Jan 2, 2019, 9:51 am

Jan 2, 2019, 9:51 am

Last edit by: danpeake

As of Nov 11, 2020, Meta gebits are getting declined when used for MO/BP purchases at MC/SD. New limit appears to be $99 per swipe with some metas at some stores. READ the posts below and add a data point with details. USB and GD gift cards do not seem to be affected.

As of Nov 11, 2020, Meta gebits are getting declined when used for MO/BP purchases at MC/SD. New limit appears to be $99 per swipe with some metas at some stores. READ the posts below and add a data point with details. USB and GD gift cards do not seem to be affected.

This is the thread for 2019. The previous discussion can be found here: https://www.flyertalk.com/forum/manu...rt-2018-a.html

New to MO: Read this entire Wiki (Click to open) and all posts for some tips before asking common questions. It is best to know what you are doing before you try.

Note: The policy for allowing gift cards as payment for money orders can be more restrictive with certain stores or certain clerks. Just because an employee says there's a new restrictive policy "for all Walmarts" means nothing. There are plenty of cases where the employee is incorrect and the new policy is only regional or store specific.

---------------------------------------------------------------------------------

Tested Gebit (gift debit) cards:

1. DO NOT WORK - Any Vanilla product affiliated with InComm or ITC Financial Services will not work for swipes over $49.99.

2. See above on Visas issued by MetaBank. New limit appears to be $99 per swipe with some metas at some stores. Follow the posts below for the latest information.

3. MC issued by US bank OR Metabank MC (Giftcards.com) can work, but you need to change payment type to debit before they enter the amount in the register. See below for details.

4. Gdot/sun work but take about an hour to activate.(VGC issued by Sunrise also limited to $99/swipe, same as Metabank issued cards, and Sunrise was available immediately).

5. USB work

__________________________________________________ __________________________________________

NEW Limits as of 11/18 - 8K with ID every 24 hours. ID required for MO over 1K.Some tips for starting out:

All WM registers allow 4 debit swipes per transaction, but YMMV per store and cashier. Refer to cards as Debit cards.

Start slow and buy one MO with one Gebit to see how it works. Refer to cards as Debit, only this community calls them Gebits. Your store or cashier may have rules that other stores do not have, only allowing one swipe per trans or up to 4 swipes per trans. Read all the tips below and all the posts below before trying more advanced transactions. NO variety or design of VISA or MC Gebit's will ever auto-drain at Walmart so always tell them the amount you want to pay per card. Fee: 1K MO or less is usually 88 cents each, but ask or check the wall. Subtract the fee from the total or pay in cash. If a store says "no", thank them and try again another day with a different clerk.

Helpful details and tips for advanced transactions:

1. Cost: 1K MO fee is usually $1 each(Some states limit MO total to 750 or 950 and may have a different fee). Subtract fee from your total or pay in cash. Can buy two 1K MO in one transaction with 4 swipes for $1 x 2 in most states. NO variety or design of VISA or MC Gebit's will ever auto-drain at Walmart so always tell them the amount you want to pay per card.

2. Split payment transactions: You cannot successfully swipe more than 4 cards in a single transaction. If the cashier screws up and enters $50.00 instead of $500.00 (thus making it impossible for 4 swipes to complete the transaction), the transaction will need to be canceled. The funds should return to your cards right away but may take 24 hours, so note the time and person helping you. When a transaction is canceled during the trans, the money returns to the cards. If canceled after, the cash reg drawer opens and they pay you back in cash.

3. Split payment: The amount of each swipe needs to be entered by the cashier. Ask to "split the payment by $$$". The Gebit must have current balance of that amount or more otherwise slip with Error 51 will print out. Warning: (YMMV) It appears (my experience on 3 occasions during prepaid card load and buying MO in 2 different WMs) that after the debit card was charged no cash could be credited back to the card. Cashier should issue cash back. Keep the slip and contact manager if in doubt. Remember date, time and register if no slip.

4. Bad Printer: IF, by chance, you've swiped your GCs successfully, a receipt prints but the MO doesn't, make sure to ask to see the receipt and check near the bottom IF it says CHANGE/REFUND with a negative sign before the amount of GCs you swiped, that means the cashier must give you cash refund. Cashier may have to call for the cash dept manager to verify the refund. Some stores may outright give your cash refund immediately while there are others that will ask you to come back. Think twice before you buy MOs while on vacation or when you're in unknown to you territories for issues like this.

6. MCGC liquidation- The cashier should not enter the amount first. Technically they just can't hit enter after entering the amount. Let the CSR know you need to swipe first and switch the payment type to debit, then swipe and hit "Cancel" or "Change Payment" to select "Debit" on the screen, enter the pin and have them enter the amount.

7. SSN/ID entry - Any MO purchases in one transaction at or over $3K requires you to input your SSN. Any MO at or over $1K requires ID input (and ID requirement can also be forced by cashier at any amount).

