Dec 20, 2015, 4:45 am

Dec 20, 2015, 4:45 am

Last edit by: wilsnunn

The FlyerTalk Lending Team on Kiva:

improving lives a small loan at a time.

Kiva.org is the not-for-profit microlending organization that networks people willing to lend to small entrepreneurs in developing nations using available technology and international networking / collaboration, and how Kiva.org had become an approved FlyerTalk charity thanks to TalkBoard's approval June 29, 2008 <link> It is listed on the FlyerTalk Cares page.improving lives a small loan at a time.

"Kiva is a grassroots project started by a team with a big idea: one-to-one, real-time lending to the poor via the Internet. Currently, we take no cut of the loan you make through our site -- 100% goes to the entrepreneur. We suggest a 10% donation, in addition to your loan, to help us cover our costs. Kiva is a 501(c)(3) nonprofit and your donation is tax-deductible for US taxpayers." (Suggested donations for administrative overhead, low though that is, are not required - you may lend 100% if you so choose.)

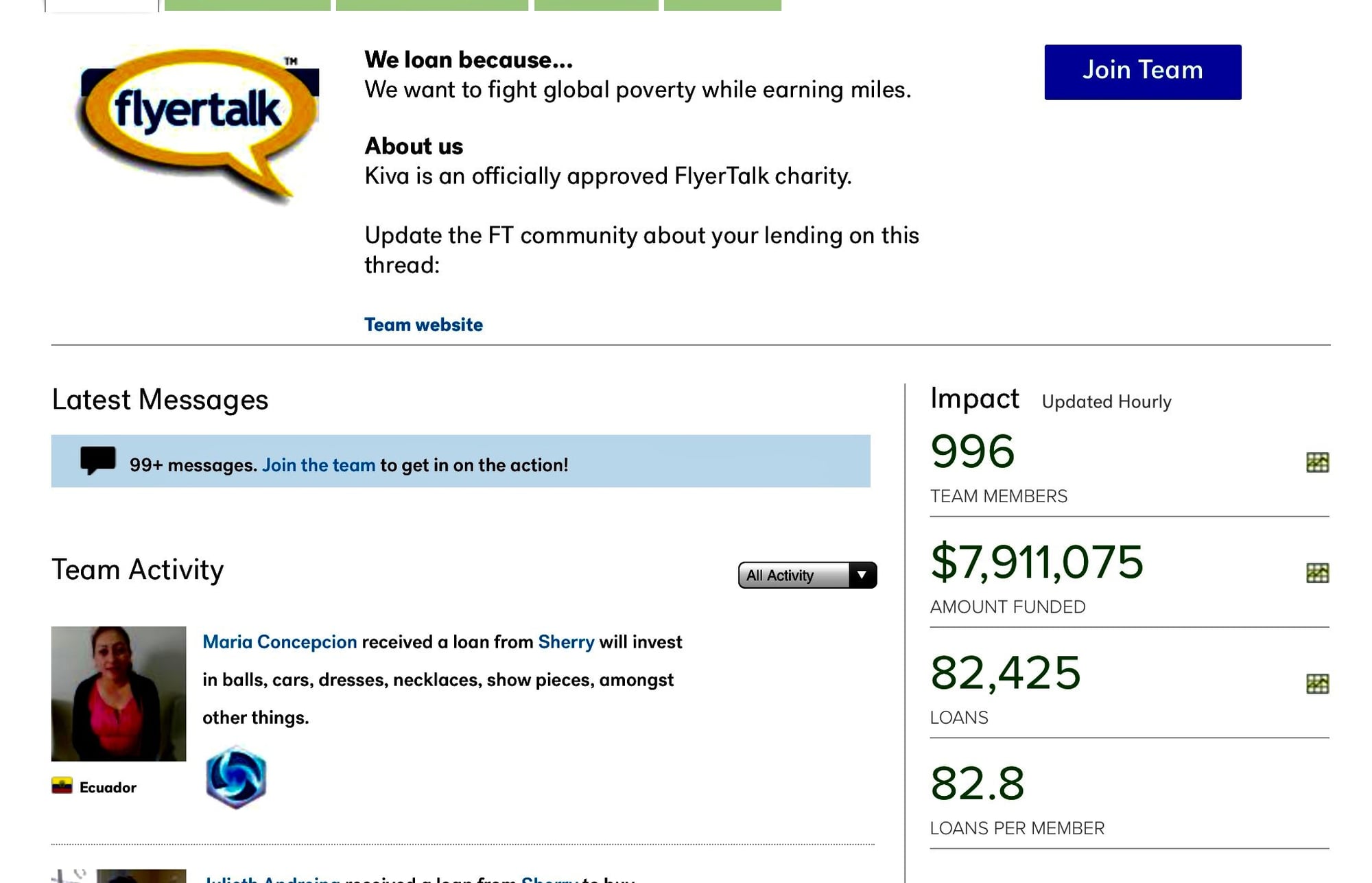

As of 15 May 2016 it was 607 FlyerTalk lending team who have lent $2,209,175 in 37,092 loans! And now as of 30 June 2019 it is 941 members who have lent $6,415,775 in 71,722 loans!

Our motto is: "We loan because: We want to fight global poverty while earning miles."

