Apr 14, 2016, 7:52 am

Apr 14, 2016, 7:52 am

Last edit by: garykung

CitiGold is Citi's premium banking relationship. To remain a Citigold client, maintain a minimum combined average monthly balance of $200,000 in eligible linked deposit, retirement and investment accounts. There is no monthly service fee for accounts in The Citigold Account Package.

Be aware that Citi Wealth Management will not allow any trading of non traditional stocks and ETFs. No leveraged ETFs, no inverse ETFs. Its brokerage service is similar to Chase YouInvest. It is just basic investment service.

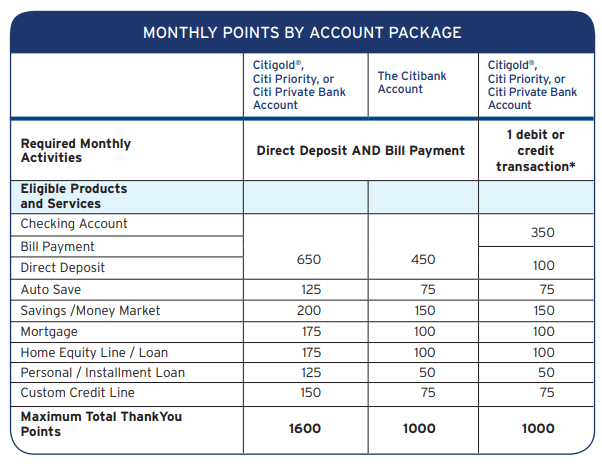

1. Click HERE to read a separate thread discussing expiration of ThankYou Points when closing a Citigold account.

2. Citi has introduced Citi Priority with a minimum combined balance of $50K as of November 6, 2016. Those who were no longer qualified under the new Citigold requirement has been downgraded to Citi Priority. Discussion HERE.

Be aware that Citi Wealth Management will not allow any trading of non traditional stocks and ETFs. No leveraged ETFs, no inverse ETFs. Its brokerage service is similar to Chase YouInvest. It is just basic investment service.

1. Click HERE to read a separate thread discussing expiration of ThankYou Points when closing a Citigold account.

2. Citi has introduced Citi Priority with a minimum combined balance of $50K as of November 6, 2016. Those who were no longer qualified under the new Citigold requirement has been downgraded to Citi Priority. Discussion HERE.

Benefits of a Citigold account? [consolidated]

Jan 18, 2021, 4:19 pm

#901

Join Date: Jul 2014

Location: Western US

Programs: Costco Executive Member, Amazon Optimus Prime

Posts: 1,251

I guess we all know what "self-directed" or "self-guided" mean. So if both Chase and Citi state they offer stock and ETF trading, but in reality then only allow a subset of stocks and ETFs, then this is misleading to me. I was mislead for sure. They should have disclosed this at beginning. It is none of their business if some novice traders got wiped out. They can be wiped out the same way at Chase and Citi if they borrowed on margin and do risky trades like with options etc.

I guess both Chase and Citi were pressured by the evolving brokerage industry. I remember before most brokerage houses had the zero commissions, Citi charged good money for stock trading. And its brokerage offering is really subpar, with very limited functionalities.

The worst thing with Citi is its customer service. Most are serviced with overseas service centers.

I guess both Chase and Citi were pressured by the evolving brokerage industry. I remember before most brokerage houses had the zero commissions, Citi charged good money for stock trading. And its brokerage offering is really subpar, with very limited functionalities.

The worst thing with Citi is its customer service. Most are serviced with overseas service centers.

For people who its really an issue for they can check with a broker before they ACAT a bunch of stuff over, or ask to see the blocked securities list. A long time ago we had some accounts at Wells Fargo Advisors and they were pretty lousy about blocking Vanguard products, and only wanting people to use partner firm ETFs (ie. ones sharing some of the mgmt fee back to the Wells broker), so after a year or two of that foolishness we ACAT'd out of there. That was a broker who'd served part of our family for 20 years or so, but when she moved to WFA we had not realized all the craziness that would come with her move. (And in any case, their advice was nothing special that a Kiplingers magazine wouldn't replicate, not worth the huge fee they collected every year)

As sucky as the citi pwm platform is, plop in a few ETFs that can be left alone, and let them meet the balance tests to get you free cookies from Citi.

