card online through your Account

� Cash at a Target Store

� Direct Deposit (You can automatically add all or part of your paycheck, government benefits and federal tax refunds to your Prepaid REDcard)

DEAD FOR DEBIT CARD LOADS EFFECTIVE 10/12/2015 - MEMO: http://frequentmiler.boardingarea.co...uests-can-use/

DEAD FOR CREDIT CARD LOADS. (Amex GCs Included)

Effective May 6, 2015 registers are hard-coded to not allow credit card reload. PIN-based debit cards are working, however YMMV. PIN-based debit cards may be refused by cashiers.

WHAT IS TARGET PREPAID REDCARD?

Prepaid Redcard is a reloadable American Express card. It is only available to purchase at select Target stores.

WEBSITE:

This site may error when in Firefox, especially with adding payees / bill pay. Customer service says to use Chrome or Internet Explorer.

https://amex.serve.com/prepaidredcard

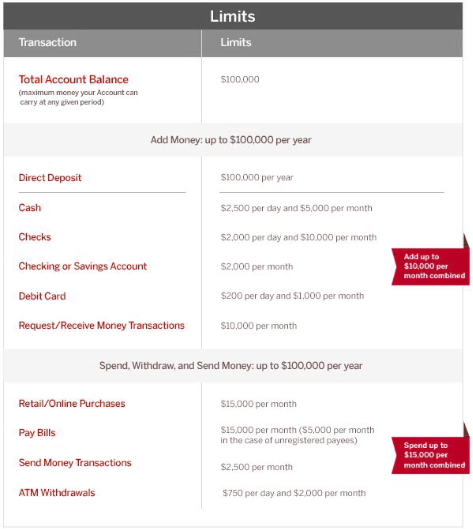

PREPAID REDCARD LOAD LIMITS

Cash (or debit card) loading at Target: ** - $1,000/transaction, $2,500/day and $5,000/month

Online Debit Card Load * - $200/day and $1,000/month

Checking/Savings Account - $2,000/month

Checks - $2,000/day and $10,000/month

ATM Withdrawals - $750/day and $2,000/month

All "Monthly" limits are per calendar month and reset on the 1st of each month.

Daily limits reset at midnight Eastern time, 9 PM Pacific time.

*For online debit load, only use of bank-issued cards is allowed. The use of pre-paid debit cards (Netspend, Paypower, Univision, Paypal, etc.) and VGC/MGC/AGCs is not allowed. Your account will be flagged upon first/second attempt.

ATM Withdrawals:

No-fee ATM usage at US Target stores* and U.S. Allpoint network ATMs. (ATM usage not available at any other ATMs.) Find an Allpoint ATM at: www.allpointnetwork.com Note that some ATMs only allow $400/transaction. There is a $750/day and $2,000/month limit to ATM withdrawals.

RedCard is only available in specific Target stores and is not available in all states. Go to this site to find a list of available locations:https://amex.serve.com/prepaidredcard

FREQUENTLY ASKED QUESTIONS

Q: Can I reload a RB at a Target that doesn't sell RB?

Yes. However, the cashier may not know how to do it. You may be able to coach them through it by saying "It's like reloading a Starbucks (or Gift) card". For step-by-step instructions on one method of 'coaching' new cashiers see Post#1904

Q: Can I buy or reload a RB in North Carolina?

See post here: http://www.flyertalk.com/forum/manuf...a-63.html#2520

There is currently a software issue preventing any reload of any kind in NC. It is a known issue but there is no ETA on a fix.

Q: Can I reload the RB at any register, or just at the Customer Service desk?

It can be done at any register, however some cashiers are not trained on how to do this and you may have to go to Customer Service.

Q: What is the most efficient way to drain a RedCard?

Use BillPay to pay bills. For example, pay the credit card you used to load RedCard with. You can also withdraw money at ATMs.

Q: I cant access the BillPay feature through the RB website!

Verify that your account information correctly reflects a 10-digit phone number (including area code). Numerous people have reported that their account only had a 7-digit phone number (no area code) and that, after updating to a 10-digit phone number, BillPay miraculously started working.

Q: Can we buy a temporary Redbird card while we still have a Bluebird or Serve account?

Yes.

Q: How many Redbird cards can you purchase at once?

You can only purchase one Redbird card a day per SSN. If you plan to purchase more than one, be sure to use a different SSN for each purchase to avoid activation issues.