This is tangible evidence Flyertalk Cares! There are likely other FlyerTalkers on Kiva who have not joined - if you are one of them, do so now to show your and FT's support and involvement. If you haven't lent yet, check it out - you may want to join up. For the low-income entrepreneurs on five continents who are requesting loans, microlending is significant - and it takes a lot of drops to fill the bucket. (Read on to see updates!)

Now, we can see this sophisticated network link resources from those who can lend (no interest, sorry!) with those who are needy, worthy and screened by local NGOs and have a need to start / expand their small business to enhance their and their families' survival. And, using PayPal and your FFP/FFG linked card or account, you can earn miles or points with many loans!

FlyerTalkers are lending, and fulfilling one of FT's seminal values, that of "paying it forward."

Read more about Kiva.org, who supports and enables it (Intel, Google, Paypal, Intuit and many others,) and see if you have $25.00 (or more) you can lend someone deserving in a land you have visited and enjoyed (or not.)

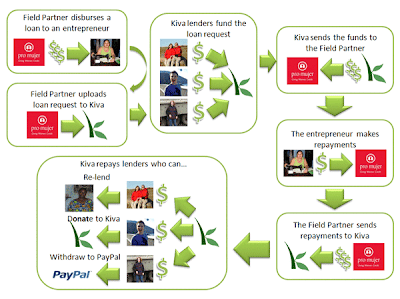

This is how it works:

Add your experiences here, or if you haven't joined... won't you consider joining the FlyerTalker Lending Team?

You can see who the latest FT borrowers are (some still possibly needing loans) here

For ease, you can click here: Subscribe to FlyerTalker Lending Team on Kiva.org

FlyerTalker Lending Team on Kiva.org!