Jan 18, 2021, 4:45 pm

Jan 18, 2021, 4:45 pm

#902

Suspended

Join Date: Jan 2017

Location: EWR/PHL/BWI

Posts: 4,412

The issue is that some of these levered/inverse products have payoffs that are difficult for retail investors to understand. Path dependency is not a concept they grasp. They can't understand why their underlying asset class is either flat/up over a year, yet their ETF is down, because the underlying price path taken along the way was up and down (volatile) and that tends to destroy value along the way. So after enough arbitration suits (which the industry wins) someone in the general counsel's office says 'block these products'. It still costs money, management attention, and broker distraction to fight off suits, no matter how easy wins they are. There is also reputational damage, as aggrieved investors tell their friends or write on chatboards. The upside to allowing those products is small, especially in a world where there are no real commissions to be had. And most fee based advisors are going to be very reluctant to use them in portfolios too.

For people who its really an issue for they can check with a broker before they ACAT a bunch of stuff over, or ask to see the blocked securities list. A long time ago we had some accounts at Wells Fargo Advisors and they were pretty lousy about blocking Vanguard products, and only wanting people to use partner firm ETFs (ie. ones sharing some of the mgmt fee back to the Wells broker), so after a year or two of that foolishness we ACAT'd out of there. That was a broker who'd served part of our family for 20 years or so, but when she moved to WFA we had not realized all the craziness that would come with her move. (And in any case, their advice was nothing special that a Kiplingers magazine wouldn't replicate, not worth the huge fee they collected every year)

As sucky as the citi pwm platform is, plop in a few ETFs that can be left alone, and let them meet the balance tests to get you free cookies from Citi.

For people who its really an issue for they can check with a broker before they ACAT a bunch of stuff over, or ask to see the blocked securities list. A long time ago we had some accounts at Wells Fargo Advisors and they were pretty lousy about blocking Vanguard products, and only wanting people to use partner firm ETFs (ie. ones sharing some of the mgmt fee back to the Wells broker), so after a year or two of that foolishness we ACAT'd out of there. That was a broker who'd served part of our family for 20 years or so, but when she moved to WFA we had not realized all the craziness that would come with her move. (And in any case, their advice was nothing special that a Kiplingers magazine wouldn't replicate, not worth the huge fee they collected every year)

As sucky as the citi pwm platform is, plop in a few ETFs that can be left alone, and let them meet the balance tests to get you free cookies from Citi.

Maybe Morgan Stanley + ETrade can open some front. Who knows.

Jan 19, 2021, 2:00 pm

#903

Join Date: Jul 2014

Location: Western US

Programs: Costco Executive Member, Amazon Optimus Prime

Posts: 1,251

Citi is not my only service provider in this dimension, maybe a half dozen providers too. I'm happy to use each for specific benefits....sort of like having a quiver of cards!!!

Jan 25, 2021, 12:36 pm

#904

Join Date: May 2003

Location: LAX

Programs: DL-Plat, UA-Plat 2MM, AA-PlatPro, B6-Mosaic 3, AY-Plat, HY-Globalist, MR-LT Plat, HH-Gold

Posts: 1,237

My spouse received a checking account offer with up to 60k AA miles to sign up for a new checking account. I am a CG account holder and he doesn’t hold any non-CC accounts with Citi. New CG accounts get the highest bonus. Can I sign him up for a new account using my CG status and get the bonus? Does that need to be done at account opening? Thanks for any DPs!

ETA:

For future reference, we met with a CG banker and it has to be a separate account. In my case, they signed up the new account as Citi Priority until the bonus hits, at that point we can link it to CG and it will be fee free. It means paying a monthly fee for a few months since we won’t fund it with the $50k required, but well worth it for 50k miles.

ETA:

For future reference, we met with a CG banker and it has to be a separate account. In my case, they signed up the new account as Citi Priority until the bonus hits, at that point we can link it to CG and it will be fee free. It means paying a monthly fee for a few months since we won’t fund it with the $50k required, but well worth it for 50k miles.