Q: Can we register our temporary Redbird online while we still have a Bluebird or Serve account?

No. You will have to cancel your Bluebird or Serve account first before registering.

Q: How do I cancel my BlueBird or Serve Account online? Do I need to call them?

Frequent Miler posted a useful trick that will help you cancel online How to cancel Bluebird online This works for both BlueBird and Serve.

Q: Cancelled Bluebird, why does registering Redbird error out saying Bluebird is still active?

If you have open transactions that have not been settled, like BillPay checks that have not yet been cashed, the account cannot settle and will not be truly closed. Thus Target will reject it until it's permanently closed.

Q: Can we get Redbird online?

No. The only way to get Redbird is to find a participating Target store and buy a temporary card there. Some people have purchased RB on Ebay, Amazon, or through private deals. Be aware that doing so may violate the TOS of one or more of these services. Also be aware that buying an un-activated RB, you are potentially buying "stolen" merchandise; the seller *may* have simply taken the un-activated RB cards from a target store without permission. At best they got permission from a low-level employee; they certainly are not getting permission from someone authorized to allow sale of RB outside of the current Target-authorized roll out markets. It is highly recommended to only buy already activated Redbirds because many Targets which do not offer Redbirds also will not be able to activate them and you will spend a month with the Customer Service line trying to get a new one.

Q: Does the initial load you put in when purchasing the Redbird count against the monthly limit?

No. After registering the Redbird online, any loads done will count against your monthly limit, even on your temp card.

Q: Can we load Redbird with Target gift cards at Target?NO.

When loading, the register displays a large message saying that gift cards cannot be used to pay for this transaction.

Q: What are the card�s load limits per transaction at Target?

[B]As of 2/2/2015 there is a maximum $1,000 load per transaction. You can no longer load the same RB multiple times (multiple swipes) in 1 transaction. Likewise, you can no longer load multiple RBs (say your's and your spouse's) in 1 transaction. Maximum of 1 load, for $1,000 per debit card payment. End of story.

Q: What credit cards can I use to reload RedCard in Target stores?

NONE. As of May 6, 2015, credit cards cannot be used to reload.

Q: Can I reload with a debit card?

Yes, but only if the debit card can be authenticated with PIN-number. Signature-based debit that processes on the Visa/MasterCard/AmEx networks will NOT work.

Q: Can I reload with a prepaid debit card or Vanilla Visa?

Yes, but only if you have a PIN for that card.

Q: How can I load 2 debit cards in one transaction? Example 2x$500.

1. Swipe debit card on my terminal after total comes up $1000.

2. PIN pad comes up. Enter 4 digit PIN.

3. Do you want cash back? press NO

4. Do you want full amount on this card? press NO <<<Note: I pressed YES and did not have a step 5. - PHLisa

5. Cashier reads something on register, asks how much on this card. $500. They push something to continue.

6. Swipe card #2. Enter PIN

7. Repeat 3 to 5. Total: 0.00

8. Receipt prints. Thank cashier. The end.

(thanks to Mamibear)

Q: Can someone else buy a Redbird card for you?

Yes. When you buy a temp Redbird card at Target, you have to give them your drivers license info, your SSN (can be any set of numbers, does not need to be real), birthdate, and more. Then, you have to register the card online in order to get a permanent card. In the process of registering online, they ask for the birthday of the original buyer on the first screen, but you can put your own and it will still work. Either way, you can still change the details on the following screens. I did this for my wife. I bought the card at Target and used my own driver�s license, SSN, etc. But, when I got home, I registered the card to my wife. I can�t promise this will work for everyone, but it worked for me.

Q: Can you reload Serve/Bluebird at Target?

No.

Q: How do I contact Target's support team to resolve an issue with my RedCard?

Call Target's Prepaid Resolution Team, their direct telephone number is 800 438 6468 (open from 8AM to 430PM MST).

Q: Can you have both Redbird and AFT cards?

Yes.

You can have both Redbird and AFT since they are independent products.

Q: I got a "Pending" notice that the registration is being reviewed, what now?

Add [email protected] to your address book, and check your spam folder for an email about it. You can also call in. They will need images or faxes of:

� Social Security Documentation (must clearly show full 9 digit Social Security Number). Choose 1 of the following options:

◦ Social Security Card, OR

◦ A Medicare insurance card

Plus...