Jan 29, 2020 | 4:14 pm

Jan 29, 2020 | 4:14 pm

#1352

Join Date: Aug 2008

Location: Somewhere in Florida

Posts: 2,876

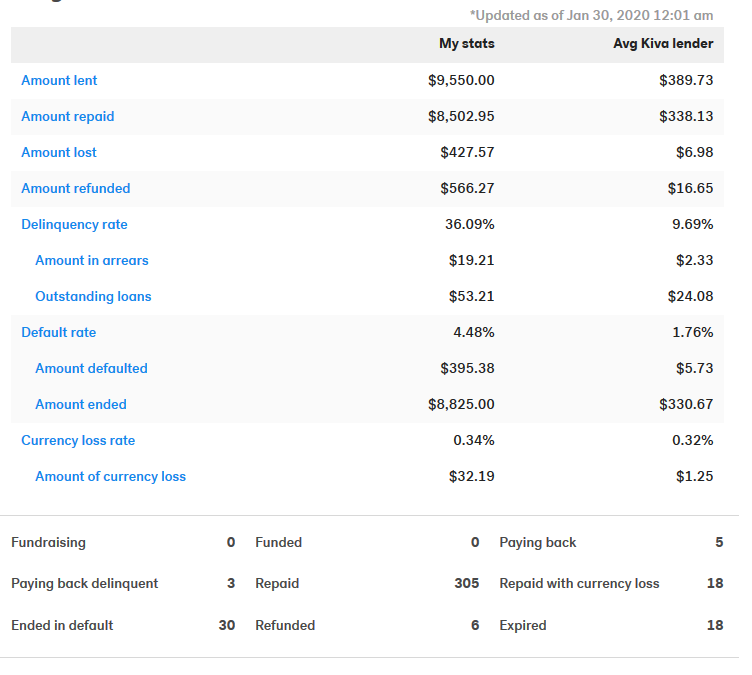

Well, it's been a year since I updated my stats, so here's where I stand as of Jan 2020:

Started in Dec 2015.

Amount Lent: $18,900

Amount Defaulted: $22.97

Amount of Currency Rate Loss: $0.41 (unchanged from last year)

Total losses: $23.38

$23.38 / $18,900 = 0.001237 or 0.124%. (Note that this is lower than last year)

US inflation for the same time period was 9%.

So, I've made 690 loans, got the chance to help out at least that many people, and earned ~66k UR points for $23.38. Still not as great of a return as the prior year, but still a good deal in my book.

Defaulted loans: 4 total.

1) $25. Total loan was $8050 in Rwanda. Debtor paid back $22.95, thus $2.05 loss. I'm not upset about this one.

2) $50. Total loan was $500, in the Philippines. Debtor paid back $37.08, thus $12.92 loss. Annoyed by this, but still they paid back 74% of the loan, so I can't be too upset.

3) $25. Total loan was $900, in Ghana. Debtor paid back $23.25, thus a loss of $1.75. Not upset at this.

4) $25. Total loan was for $$1,000, in Lebanon. Debtor paid back $18.68, thus a loss of $6.32. Biggest 'loss' I've had so far on a loan. Still works out to 74% paid back.

I post this info, not to toot my own horn, but rather for others to see what it's like to make loans on Kiva. I will say that my stats are substantially more favorable than the total Kiva users. For example, I only had 0.122% losses due to default, whereas the total Kiva users have 1.76%. My currency rate loss works out to 0.000022%, whereas the total Kiva users have 0.32%. You better believe that the Default % of Kiva Partners is one of the first things I look at.

Started in Dec 2015.

Amount Lent: $18,900

Amount Defaulted: $22.97

Amount of Currency Rate Loss: $0.41 (unchanged from last year)

Total losses: $23.38

$23.38 / $18,900 = 0.001237 or 0.124%. (Note that this is lower than last year)

US inflation for the same time period was 9%.

So, I've made 690 loans, got the chance to help out at least that many people, and earned ~66k UR points for $23.38. Still not as great of a return as the prior year, but still a good deal in my book.

Defaulted loans: 4 total.

1) $25. Total loan was $8050 in Rwanda. Debtor paid back $22.95, thus $2.05 loss. I'm not upset about this one.

2) $50. Total loan was $500, in the Philippines. Debtor paid back $37.08, thus $12.92 loss. Annoyed by this, but still they paid back 74% of the loan, so I can't be too upset.

3) $25. Total loan was $900, in Ghana. Debtor paid back $23.25, thus a loss of $1.75. Not upset at this.

4) $25. Total loan was for $$1,000, in Lebanon. Debtor paid back $18.68, thus a loss of $6.32. Biggest 'loss' I've had so far on a loan. Still works out to 74% paid back.

I post this info, not to toot my own horn, but rather for others to see what it's like to make loans on Kiva. I will say that my stats are substantially more favorable than the total Kiva users. For example, I only had 0.122% losses due to default, whereas the total Kiva users have 1.76%. My currency rate loss works out to 0.000022%, whereas the total Kiva users have 0.32%. You better believe that the Default % of Kiva Partners is one of the first things I look at.