Last edited by daslax; Feb 1, 2021 at 9:55 pm Reason: Added outcome from Citi banker

Feb 3, 2021, 11:20 am

#905

Join Date: Feb 2021

Posts: 4

Does anyone here use Citi Personal Wealth Management self-directed brokerage to maintain Citigold status?

I opened an account recently to bring in some investments, and so far it has been a nightmare:

- Brokerage website is embarrassingly ancient, have they not looked at their competitors?

- Citi Mobile app brokerage features are broken: you place a trade and it doesn't show up for 20 minutes -- called and they said "they're fixing it" (yeah, sure...)

- No way to link external accounts for ACH or submit online funds transfers: you have to call every time you want to ACH in from an external account

- ACAT transfers also need to be started manually over the phone and using DocuSign

- Citi Wealth Management phone lines are broken: they redirect you to the banking division unless you magically know to press "0 0" at the beginning (also was told "they're fixing it")

- Everything else needs to be done over the phone with 30 minute wait times. I was told there's no way to secure message or email anyone

- Linking Citi Personal Wealth Management to personal finance apps like Mint and Personal Capital is also completely broken

I'm curious to hear what other people's experiences are like. There is no point in having cash sitting in low-yield accounts for Citigold, and I was hoping to use brokerage to hit the balance instead. But their technology, customer service and everything else is so behind the times, that I'm now on the verge of aborting this and moving my entire banking relationship elsewhere (Chase, Schwab or somewhere else).

I opened an account recently to bring in some investments, and so far it has been a nightmare:

- Brokerage website is embarrassingly ancient, have they not looked at their competitors?

- Citi Mobile app brokerage features are broken: you place a trade and it doesn't show up for 20 minutes -- called and they said "they're fixing it" (yeah, sure...)

- No way to link external accounts for ACH or submit online funds transfers: you have to call every time you want to ACH in from an external account

- ACAT transfers also need to be started manually over the phone and using DocuSign

- Citi Wealth Management phone lines are broken: they redirect you to the banking division unless you magically know to press "0 0" at the beginning (also was told "they're fixing it")

- Everything else needs to be done over the phone with 30 minute wait times. I was told there's no way to secure message or email anyone

- Linking Citi Personal Wealth Management to personal finance apps like Mint and Personal Capital is also completely broken

I'm curious to hear what other people's experiences are like. There is no point in having cash sitting in low-yield accounts for Citigold, and I was hoping to use brokerage to hit the balance instead. But their technology, customer service and everything else is so behind the times, that I'm now on the verge of aborting this and moving my entire banking relationship elsewhere (Chase, Schwab or somewhere else).

Feb 3, 2021, 11:47 am

#906

Suspended

Join Date: Jan 2017

Location: EWR/PHL/BWI

Posts: 4,412

If you read the old posts, you'll see my experience.

I opened both bank and self-directed investment accounts with Citi. Go through a lot of loops on account opening and account linking. Then to the end, I realized Citi does not offer all the ETFs. It is the same way as what Chase offers, no complicated ETFs, like leveraged and inverse ETFs. I've not tried options and shorting any stocks, but I figure it is not the place for that.

Basically both Citi and Chase offer the investment accounts for folks to trade regular stocks and ETFs. The real intention is to let investors invest in their own ETF and mutual funds.

I finally unwound all my bank and investment accounts with Citi. Not worth it. The other key issue is that Citi has closed many local branches in Northeast states. So the lack of local branch with outdated technology is very toxic.

I only have CC accounts with Citi now. Not good experience.

I opened both bank and self-directed investment accounts with Citi. Go through a lot of loops on account opening and account linking. Then to the end, I realized Citi does not offer all the ETFs. It is the same way as what Chase offers, no complicated ETFs, like leveraged and inverse ETFs. I've not tried options and shorting any stocks, but I figure it is not the place for that.

Basically both Citi and Chase offer the investment accounts for folks to trade regular stocks and ETFs. The real intention is to let investors invest in their own ETF and mutual funds.

