UA Q4/Full Year 2017 Results/Conference Call 23 Jan 2018

Jan 26, 2018, 1:51 pm

Jan 26, 2018, 1:51 pm

#77

Join Date: Feb 2008

Programs: 6 year GS, now 2MM Jeff-ugee, *wood LTPlt, SkyPeso PLT

Posts: 6,526

We have the CS100 and CS300 payrates in the current contract. CS100 is the same as E190/E195. The CS300 payrate is the same as the A319 and 737-700. (That's what the 'paybanding' means) There's also a payrate for the CRJ900 which is the lowest payrate in the current contract.

If they added the CS100 or E190/E195 the current SCOPE would allow them to add additional 70/76-seaters operated by regional airlines. They could add an unlimited number of 70/76-seat airplanes as long as United pilots flew them. We have a rate for the CRJ-900. The similarly-sized E170/175 is not covered but the procedure for adding a fleet that isn't listed is covered. The procedure allows for the process to be completed within 180 days included binding arbitration, if necessary, and specifically says that it will not prevent the company from introducing the new aircraft before an agreement is reached. They can introduce the new aircraft paying no less than the lowest existing rate which is the CRJ-900 rate. Obviously, they don't want to pay us that rate to fly those airplanes.

Delta has the CS100 on order and their payrate is 18%-19%, depending on longevity, HIGHER than the rate in the United pilot agreement. UAL could put them online ASAP and operate then at a nearly 20% discount to DAL on the pilot rates.

He hasn't given specifics. One can only speculate that he wants to be able to fly more 70/76-seaters at regional airlines than the current SCOPE allows.

If they added the CS100 or E190/E195 the current SCOPE would allow them to add additional 70/76-seaters operated by regional airlines. They could add an unlimited number of 70/76-seat airplanes as long as United pilots flew them. We have a rate for the CRJ-900. The similarly-sized E170/175 is not covered but the procedure for adding a fleet that isn't listed is covered. The procedure allows for the process to be completed within 180 days included binding arbitration, if necessary, and specifically says that it will not prevent the company from introducing the new aircraft before an agreement is reached. They can introduce the new aircraft paying no less than the lowest existing rate which is the CRJ-900 rate. Obviously, they don't want to pay us that rate to fly those airplanes.

Delta has the CS100 on order and their payrate is 18%-19%, depending on longevity, HIGHER than the rate in the United pilot agreement. UAL could put them online ASAP and operate then at a nearly 20% discount to DAL on the pilot rates.

He hasn't given specifics. One can only speculate that he wants to be able to fly more 70/76-seaters at regional airlines than the current SCOPE allows.

Bombardier wins big over Boeing in trade dispute - Jan. 26, 2018

Bombardier wins big over Boeing in trade dispute - Jan. 26, 2018So taking stock, Boeing made a bunch of ridiculous arguments, which the Trump Admin followed, which caused Airbus to Buy the c100/c300 line, making them a fearsome competitor, putting Boeing in a weaker position. At some point Boeing is going to have to start making good A/C that passengers prefer, rather than playing politics all the time.

Jan 26, 2018, 2:29 pm

#78

Join Date: Apr 2011

Programs: WN, AA, UA, DL

Posts: 1,313

I'm curious. From a passenger perspective, would you consider the 199-seat DL 757 "junky"? Ignore the AVOD angle for a second. Judge it based on layout, space, and comfort.

Jan 26, 2018, 2:48 pm

#79

Join Date: Jan 2005

Location: New York, NY

Programs: UA, AA, DL, Hertz, Avis, National, Hyatt, Hilton, SPG, Marriott

Posts: 9,452

Well, I prefer it to Delta's 739, because DL's slimlav layout on that airplane is terrible. But the midlav on the 757 sits smack in the middle of C+, so that's no picnic, either. I actually prefer UA's 739 configuration to both.

Jan 26, 2018, 4:25 pm

#81

Join Date: Feb 2008

Programs: 6 year GS, now 2MM Jeff-ugee, *wood LTPlt, SkyPeso PLT

Posts: 6,526

But hey, I much prefer the 757, even in DL's rather strange 20 F configuration to any 739. This said, I much prefer the A321 to either. In AA or DL or VX configuration its a much, much nicer plane. Width is nice and the overhead bins don't take up so much space.