Jan 30, 2020 | 6:05 am

#1353

Moderator: Lufthansa Miles & More, India based airlines, India, External Miles & Points Resources

Join Date: Dec 2002

Location: MUC

Programs: LH SEN

Posts: 52,340

After nearly 10 years of investing and reinvesting 1000$ collected at SMD 1 & 2, I took a look at the stats this year, and the result is horrid:

Kiva has a very nonchalant attitude to the money it handles, its as if they are passing on monopoly money. The associated companies they lend to who who actually do the final microlending are rather shady and not vetted in advance or held accountable when things go bad. Sad situation.

Kiva has a very nonchalant attitude to the money it handles, its as if they are passing on monopoly money. The associated companies they lend to who who actually do the final microlending are rather shady and not vetted in advance or held accountable when things go bad. Sad situation.

Jan 31, 2020 | 9:57 am

#1354

Join Date: Aug 2008

Location: Somewhere in Florida

Posts: 2,876

We hit $8M today!!! WooHoo!!!

oliver2002 : In some respects I agree with you and in others I disagree. Kiva has managed to set up a platform where they have 0% of the risk and the investors carry 100% of it. It is too bad that they don't have at least a little skin in the game. Unlike other micro-lending sites, the only thing we stand to gain are miles/points and possibly a feeling of helping someone out. At best, we'll break even. Zero chance for positive returns.

At the same time, they do give you plenty of information to help guide your decisions. While the individual causes are important to me, using my money responsibly is more important when it comes to Kiva. I do know one of the defaulted loans I made wasn't the best business decision, but I liked what they were doing and probably would have outright donated to them if given the chance.

Here's a few of my guidelines I use with my own Kiva use:

1) Kivalens.org --- use it!

2) Partner age -- I only fund partners who have been around for at least 3 years, preferably longer.

3) Default rates -- I only do 0.3 or lower. Lower is definitely better here. There are some partners out there with 0% defaults, ie: they cover the losses from their own funds. I like these guys. Others are 0.03 or less.

4) DO NOT loan to anyone in a modern country, especially the USA. There are more sources for loans in the USA than anywhere. If someone can't get a loan through a traditional lender in the USA, there's a damn good reason -- STAY AWAY. The statistics for defaults of USA loans really drive this point home.

5) Look at how much the loan is for vs. economics of the country. If a single individual from a rural village in Rwanda wants $20k to sell high-end cosmetics, RUN AWAY. If same individual is in a decent-sized city, asking for $10k, then maybe. If they're in a rural village, asking for $5k for livestock and related essential items, winner.

5) Partner Risk Rating -- I only do 3.5 or higher. Not a hard rule and probably one of the least important factors in my process, but it's still part of the process.

If you think Kiva's rate of return is bad, you should take a look at Prosper / Lending Club. There's some real money pit loans to be had over there. I liked the concept, but waited to see what returns were before investing money there. I've not invested a single cent there.

oliver2002 : In some respects I agree with you and in others I disagree. Kiva has managed to set up a platform where they have 0% of the risk and the investors carry 100% of it. It is too bad that they don't have at least a little skin in the game. Unlike other micro-lending sites, the only thing we stand to gain are miles/points and possibly a feeling of helping someone out. At best, we'll break even. Zero chance for positive returns.

At the same time, they do give you plenty of information to help guide your decisions. While the individual causes are important to me, using my money responsibly is more important when it comes to Kiva. I do know one of the defaulted loans I made wasn't the best business decision, but I liked what they were doing and probably would have outright donated to them if given the chance.

Here's a few of my guidelines I use with my own Kiva use:

1) Kivalens.org --- use it!

2) Partner age -- I only fund partners who have been around for at least 3 years, preferably longer.

3) Default rates -- I only do 0.3 or lower. Lower is definitely better here. There are some partners out there with 0% defaults, ie: they cover the losses from their own funds. I like these guys. Others are 0.03 or less.