Debit codes PDF

http://www.flyertalk.com/forum/attac...0&d=1461170080

Buying Money Orders at Walmart (2019 - 2022)

Nov 21, 2019, 1:02 pm

#1561

Join Date: Apr 2014

Posts: 303

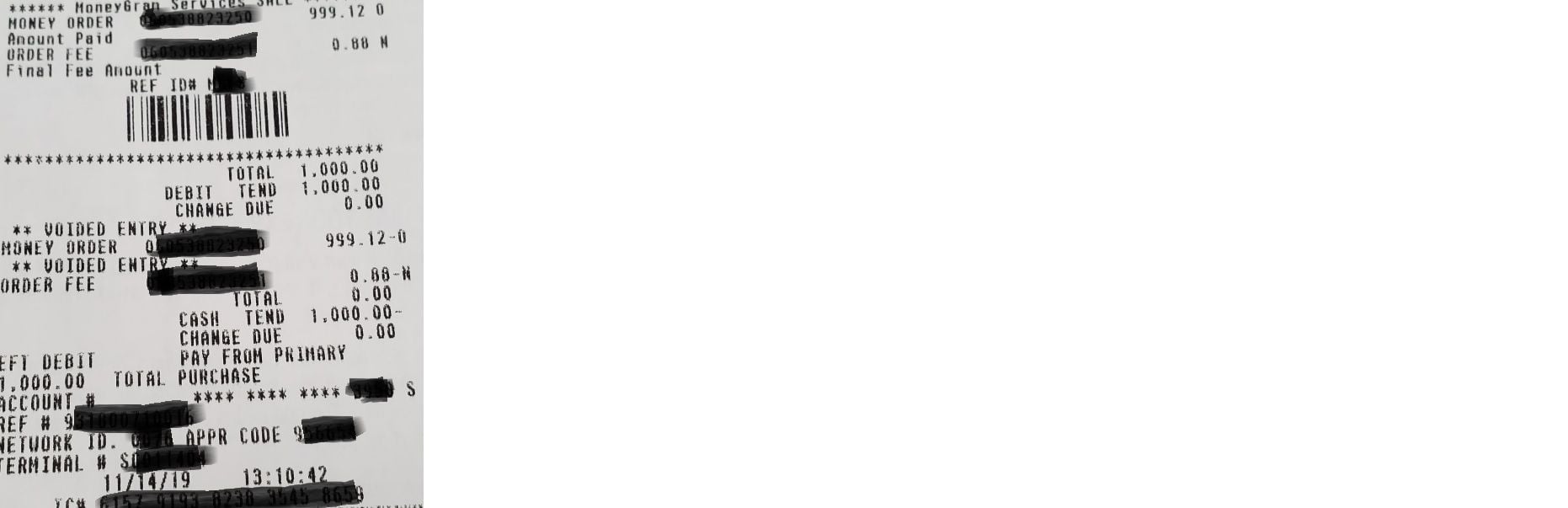

Hi I've purchased a MO a week ago using a SM $1k GC and the transaction didnt complete in printing the MO as per attached receipt image, where there are voided entry messages and transaction should have been reversed but the GC was charged for the full $1k amount. The money has not been refunded to the GC after 5 business days today and having gone back to the store is giving a hard time and is saying to wait a further 5 business days before coming back even though already 5 has passed in case a refund automatically comes back which I dont think will.

They were also insisting on a "bank statement" or wont do anything and is saying wont accept the printout I showed from the GC website and when I called the card customer service has said that since theres no real bank account connected there is no such thing that can be provided. Will try to argue again when go back (hopefully some other manager will be there), but does anyone here by chance know if theres another kind of statement that can be provided besides just what comes up on the check balance page of the GC?

I'm confused if based on the image, "CASH TEND" shows $1,000, which may suggest that the refund was to be given back to me in cash?

Looks like if they still dont cooperate when I go back next week will have to start a long winded dispute with the GC. These hassles are driving me to lay off this activity!

They were also insisting on a "bank statement" or wont do anything and is saying wont accept the printout I showed from the GC website and when I called the card customer service has said that since theres no real bank account connected there is no such thing that can be provided. Will try to argue again when go back (hopefully some other manager will be there), but does anyone here by chance know if theres another kind of statement that can be provided besides just what comes up on the check balance page of the GC?

I'm confused if based on the image, "CASH TEND" shows $1,000, which may suggest that the refund was to be given back to me in cash?

Looks like if they still dont cooperate when I go back next week will have to start a long winded dispute with the GC. These hassles are driving me to lay off this activity!

Nov 21, 2019, 1:06 pm

Nov 21, 2019, 1:06 pm

#1562

Join Date: Sep 2019

Posts: 317

Your receipt says "CASH TEND 1,000.00-"

That means you were supposed to be handed $1,000 in cash. You weren't. That's the clerk's mistake. There isn't going to be any credit to your Simon card. Show the receipt to a manager.

That means you were supposed to be handed $1,000 in cash. You weren't. That's the clerk's mistake. There isn't going to be any credit to your Simon card. Show the receipt to a manager.

Nov 21, 2019, 1:14 pm

#1563

Join Date: Apr 2014

Posts: 303

Thanks for confirming, the "manager" was trying to claim all of what I described but when go back will surely insist on "CASH TEND" and they can see the recorded video if wants to as proof! Plus the cashier did this transaction was in the store and knows I wasnt given any cash.