But hey, I much prefer the 757, even in DL's rather strange 20 F configuration to any 739. This said, I much prefer the A321 to either. In AA or DL or VX configuration its a much, much nicer plane. Width is nice and the overhead bins don't take up so much space.The 737-900 is a total piece of junk.

Jan 26, 2018, 5:28 pm

#82

Join Date: Jun 2010

Location: Florida

Programs: United 1K, Marriott Ambassador, Hilton Gold

Posts: 673

Jan 27, 2018, 3:09 pm

#83

Join Date: Mar 2011

Location: Canada

Programs: Star Alliance G*, Marriott Bonvoy Titanium,

Posts: 3,585

United Expansion Hits Airline Shares

This from WSJ January 25, 2018:

https://www.wsj.com/articles/airline...ans-1516820046

Per FT Rules on external links

WSJ has a paywall

https://www.wsj.com/articles/airline...ans-1516820046

Per FT Rules on external links

Jan 24, 2018

Airline shares tumbled on Wednesday as investors fretted that United Continental Holdings Inc.’s expansion plans threatened profit margins and could spark a price war if other carriers follow suit.

Airline shares tumbled on Wednesday as investors fretted that United Continental Holdings Inc.’s expansion plans threatened profit margins and could spark a price war if other carriers follow suit.

Last edited by WineCountryUA; Jan 27, 2018 at 3:54 pm Reason: added content per FT Rules; add to existing thread covering the topic

Jan 28, 2018, 7:25 am

#84

FlyerTalk Evangelist

Join Date: Mar 2010

Location: DAY

Programs: UA 1K 1MM; Marriott LT Titanium; Amex MR; Chase UR; Hertz PC; Global Entry

Posts: 10,159

I didn't get to listen to the entire call, but what I heard about the 50 seaters and "small" markets was a hoot.

They just decimated my DAY service, removing all 2 cabin planes that were standard on ORD, and had been increasing to other hubs. All 50 seaters now. And AA and Delta both have multiple mainline ops every day. Hardly competetive.

I started flying out of CVG to avoid the CR2s, and now my costs have gone down as I am seeing lower fares.

I fear they are going to be disappointed by their plan to have the Devil's Chariot be the solution to their yield issues.

I will try to listen to the entire call later tonight to see if I missed anything, though.

I was was also struck by "natural share" discussion, which sounded a lot like "we don't need to compete for business".

...

DAY again. For 2017, both UA and DL (even mainline) are shrinking at DAY. AA is the largest and is up slightly. Much of the declines at DAY are undoubtedly due to competition returning to CVG, lowering fares there, and reversing CVG leakage to DAY.

UA still has 2-class RJs to ORD at comparable levels going back quite a few years.

AA has only two mainline flights, and DL has only four mainline flights, both going to one hub each in directions UA doesn't compete with them on.

UA's traffic decline predates the inclusion of CRJs replacing E145s.

UA recently announced a return to IAH, something I mentioned previously was their biggest hole at DAY.

...

DAY again. For 2017, both UA and DL (even mainline) are shrinking at DAY. AA is the largest and is up slightly. Much of the declines at DAY are undoubtedly due to competition returning to CVG, lowering fares there, and reversing CVG leakage to DAY.

UA still has 2-class RJs to ORD at comparable levels going back quite a few years.

AA has only two mainline flights, and DL has only four mainline flights, both going to one hub each in directions UA doesn't compete with them on.

UA's traffic decline predates the inclusion of CRJs replacing E145s.

UA recently announced a return to IAH, something I mentioned previously was their biggest hole at DAY.

...

Just because you keep saying it, it does not make it true...and I am tired of arguing with you about it. I have lived it.

DAY<->ORD on a 2 cabin plane seems to be down to one turn a week...Tuesday afternoons. Everything else seems to be 1 cabin.

That is a drastic reduction in 2-cabin service over the past several years.

And the other routes which used to see 2 cabin -DEN on most days, and the occasional IAD, are all 50 seaters now.

mduell - do you have time to run the schedule on this? I don't know of any other way to prove the obvious.

Oh, and sure, it is nice to see DAY<->IAH be added back this summer...but we are looking at an almost 3 hour flight on a 50 seater, so not like this is a groundbreaking.

DAY<->ORD on a 2 cabin plane seems to be down to one turn a week...Tuesday afternoons. Everything else seems to be 1 cabin.

That is a drastic reduction in 2-cabin service over the past several years.