4) DO NOT loan to anyone in a modern country, especially the USA. There are more sources for loans in the USA than anywhere. If someone can't get a loan through a traditional lender in the USA, there's a damn good reason -- STAY AWAY. The statistics for defaults of USA loans really drive this point home.

5) Look at how much the loan is for vs. economics of the country. If a single individual from a rural village in Rwanda wants $20k to sell high-end cosmetics, RUN AWAY. If same individual is in a decent-sized city, asking for $10k, then maybe. If they're in a rural village, asking for $5k for livestock and related essential items, winner.

5) Partner Risk Rating -- I only do 3.5 or higher. Not a hard rule and probably one of the least important factors in my process, but it's still part of the process.

If you think Kiva's rate of return is bad, you should take a look at Prosper / Lending Club. There's some real money pit loans to be had over there. I liked the concept, but waited to see what returns were before investing money there. I've not invested a single cent there.

Jan 31, 2020 | 11:39 am

#1355

Original Poster

Moderator: American AAdvantage

Join Date: May 2000

Location: NorCal - SMF area

Programs: AA LT EXP; HH LT Diamond, Maître-plongeur des Muccis

Posts: 62,950

In 1,088 loans totaling $28,980.00 I’ve had $69.48 in currency losses and $740.79 in defaulted loans. I tend to make occasional loans with higher risks but high returns if the borrower succeeds. E.g. I knew lending to a furniture rebuilder in Nairobi’s Kibera neighborhood was risky due to instability and possibility of uprising, and unfortunately that’s what occurred. The borrower paid back part of the loan, but Kibera exploded into disorder.

I’m okay with that, honestly. And I’m glad Kiva has organized the technology at this end, the connections with local micro lenders at the other, and I believe they’ve aspired to keep that end clean. But I’ve been many places the micros operate, and in some cronyism, corruption, etc. are powerful streams they’re fighting in their up current swim.

I’m okay with that, honestly. And I’m glad Kiva has organized the technology at this end, the connections with local micro lenders at the other, and I believe they’ve aspired to keep that end clean. But I’ve been many places the micros operate, and in some cronyism, corruption, etc. are powerful streams they’re fighting in their up current swim.

Feb 1, 2020 | 8:59 am

#1356

Join Date: Sep 2012

Location: TPA/SRQ

Programs: Hyatt Explorer, Marriott Titanium, AA Plat Pro, UA Silver, Avis Plus, Hertz PC

Posts: 2,692

I just started. I have maybe 20 loans under my belt, I just dipped my toe in the water. I only did it when I noticed the AA moderator JDiver posted something, that ended up in my feed. Since he was always so helpful on that forum with the banal questions I and some others would ask. And it looked like a good way to help out.

In my short time what I have noticed is that women pay back better than men. I prefer loaning to agriculture or ongoing businesses, like resale and transportation. Like KRSW I have not loaned to a modern country. I have stayed mostly in Central/South America, Africa and have had a couple to the Baltics and Pakistan. What do they call it, the underbanked?

As per KRSW, I will start to use Kivalens. And I really appreciate ALL the advice I have seen in this thread. I wanted to step it up, but now I have more direction in choosing. I am not really worried about a little breakage since it seems like a worthy endeavor. I am glad I finally found it. It gives me something to do, on the computer besides arguing on Omni.

In my short time what I have noticed is that women pay back better than men. I prefer loaning to agriculture or ongoing businesses, like resale and transportation. Like KRSW I have not loaned to a modern country. I have stayed mostly in Central/South America, Africa and have had a couple to the Baltics and Pakistan. What do they call it, the underbanked?

As per KRSW, I will start to use Kivalens. And I really appreciate ALL the advice I have seen in this thread. I wanted to step it up, but now I have more direction in choosing. I am not really worried about a little breakage since it seems like a worthy endeavor. I am glad I finally found it. It gives me something to do, on the computer besides arguing on Omni.