� Picture ID

◦ A valid driver's license card OR

◦ A valid state issued ID OR

◦ A valid United States Government ID Card (e.g. Green Card) OR

◦ A valid United States Passport (photo page only)

◦ Social Security Card, OR

◦ A Medicare insurance card

Plus...

� Picture ID

◦ A valid driver's license card OR

◦ A valid state issued ID OR

◦ A valid United States Government ID Card (e.g. Green Card) OR

◦ A valid United States Passport (photo page only)

Secure Document Upload

Here's the link to upload secure documents to REDcard: https://secure.prepaidredcard.com/User/SecureFileUpload

Prepaid REDcard (Target) 2015-2016

Jun 24, 2015, 7:37 am

#8701

Join Date: Jul 2014

Posts: 3,688

regardless of other people's experiences, it's always been YMMV even though many hate that acronym. standing up for yourself does NOT work all the time depending on store personnel you're dealing with. some MS customers may try and exert pressure but if store management says NO, they can insist and make a scene but management has the right to kick them out of the store for causing disturbance. Stores are private properties and management reserves the right to make their own rules; OTOH, customers can file a complaint to store's HQ but it doesn't mean they'll get their way.

Jun 24, 2015, 7:51 am

Jun 24, 2015, 7:51 am

#8702

Join Date: Jan 2014

Posts: 1,269

^ This!

Getting tired of all these Type B personalities simply accepting made up rules by minimum wage floor managers (I'm not really sure what a floor manager even does but I digress). In the game of MS, Type A people will always win. And Type B people will come on these boards and seek the advice of Type A people wondering where they went astray.

Getting tired of all these Type B personalities simply accepting made up rules by minimum wage floor managers (I'm not really sure what a floor manager even does but I digress). In the game of MS, Type A people will always win. And Type B people will come on these boards and seek the advice of Type A people wondering where they went astray.

regardless of other people's experiences, it's always been YMMV even though many hate that acronym. standing up for yourself does NOT work all the time depending on store personnel you're dealing with. some MS customers may try and exert pressure but if store management says NO, they can insist and make a scene but management has the right to kick them out of the store for causing disturbance. Stores are private properties and management reserves the right to make their own rules; OTOH, customers can file a complaint to store's HQ but it doesn't mean they'll get their way.

Jun 24, 2015, 8:35 am

#8703

Join Date: Mar 2013

Location: PVD

Programs: AA Plat, HH Gold, Hyatt Plat, Marriott Gold, National EE

Posts: 135

^ This!

Getting tired of all these Type B personalities simply accepting made up rules by minimum wage floor managers (I'm not really sure what a floor manager even does but I digress). In the game of MS, Type A people will always win. And Type B people will come on these boards and seek the advice of Type A people wondering where they went astray.

Getting tired of all these Type B personalities simply accepting made up rules by minimum wage floor managers (I'm not really sure what a floor manager even does but I digress). In the game of MS, Type A people will always win. And Type B people will come on these boards and seek the advice of Type A people wondering where they went astray.

Jun 24, 2015, 9:31 am

#8704

Join Date: Feb 2012

Location: Los Angles

Posts: 2,101

but if store management says NO, they can insist and make a scene but management has the right to kick them out of the store for causing disturbance. Stores are private properties and management reserves the right to make their own rules; OTOH, customers can file a complaint to store's HQ but it doesn't mean they'll get their way.

Does this seem to be business unfriendly attitude? hostile business environment? why? Corporate headquarters not aware of their minimum wage employee behavior? The friction between the business and clients/customers is never a healthy sign....(remember? customer is always right, the American thing only if he is not a terrorist

)

)Business are happy to participate in the MS activity (money making) so, why be difficult? (fraud, ML is all BS) unless they know smething we don't know?

Are they scared of regulators? being shut down? has happened to all the Gebits, the seasoned MSers know the stories!

Are they struggling to survive the MS game? because is so lucrative? but stay under the radar?

Jun 24, 2015, 11:16 am

#8705

Suspended

Join Date: Dec 2014

Posts: 8,460

Have you seen Target "security" before? At my local store, the security team consists of a 30 something tall lanky woman who reminds me of Olive Oil in Popeye. Doesn't exactly strike fear in my heart and she won't be "throwing" anyone out of any store.

Jun 24, 2015, 11:41 am

#8706

Join Date: Dec 2000

Location: NY

Posts: 132

One more boring data point for those that care. Loaded $2k worth of VGC's across a couple RB cards today, 7/24, with no problems. No ID required. This was done in upstate NY at a Target near Albany.