And the other routes which used to see 2 cabin -DEN on most days, and the occasional IAD, are all 50 seaters now.

mduell - do you have time to run the schedule on this? I don't know of any other way to prove the obvious.

Oh, and sure, it is nice to see DAY<->IAH be added back this summer...but we are looking at an almost 3 hour flight on a 50 seater, so not like this is a groundbreaking.

I'm not saying because I'm saying it. I'm saying it because it's what the BTS and Dayton Airport stats tell us. I'd be on board with you if that's what the stats show. UA hasn't had drastically more 2-class service on ORD-DAY for many years. And it's ironic that mduell shows you that 2017 had more 2-class service than 2016. ORD-DAY has been a mix of 2-class and 50-seaters for over a decade. Mainline left in 2009, and the RJ mix has been similar for even longer.

IAD-DAY had some 2-class service many years ago, but that was also limited. The overall DAY mix has been in the 50/50 to majority 50-seater range for a long time. The mix has been more favorable to 2-class lately, although overall traffic has been in decline for years. But that has been true for most carriers at DAY. Interestingly mainline traffic has also dropped over the past five years with DL and AA. It'as not a UA thing. It's primarily a DAY/CVG thing. Even if UA gets more 2-class RJs, I wouldn't expect a dramatic increase in service to DAY. That ship appears to be sailing down I-75. Maybe the new focus on small markets will stem the tide in the next few years, but don't expect mainline to suddenly dominate.

IAD-DAY had some 2-class service many years ago, but that was also limited. The overall DAY mix has been in the 50/50 to majority 50-seater range for a long time. The mix has been more favorable to 2-class lately, although overall traffic has been in decline for years. But that has been true for most carriers at DAY. Interestingly mainline traffic has also dropped over the past five years with DL and AA. It'as not a UA thing. It's primarily a DAY/CVG thing. Even if UA gets more 2-class RJs, I wouldn't expect a dramatic increase in service to DAY. That ship appears to be sailing down I-75. Maybe the new focus on small markets will stem the tide in the next few years, but don't expect mainline to suddenly dominate.

If you have DATA showing something different, post it. Otherwise, you have lost credibility on this.

Overall, Kirby was very specific about the connectivity issue being key to increasing yields - that United needs to compete for small market share when there is competition.

I maintain that throwing CR2s against 2-cabin RJs and Mainline is not a winning strategy.

Jan 28, 2018, 9:12 am

#85

Join Date: Feb 2002

Location: NYC: UA 1K, DL Platinum, AAirpass, Avis PC

Posts: 4,599

You have denied UA had more 2 cabin service in previous years. mduell was kind enough to post the data that proves you are not correct.

If you have DATA showing something different, post it. Otherwise, you have lost credibility on this.

Overall, Kirby was very specific about the connectivity issue being key to increasing yields - that United needs to compete for small market share when there is competition.

I maintain that throwing CR2s against 2-cabin RJs and Mainline is not a winning strategy.

If you have DATA showing something different, post it. Otherwise, you have lost credibility on this.

Overall, Kirby was very specific about the connectivity issue being key to increasing yields - that United needs to compete for small market share when there is competition.

I maintain that throwing CR2s against 2-cabin RJs and Mainline is not a winning strategy.

For example if you want to go ILM-SAN and want a travel time under 8 hours...

Theres

ILM-ATL 6am

ILM-IAD 10:30am

ILM-CLT 2:20pm

ILM-ATL 4:55pm

ILM-ATL 6:20pm

So UA slotted in during an 8 hour gap in the schedule. The prime time slots are taken but if you happen to be someone who doesn�t want the ultra early wake up UA is your choice.

Then let�s look at long haul like ILM-GRU

If you want just one stop there�s

6:05pm ATL - 2 hr layover

7:55pm IAD - 1hr layover

Riskier connection here but it gives more time working in ILM and shows up higher in search results (shorter ttrip). More important - only 2 airlines not 3 duking it out.

Bismarck - NYC

5am DL 2 cabin

6:20 UA single

6:55am DL 2 cabin

10:55 DL 2 cabin

12:55 UA 1 cabin

1:20 DL 1 cabin

3:20 AA 2 cabin

5:39 DL 2 cabin

Not great on the early morning - fills a hole during the midday when DL is running single cabin.

Will it achieve his numbers? No idea - clearly we all would rather see 2 cabin on every route - but it�s not as cut and dry as throwing single cabin planes on saturated routes like ORD-NYC.