Feb 5, 2020 | 11:34 am

#1357

Join Date: Apr 2010

Location: Unio Europaea

Programs: BA Gold, AS, Hertz Cirque Présidentielle

Posts: 1,448

I have been on Kiva for about 10 months now and all my lending has been in the name of the FT team. I haven't just posted in this thread to make myself visible.

So far I have invested in 222 loans and out of those the larger investments have been $XXX. I lend mainly to women, since I believe the entrepreneurial skills of women are important for solving the microeconomics in the 3rd world. To me it's not surprising that my top 3 countries are as follows:

El Salvador 22.52 %

Timor-Leste 14.41 %

Honduras 12.16 %

One can tell that I have flown to SAL and DIL.

I personally recommend lending to productive individuals that will use the capital for manufacturing new items, doing other manual labour or running a useful business. For instance I have loaned for beauty services only very selectively, while raising farm animals has always my backing (somekind of Victorian wisdom, I suppose). Also rendering food services is something I find constructive. I have avoided e.g. medical bills, because I think Kiva should be used to foster becoming financially empowered in a constructive way. My sentiment is very similar to the one of George Peabody. For a good/sensible cause, my coffers may provide up to XXX of dollars, since I then trust the loan will also be repayed. My only serious slacker has been a Ugandan woman, that wanted to buy items for her general store. I guess the energy saving bulbs vanished or something... The loan hasn't defaulted, but it's lagging behind badly. Either way, I didn't follow my doctrine, which I should've. Interesting to see what happens with a female Bolivian police officer, that wanted to lend for selling appliances. No, I don't expect honesty for being a law enforcement officer. I decided to see what happens when one loans $25 to a Bolivian police officer.

Looking forward to visiting more of the countries I lend to. Some of my countries are based on a big likelihood it will happen, it's just a matter of when.

Happy lending!

So far I have invested in 222 loans and out of those the larger investments have been $XXX. I lend mainly to women, since I believe the entrepreneurial skills of women are important for solving the microeconomics in the 3rd world. To me it's not surprising that my top 3 countries are as follows:

El Salvador 22.52 %

Timor-Leste 14.41 %

Honduras 12.16 %

One can tell that I have flown to SAL and DIL.

I personally recommend lending to productive individuals that will use the capital for manufacturing new items, doing other manual labour or running a useful business. For instance I have loaned for beauty services only very selectively, while raising farm animals has always my backing (somekind of Victorian wisdom, I suppose). Also rendering food services is something I find constructive. I have avoided e.g. medical bills, because I think Kiva should be used to foster becoming financially empowered in a constructive way. My sentiment is very similar to the one of George Peabody. For a good/sensible cause, my coffers may provide up to XXX of dollars, since I then trust the loan will also be repayed. My only serious slacker has been a Ugandan woman, that wanted to buy items for her general store. I guess the energy saving bulbs vanished or something... The loan hasn't defaulted, but it's lagging behind badly. Either way, I didn't follow my doctrine, which I should've. Interesting to see what happens with a female Bolivian police officer, that wanted to lend for selling appliances. No, I don't expect honesty for being a law enforcement officer. I decided to see what happens when one loans $25 to a Bolivian police officer.

Looking forward to visiting more of the countries I lend to. Some of my countries are based on a big likelihood it will happen, it's just a matter of when.

Happy lending!

Feb 5, 2020 | 11:56 am

#1358

Join Date: Apr 2010

Location: Unio Europaea

Programs: BA Gold, AS, Hertz Cirque Présidentielle

Posts: 1,448

That's a new one for me. Will look into what it does.

I was first thinking are you looking at the age of the debtors - especially *cough* the ladies.

Hear, hear.

True, for instance the ones needing money to repair their car (e.g. a taxi) will need more, while lending to cosmetics is risky. I know beauty is in demand in all parts of the world, but honestly speaking it's not a sensible business everywhere. Overall it anyway falls under the category of not being maybe as much of constructive financial self-help as I'd like it to be, but indeed, I've lended to such cases as well and so far the selected ones have paid as expected. *knock, knock* I do however approve the lending reasoning when e.g. an existing hairdresser/barber wants to improve their shop or get more stuff. Then there's an actual business sentiment there. Miss X just wanting to become an entrepreneur with $2000 of cosmetics in e.g. Rwanda or Nicaragua is just *cough* outright ludicrous, where as miss Z and her pupusas in El Salvador is absolutely bueno - too bad I can't have the interest paid in ones and delivered to my home.