I finally unwound all my bank and investment accounts with Citi. Not worth it. The other key issue is that Citi has closed many local branches in Northeast states. So the lack of local branch with outdated technology is very toxic.

I only have CC accounts with Citi now. Not good experience.

Feb 3, 2021, 12:07 pm

#907

Suspended

Join Date: Jan 2017

Location: EWR/PHL/BWI

Posts: 4,412

Wells Fargo is really under rated. Other than some slow processing now with the COVID, never had issues with WF for more than 15 years. Made a lot of $ with WellsTrade. Not with Citi.

There are two WF local branches within 10 minute drive....

There are two WF local branches within 10 minute drive....

Feb 3, 2021, 12:24 pm

#908

Join Date: Feb 2021

Posts: 4

If you read the old posts, you'll see my experience.

I opened both bank and self-directed investment accounts with Citi. Go through a lot of loops on account opening and account linking. Then to the end, I realized Citi does not offer all the ETFs. It is the same way as what Chase offers, no complicated ETFs, like leveraged and inverse ETFs. I've not tried options and shorting any stocks, but I figure it is not the place for that.

Basically both Citi and Chase offer the investment accounts for folks to trade regular stocks and ETFs. The real intention is to let investors invest in their own ETF and mutual funds.

I finally unwound all my bank and investment accounts with Citi. Not worth it. The other key issue is that Citi has closed many local branches in Northeast states. So the lack of local branch with outdated technology is very toxic.

I only have CC accounts with Citi now. Not good experience.

I opened both bank and self-directed investment accounts with Citi. Go through a lot of loops on account opening and account linking. Then to the end, I realized Citi does not offer all the ETFs. It is the same way as what Chase offers, no complicated ETFs, like leveraged and inverse ETFs. I've not tried options and shorting any stocks, but I figure it is not the place for that.

Basically both Citi and Chase offer the investment accounts for folks to trade regular stocks and ETFs. The real intention is to let investors invest in their own ETF and mutual funds.

I finally unwound all my bank and investment accounts with Citi. Not worth it. The other key issue is that Citi has closed many local branches in Northeast states. So the lack of local branch with outdated technology is very toxic.

I only have CC accounts with Citi now. Not good experience.

Wells Fargo won't work for me. I need a bank that waives foreign exchange fees on ATM withdrawals abroad, refunds out of network ATM fees, and provides free perks like points for banking relationship (e.g. ThankYou points) and benefits such as free safe deposit, which I get at Citi. The only major brick-and-mortar bank that seems to offer all of this is Chase.

Feb 3, 2021, 12:48 pm

#909

Suspended

Join Date: Jan 2017

Location: EWR/PHL/BWI

Posts: 4,412

Thanks. Yeah, I'm not looking to actively trade or use sophisticated instruments, just park a bunch of passive ETFs. But if I can't even link Citi Wealth Management to Mint or Personal Capital, this is a massive fail...

Wells Fargo won't work for me. I need a bank that waives foreign exchange fees on ATM withdrawals abroad, refunds out of network ATM fees, and provides free perks like points for banking relationship (e.g. ThankYou points) and benefits such as free safe deposit, which I get at Citi. The only major brick-and-mortar bank that seems to offer all of this is Chase.

Wells Fargo won't work for me. I need a bank that waives foreign exchange fees on ATM withdrawals abroad, refunds out of network ATM fees, and provides free perks like points for banking relationship (e.g. ThankYou points) and benefits such as free safe deposit, which I get at Citi. The only major brick-and-mortar bank that seems to offer all of this is Chase.

Feb 3, 2021, 12:58 pm

#910

Moderator

Join Date: Jun 2003

Location: Miami, Mpls & London

Programs: AA & Marriott Perpetual Platinum; DL & HH Gold

Posts: 48,959

Feb 3, 2021, 1:01 pm

#911

Join Date: Feb 2021

Posts: 4

But you need to think how much you lose or gain from parking your $$$ with them. Or you can get more returns from a full broker. If you get only $100 per year from those perks, but you can make $1,000 more from other brokers, then it is not worth to park at Citi or Chase.