Jan 28, 2018, 9:22 am

#86

FlyerTalk Evangelist

Join Date: Jun 2001

Programs: DL 1 million, AA 1 mil, HH lapsed Diamond, Marriott Plat

Posts: 28,190

For kicks let's say it a different way isolated on the revenue side of the equation. For the average UA flyer at the average UA stage length (1,460 mi), it means UA flyers paid $221.92 instead of $242.50 to travel from point A to point B, and they did it more reliably to boot. UA is a good deal.

Jan 28, 2018, 12:59 pm

#87

Join Date: Jan 2007

Location: Bellingham/Gainesville

Programs: UA-G MM, Priority Club Platinum, Avis First, Hertz 5*, Red Lion

Posts: 2,808

For kicks let's say it a different way isolated on the revenue side of the equation. For the average UA flyer at the average UA stage length (1,460 mi), it means UA flyers paid $221.92 instead of $242.50 to travel from point A to point B, and they did it more reliably to boot. UA is a good deal.

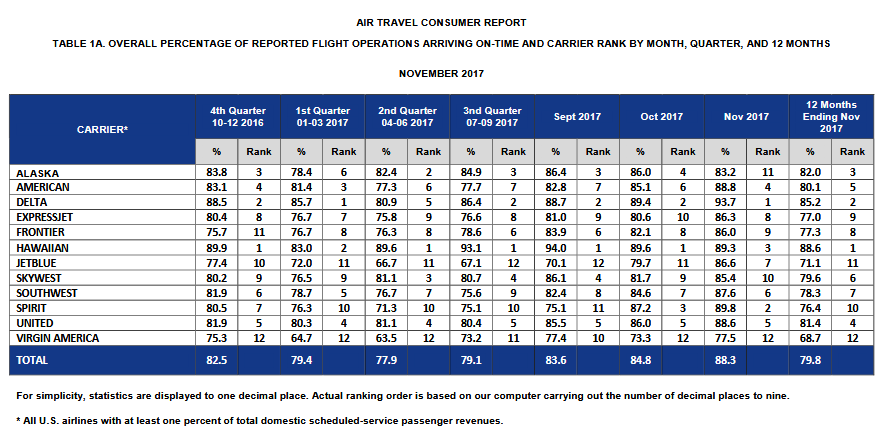

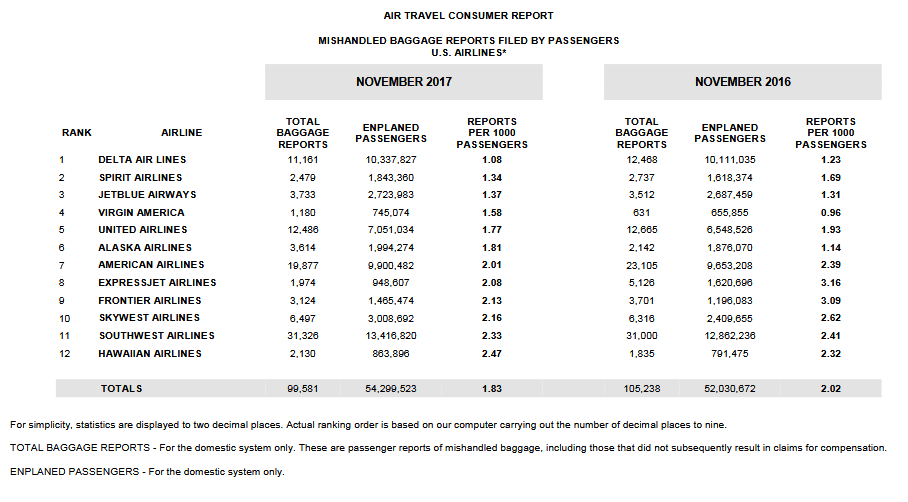

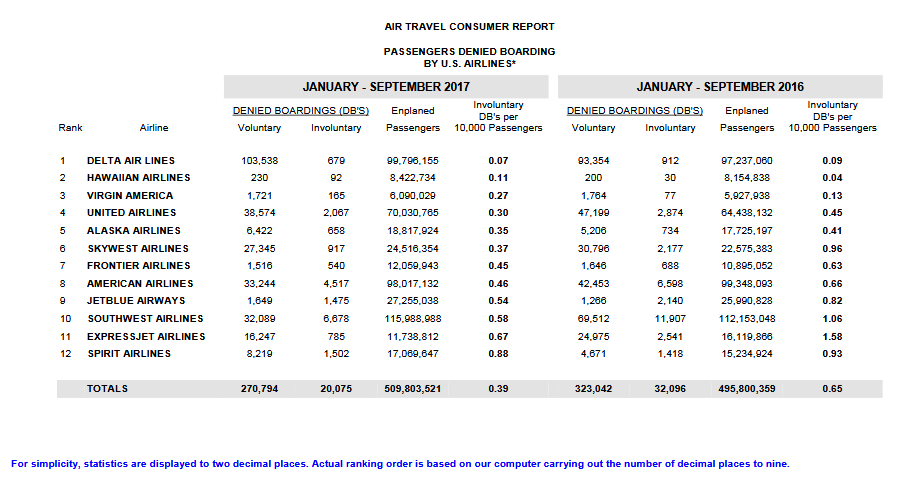

- lower OTA

- greater chance of IDB

- Higher bag mishandling rate

Jan 28, 2018, 2:17 pm

Jan 28, 2018, 2:17 pm

#89

Suspended

Join Date: Aug 2017

Programs: Rapid Rewards, AAdvantage, SkyMiles

Posts: 2,931

I read somewhere that UA admitted they were losing money with Basic Economy and that they were going to change it up a bit, including giving passengers the benefit of paying for seat assignments/upgrades. Was this mentioned in this conference call or did I get this info from somewhere else?

Jan 28, 2018, 2:19 pm

#90

Join Date: Apr 2011

Programs: WN, AA, UA, DL

Posts: 1,313

You have denied UA had more 2 cabin service in previous years. mduell was kind enough to post the data that proves you are not correct.

If you have DATA showing something different, post it. Otherwise, you have lost credibility on this.

Overall, Kirby was very specific about the connectivity issue being key to increasing yields - that United needs to compete for small market share when there is competition.

I maintain that throwing CR2s against 2-cabin RJs and Mainline is not a winning strategy.

If you have DATA showing something different, post it. Otherwise, you have lost credibility on this.

Overall, Kirby was very specific about the connectivity issue being key to increasing yields - that United needs to compete for small market share when there is competition.

I maintain that throwing CR2s against 2-cabin RJs and Mainline is not a winning strategy.