4) DO NOT loan to anyone in a modern country, especially the USA. There are more sources for loans in the USA than anywhere. If someone can't get a loan through a traditional lender in the USA, there's a damn good reason -- STAY AWAY. The statistics for defaults of USA loans really drive this point home.

5) Look at how much the loan is for vs. economics of the country. If a single individual from a rural village in Rwanda wants $20k to sell high-end cosmetics, RUN AWAY. If same individual is in a decent-sized city, asking for $10k, then maybe. If they're in a rural village, asking for $5k for livestock and related essential items, winner.

Feb 5, 2020 | 11:43 pm

#1359

Senior Moderator and Moderator: American AAdvantage & TravelBuzz

Join Date: Nov 2007

Location: BOS

Programs: AA EXP, Marriott Titanium

Posts: 10,673

I just started. I have maybe 20 loans under my belt, I just dipped my toe in the water. I only did it when I noticed the AA moderator JDiver posted something, that ended up in my feed. Since he was always so helpful on that forum with the banal questions I and some others would ask. And it looked like a good way to help out.

I'm hoping to hit my next personal lending "milestone" the latter half of this year, and I have JDiver to thank for getting my started on Kiva.I've been on Kiva a little bit now, and I've been fortunate enough to get semi-regular updates from their management team and occasionally have the chance to pop out to their offices to meet with their teams for a day. I know we all lend for different reasons, but I wanted to share a couple thoughts and tidbits for consideration...

- Yes, like with any business or platform, there are occasionally the bad nuts. Kiva does do regular audits of their microfinancing partners; those who are "fail" are kicked off the platform. Others are put on probation and given some guidance on how to improve. There are Kiva Fellows who are on the ground around the world who check in with these partners, not only to provide guidance/assistance but also to spot-check for compliance. (These fellows will pick a random set of loan recipients and do surprise checks to ensure that 1) these individuals actually exist, 2) they're actually working with the local partners, 3) the funds disbursed are actually being used for the stated purpose.)

- All of us loan for different reasons. If you're expecting market returns, you should probably resort to more "classic" investing instruments. However, just like regular financial services, if you chose to invest in "bad" entities or take on greater risk, don't be surprised if you suffer larger losses. I won't belabor this point.

- I would ask folks to keep in mind Kiva's core goal: to serve the underbanked and provide opportunities to those who are most vulnerable. This fundamentally means that risk needs to be taken. I'll share a conversation I had a few years ago with the Kiva team. We were discussing the default rate and the fact that it was about 1.5-2%. You might think we talked about ways to lower that number, but in fact, we discussed why that number actually needed to be *higher*! You see, if you make only low-risk loans, you're really not serving the most vulnerable. You're serving the lowest-hanging fruit who are already most likely to be able to get credit and repay loans.

- Reaching individuals in the most impoverished and rural neighborhoods is expensive - it can take a full day of travel just for a loan officer to visit a client to collect a loan repayment. That's part of the reason why you'll see the interest rates be so high for some customers. These partners are also often providing more than just a loan. They're providing education on budgeting, savings, and marketing. They're helping develop cooperatives and increase the use of technology to ensure clients are getting the best prices. This all costs money. By providing zero-interest loans, we are already help cut out some of the costs that would otherwise have to be passed to the borrowers.

- To truly reach those who are the most vulnerable involves making loans to those in war-torn countries, seeking out refugees, reaching populations who have never traded with money and now are learning a completely new world. This involves risk. These are the folks who are most in need - but also more likely to not be able to repay. So Kiva is finding the difficult balance between promoting their core mission whilst trying to be responsible stewards of a two-sided platform. They know that they may one day push too far and suddenly the flow of monies available for loans starts to decline...and that would obviously be detrimental to their mission.