I continue to have no problems at many different Targets up here. Friendly CS reps and only on a few occasions have I had to show ID.

YMMV but for now I am chugging along at a nice slow pace, meeting min spends with ease along with some MS'ing.

I continue to have no problems at many different Targets up here. Friendly CS reps and only on a few occasions have I had to show ID.

YMMV but for now I am chugging along at a nice slow pace, meeting min spends with ease along with some MS'ing.

Jun 24, 2015, 11:51 am

#8707

Join Date: Apr 2015

Location: PHX

Programs: Southwest, Hawaiian

Posts: 2

Payment from Redbird to credit card

Hope this helps.

Jun 24, 2015, 11:55 am

#8708

Join Date: Jun 2011

Posts: 800

I have made several large payments to my Chase SW cards from redbird online bill pay. I was curious how the checks came so I sent myself one. There was only a check and the memo field had my name. Neither Target nor Amex were listed on the check so the credit card company will have no idea where it came from. The check was from a bank, but I don't remember which one. This made me feel better knowing that it would be harder for them to figure out I was MS'ing. For all they know, they just received a check for payment from a bank.

Hope this helps.

Hope this helps.

We don't get to see how that shows up on their Accounts Receivable end...

Jun 24, 2015, 11:56 am

#8709

Join Date: Jun 2011

Posts: 800

Went back to the store that had the register upgrades today...

They insisted that I use the registers with the older firmware. I suggested the K8 command, but they would rather me use what still worked vs try something new.

I guess that's a good thing? But I'll never get to test this until they upgrade all their registers and it BETTER WORK THEN!

They insisted that I use the registers with the older firmware. I suggested the K8 command, but they would rather me use what still worked vs try something new.

I guess that's a good thing? But I'll never get to test this until they upgrade all their registers and it BETTER WORK THEN!

Jun 24, 2015, 12:24 pm

#8710

Join Date: Jul 2014

Posts: 3,688

I don't know about your Target but the ones I've been to, the security men were burly guys who don't faze me at all because my experience with these stores are nice and cordial. I've seen stores, though and not just Target, who called the cops on unruly customers. It still remains to be YMMV, I know you won't accept it so we can just agree to disagree.

Jun 24, 2015, 2:11 pm

#8712

FlyerTalk Evangelist

Join Date: Jul 2003

Location: Florida

Posts: 29,767

I have made several large payments to my Chase SW cards from redbird online bill pay. I was curious how the checks came so I sent myself one. There was only a check and the memo field had my name. Neither Target nor Amex were listed on the check so the credit card company will have no idea where it came from. The check was from a bank, but I don't remember which one. This made me feel better knowing that it would be harder for them to figure out I was MS'ing. For all they know, they just received a check for payment from a bank.

Hope this helps.

Hope this helps.

For example

FIA shows Net Access for the payment from direct PULL, but shows Electronic on all prepaid card account payments (RB/BB/Serve)

Citi shows Online Payment for the payment from direct PULL, but shows simply Payment for either Wally BP or from all prepaid card accounts.

I dont rememer how Chase shows it but I believe it is different than the direct PULL.

Jun 24, 2015, 2:55 pm

#8713

Join Date: Jul 2001

Programs: Marriott LT Tit; Hyatt Explorist; Hilton CC Gold; IHG CC Plt; Hertz (MR) 5 star

Posts: 5,536

Did my last $500 Gebit load for the month yesterday. No questions, no drama, no snags, no problems.

At the risk of once again being labeled a snob, one shouldn't MS with money that they can't afford to cover for 6 months. I don't know all of the ways to have your money trapped while MSing, but there are enough traps that 'going big' when you can barely cover your monthly rent is setting yourself up for some financial pain and stress.

We're dealing with AmEx's back end with the RB. And anyone who's MS'd for a while will tell you that AmEx is a hot mess. Their error rate is completely unacceptable in the financial industry; it's a wonder how they are able to stay in business. Sooner or later, they will lose your load or payment. They'll eventually make it right, but it could be fast or it could take 2-3 months.

With the additional step of having to use a Gebit card to load your RB, the risk of your money being tied up for a while is increased. In addition to the possibility of being denied loading a Gebit onto your RB, there's the risk of some thief stealing your GC information and draining it before you get a chance to load it onto your RB.