Let's revisit a December post of yours, where you claim UA is ceding market share. Now again you don't have evidence to back it up, and you make inference that it goes beyond the IAD/EWR-DAY specifically talked about (ZW doesn't even fly EWR-DAY). So as a data point of interest, let's take all of DAY and see what UA's share of traffic has been there since 2012, the first year of fully combined UA/CO ops (starting with that year): 17.4%, 17.9%, 17.4%, 18.3%, 17.6%, 17.0%. mduell's table indicates about a 10% increase in capacity this year, so they could have their largest share there this year since after the merger, meaning UA is planning to compete for more DAY market share. I guess we will find out as the year goes on whether your belief that it won't increase market share isn't a "winning strategy". Either way UA has had a very consistent market share at DAY in the past 6 years, providing evidence that the issue isn't UA for shrinking schedules, it's DAY demand as a whole. As a whole airlines are shrinking there.

Another way of interpreting the fare data is that a hundred million passengers were willing to pay, on average, $20 more to fly Delta than to fly United. What is it about the Delta vs. UA experience? What is UA doing to improve wage (specifically) and total cost productivity to be profitable with that headwind? These would be uncomfortable questions for UA execs.

Ironically a lack of choice is a key factor in who pays more for the "privilege" of flying certain carriers. And a simple hypothetical question tells us that in a commodity market that the "experience" has little to do with it, unless we're talking about negative operational "experiences", in which case DL has had many troubles lately. Let's ask a hypothetical question in a simple market. Let's say DL raises their prices to be $20 over a directly competing carrier (a generic UA), in this case a fixed $240 instead of a fixed $220. The demand in this certain market at a fixed $220 price level is a combined 80% load factor, meaning there is excess capacity available. In this example, the exact load factor ratio between the two at the $220 price level doesn't matter. After DL universally raises their price to $240, do you believe their load factor would hold constant and their PRASM would increase by that 9% yield increase, holding every else constant, including the same basic service (transportation) and product that DL offers now? Or is it conceivable that the competing airline would gain load factor and possibly PRASM?

P.S. UA's is doing remarkably well on the cost side versus DL and AA. Not sure how they're doing it, but the difference was large in Q4.