Anyway, congrats to the team for making it to $8MM already! Onwards and upwards.

Feb 6, 2020 | 10:30 am

#1360

Original Poster

Moderator: American AAdvantage

Join Date: May 2000

Location: NorCal - SMF area

Programs: AA LT EXP; HH LT Diamond, Maître-plongeur des Muccis

Posts: 62,950

It’s impressive how you’ve followed up, attended meetings, met with Kiva execs. Thank you, JY1024, for your thorough follow up and for taking the time to share.

Feb 6, 2020 | 10:21 pm

#1361

Join Date: Apr 2005

Location: Cambridge, MA

Programs: AAdvantage PP

Posts: 285

Does anyone know how kiva decides when a loan will move from delinquent to default? I have one that's been "paying back delinquent" for the past 7 months (final repayment scheduled for July 1, 2019, only part repaid, no action since). I'm not too upset - this would be my first default out of 72 loans if/when it happens, and my $1.55 is likely making more of a difference for someone in the current situation in Lebanon than it would back in my hands. I'm just curious how the decision is made that there's no more hope of getting paid back.

Mar 30, 2020 | 2:29 pm

#1362

Join Date: Aug 2001

Location: SFO

Programs: AC SE, AA EXP MM, BAEC Gold, UA Gold MM, Hyatt Glob, Marriott Titanium, HH Dia, IHG Plat

Posts: 4,940

Covid-19 Impact?

It's surprising there haven't been any posts on this topic. Are Kiva operations currently restricted due to travel bans and repatriation? Are repayment rates starting to fall?

Mar 31, 2020 | 9:15 pm

#1363

Join Date: Nov 2010

Location: ONT

Programs: AGR, UA, AA

Posts: 476

My default rate was already relatively high (1.37%) but I don't think it has increased substantially. If all delinquent loans remain unpaid (they won't) that number would go up to 2%. Some of the US based borrowers are still making payments as of a couple of days ago. Due to higher interest rates a couple years ago, along with easier Plastiq unloading, I had greatly downsized my use of Kiva for MS in 2019. Even with the change to disallow gift cards on Plastiq, I still never ramped up because I knew the economy could turn south (although I was thinking of a general bubble burst, not this). Due to crisis I'm going to Costco more often which means I unload my VGC bought at a discount there, and for regular spend.

Apr 12, 2020 | 10:14 pm

#1364

Senior Moderator and Moderator: American AAdvantage & TravelBuzz

Join Date: Nov 2007

Location: BOS

Programs: AA EXP, Marriott Titanium

Posts: 10,673

- Kiva Fellows scattered around the world are following the guidance of their respective governments re: returning home and/or quarantining.

- Some microfinancing institutions/partners have already announced that they are tentatively suspending loan repayments, as they do not want to endanger their staff nor borrowers with their usual in-person collections.

I'd suspect that delinquencies will start to rise. Unclear if defaults will increase in the long-term (though I suspect they will), as defaults are a lagging indicator to delinquency rates.

Apr 23, 2020 | 10:39 am

#1365

Join Date: May 2016

Posts: 19

FYI: Almost 40% of scheduled repayments were missed this month. Most of my loans are in Asia, Central America, and South America.

As always, if you want to avoid delinquency and default, don't lend in Africa, except for Senegal. Do not lend in US.

Don't expect defaults to rise anytime soon. I had people stop paying for 18 months and the loans were still not counted as defaulted.

5/4/2020 update... my delinquency rate shot up to 40%. Kiva is basically dead for a while.

As always, if you want to avoid delinquency and default, don't lend in Africa, except for Senegal. Do not lend in US.

Don't expect defaults to rise anytime soon. I had people stop paying for 18 months and the loans were still not counted as defaulted.

5/4/2020 update... my delinquency rate shot up to 40%. Kiva is basically dead for a while.

Last edited by dogeatdog; May 4, 2020 at 1:19 pm