This is not to say that you can't MS on a shoestring, but it would be better to buy one $500 GC vs 5x$500 GCs at one time if one's worried about being separated from their money for an extended period of time.

And you've only been here since Oct 14. It's been that way here for a very long time.

And you've only been here since Oct 14. It's been that way here for a very long time.

Depending on my mood, I'll either regurgitate the easily found answer, not bother responding, or make a snarky reply. I'm trying to cut back on the third response but am not always successful.

I'm pretty sure that both individual store and regional managers have the right to 'make up' their own rules. You can argue, write corporate, or even make such a hissy fit in the store that the local constable is called to escort you out of the store, but I've never read of any of those tactics changing an individual store's policy. Please post quotes to anyone who has stated that those tactics have worked. You might want to start with our North Carolina RB brethren.

We're dealing with AmEx's back end with the RB. And anyone who's MS'd for a while will tell you that AmEx is a hot mess. Their error rate is completely unacceptable in the financial industry; it's a wonder how they are able to stay in business. Sooner or later, they will lose your load or payment. They'll eventually make it right, but it could be fast or it could take 2-3 months.

With the additional step of having to use a Gebit card to load your RB, the risk of your money being tied up for a while is increased. In addition to the possibility of being denied loading a Gebit onto your RB, there's the risk of some thief stealing your GC information and draining it before you get a chance to load it onto your RB.

This is not to say that you can't MS on a shoestring, but it would be better to buy one $500 GC vs 5x$500 GCs at one time if one's worried about being separated from their money for an extended period of time.

And you've only been here since Oct 14. It's been that way here for a very long time.Depending on my mood, I'll either regurgitate the easily found answer, not bother responding, or make a snarky reply. I'm trying to cut back on the third response but am not always successful.

I'm pretty sure that both individual store and regional managers have the right to 'make up' their own rules. You can argue, write corporate, or even make such a hissy fit in the store that the local constable is called to escort you out of the store, but I've never read of any of those tactics changing an individual store's policy. Please post quotes to anyone who has stated that those tactics have worked. You might want to start with our North Carolina RB brethren.

Jun 24, 2015, 3:44 pm

#8714

Suspended

Join Date: Nov 1999

Posts: 24,153

Thats why stores have gone eto ca$h only and if they find folks walking in with wads of 100s or 20s you know it wont be long till they make it that $100 is the max for a MO and only say 2 per day. thats why you see in many mom & pops that they wont take anything larger then a $20 bill and in some cases dont even want a $20. They cant afford to take in 1 counterfeit

Yea its a hassle but I just say OK thanks anyway, leave and ddrive to the next location hoping for a better outcome

Jun 24, 2015, 5:35 pm

#8715

Join Date: Jan 2015

Location: Champaign, IL

Programs: Total Rewards Diamond, Wyndham Diamond, Marriott Gold, AA Gold

Posts: 564

I believe there are 2 diferent items 1 the business itself and 2nd the employees. Both with then same goal in mind = to make money. Now when folks start usingstolen CCs or DCs or ripping off GCs via a scam after its loaded, no store wants to end up being out the $$$, and no employee wants to lose the $8 an hour job they are relying on to help pay their bills. So if once in a blue moon they get taken thats 1 thing but when it happens too often or they hear of it happening to others they will make up their lines in order to get rid of us and retain their job, and not allow us to do our thing. I dont blame them!

Thats why stores have gone eto ca$h only and if they find folks walking in with wads of 100s or 20s you know it wont be long till they make it that $100 is the max for a MO and only say 2 per day. thats why you see in many mom & pops that they wont take anything larger then a $20 bill and in some cases dont even want a $20. They cant afford to take in 1 counterfeit

Yea its a hassle but I just say OK thanks anyway, leave and ddrive to the next location hoping for a better outcome

Thats why stores have gone eto ca$h only and if they find folks walking in with wads of 100s or 20s you know it wont be long till they make it that $100 is the max for a MO and only say 2 per day. thats why you see in many mom & pops that they wont take anything larger then a $20 bill and in some cases dont even want a $20. They cant afford to take in 1 counterfeit

Yea its a hassle but I just say OK thanks anyway, leave and ddrive to the next location hoping for a better outcome

If I'm checking out and hand the cashier two $20 bills and the cashier says, "Sorry. We don't accept $20 bills." I would laugh in their face. Actually no, I would ask to speak to the manager and then laugh in the managers face.