Which brokerages give you $1,000 in perks? I have Vanguard and TD Ameritrade, and they provide nothing unless you have balances in the millions of dollars... Schwab also doesn't provide much.

Feb 3, 2021, 1:18 pm

#912

Moderator

Join Date: Jun 2003

Location: Miami, Mpls & London

Programs: AA & Marriott Perpetual Platinum; DL & HH Gold

Posts: 48,959

Feb 3, 2021, 1:20 pm

#913

Suspended

Join Date: Jan 2017

Location: EWR/PHL/BWI

Posts: 4,412

At Citi today I get ~$130 worth of ThankYou points per year for my banking relationship at Citi (doesn't include credit cards), a free medium safe deposit box that is ~$125, plus the other perks (ATM fee rebates, no foreign exchange fee, museum passes, Citigold lounges, etc). So it's a pretty decent level of perks compared to other banks. The only better perk I've found elsewhere for similar relationship balances is Chase has free outgoing wires, but I don't need those, and Chase doesn't give you UltimateRewards points for the banking relationship, has no lounges worldwide, etc.

Which brokerages give you $1,000 in perks? I have Vanguard and TD Ameritrade, and they provide nothing unless you have balances in the millions of dollars... Schwab also doesn't provide much.

Which brokerages give you $1,000 in perks? I have Vanguard and TD Ameritrade, and they provide nothing unless you have balances in the millions of dollars... Schwab also doesn't provide much.

Citigold lounge? Do not know where to find them. BofA has very good museum pass. Schwab offers excellent ATM for overseas use.

If I get $100,000 to invest with one full broker and if I can get 1% more than at Citi, then that is $1,000 extra gain. If I get $1,000,000 at a good broker, a 1% extra gain gives me $10,000. This is much more than the Citi TY points they gave to me. Not interested. I fled.

Feb 3, 2021, 1:21 pm

#914

Suspended

Join Date: Jan 2017

Location: EWR/PHL/BWI

Posts: 4,412

I get far more Citi ThankYou points from my Seas cards....

Those bank TY points expire in some months. They can't be combined with CC TY points. Much lower value. As I recall. There is monthly max. It is worth about $10 to $20/month.

Those bank TY points expire in some months. They can't be combined with CC TY points. Much lower value. As I recall. There is monthly max. It is worth about $10 to $20/month.

Last edited by RedSun; Feb 3, 2021 at 1:30 pm

Feb 3, 2021, 1:30 pm

#915

Join Date: Feb 2021

Posts: 4

The banking TY points are nice. I can get safe deposit boxes at BofA and Wells Fargo. There is not even any Citi branches in our part of country. I'll have to go to New York City.

Citigold lounge? Do not know where to find them. BofA has very good museum pass. Schwab offers excellent ATM for overseas use.

If I get $100,000 to invest with one full broker and if I can get 1% more than at Citi, then that is $1,000 extra gain. If I get $1,000,000 at a good broker, a 1% extra gain gives me $10,000. This is much more than the Citi TY points they gave to me. Not interested. I fled.

Citigold lounge? Do not know where to find them. BofA has very good museum pass. Schwab offers excellent ATM for overseas use.

If I get $100,000 to invest with one full broker and if I can get 1% more than at Citi, then that is $1,000 extra gain. If I get $1,000,000 at a good broker, a 1% extra gain gives me $10,000. This is much more than the Citi TY points they gave to me. Not interested. I fled.

How do you get "1% more" through another brokerage? Are they paying you interest on your invested equities, paying you cash for maintaining a balance? Never heard of this. I'm not talking about investment returns here. I'm doing an apples-to-apples comparison for buying the same ETFs (e.g. VOO, VTI, etc) at different brokers. They have exactly the same rate of return, so not sure how you can get 1% more.

Now, if you're trying to access other sophisticated instruments, I get it, but that's not a fair comparison in terms of the actual perks that the brokerage is giving you for having a relationship with them. You're simply looking for other investment products, completely unrelated to what the brokerage is "paying you" to use them vs someone else.