Nov 21, 2019, 1:31 pm

#1564

Join Date: Sep 2019

Posts: 317

You're welcome. Also, the drawer pops open at that point so the CSR can give you the cash. That should be visible on the video too.

Nov 21, 2019, 1:43 pm

#1565

Join Date: Mar 2009

Posts: 2,295

That's classic cash refund right there. Hope you get this straightened out. For future, when the receipt says "CASH TEND" and the drawer pops open, demand cash.

Nov 21, 2019, 4:11 pm

#1566

Join Date: Oct 2010

Location: DFW

Posts: 684

Also that drawer should be $1000 over for Nov. 14th. Should be easy for them to check that.

Nov 21, 2019, 5:00 pm

#1567

Join Date: Oct 2004

Programs: Amtrak Guest Rewards, Starwood Preferred Guest, Marriott Rewards, Hilton Honors

Posts: 255

Please keep us posted on how it goes. It's a good DP to understand how people are able to resolve such issues with the store / manager / CSRs.

Nov 21, 2019, 5:22 pm

#1568

Join Date: Oct 2009

Posts: 19

I'll take the unpopular other side. My recollection is that a negative cash tendered amount means the transaction was reversed and the funds will be returned to the cards - five days only at the earliest.

If a cash refund on the spot was called for the receipt would have CHANGE DUE clearly indicating $1,000, not 0.00.

If a cash refund on the spot was called for the receipt would have CHANGE DUE clearly indicating $1,000, not 0.00.

Nov 21, 2019, 5:54 pm

#1569

Join Date: Mar 2009

Posts: 2,295

I'll take the unpopular other side. My recollection is that a negative cash tendered amount means the transaction was reversed and the funds will be returned to the cards - five days only at the earliest.

If a cash refund on the spot was called for the receipt would have CHANGE DUE clearly indicating $1,000, not 0.00.

If a cash refund on the spot was called for the receipt would have CHANGE DUE clearly indicating $1,000, not 0.00.

Nov 21, 2019, 5:56 pm

#1570

FlyerTalk Evangelist

Join Date: Jul 2003

Location: Florida

Posts: 29,762

In this game, your primary goal is to stay under radar as much as possible, i.e. prevent tripping wire in the system and caused your account being flagged, either automatically by algo or by human.

Nov 21, 2019, 6:01 pm

#1571

FlyerTalk Evangelist

Join Date: Jul 2003

Location: Florida

Posts: 29,762

Yes, this all should be considered. Deposit cash OR deposit MO to liquidate GCs, IF the choice is there. Experienced gamers use multiple banks / CUs to diversify their liquidation methods, and some banks / CUs are easy and convenient to accept cash deposits, and some are better used to accept WM / other supermarket MOs.

The only time you are likely to see a MO deposit "clawback" or deposit reversal by your bank / CU is when:

1. the amount tendered by WM, etc was less than the face value of the MO. I never had that happen, in 5 yrs of MS at WM. I do not think the WM POS/system will allow. BUT some supermarket/convenience stores can have a disconnect between their MO printing machine and the actual amount tendered. ALWAYS ensure the MO seller gets everything you owe him, not just because it is fair, but because you do NOT want a deposit reversal - is it a PAIN to fix. Once, I had supermarket noob employee cut a MO for 499.99, but only debit me 499.00. I gave them $1 cash to balance their till so no hassles later.

2. the bank/CU does not like the way you endorse the MO, when you deposited via mobile deposit / ATM method, and no teller was there to review/edit at the time of deposit. I had this happen once, when the LARGEST CU in the world (lets call this CU #1 ) decided to reverse my MO deposit to an ATM because I did a shared branch deposit (from another CU -CU#2 - not convenient at the time) and the rubber stamp said "mobile deposit only". The receiving CU #1 accepted the MO deposits for 5 days, then reversed them without explanation. By now I had already transferred the money out, that had deposited in CU#2 via CU#1 's ATM. CU#2 reversed the deposit, and demanded me to bring up my now negative balance. AND CU#1 MAILED the rejected MOs back to me, for possible re-deposit at CU#2 since that was the intended destination of the MOs. This whole process took about 2 weeks, and a visit to the local CU#1 and talk with branch manager to get them to reverse the reversal of the MO deposit, when they realized they were overzealous in rejecting MOs that were perfect in every way expect a word "mobile" in the endorsement. Are you confused yet? Bottom line, I got all the money back, but it wasted a few hours.

The only time you are likely to see a MO deposit "clawback" or deposit reversal by your bank / CU is when:

1. the amount tendered by WM, etc was less than the face value of the MO. I never had that happen, in 5 yrs of MS at WM. I do not think the WM POS/system will allow. BUT some supermarket/convenience stores can have a disconnect between their MO printing machine and the actual amount tendered. ALWAYS ensure the MO seller gets everything you owe him, not just because it is fair, but because you do NOT want a deposit reversal - is it a PAIN to fix. Once, I had supermarket noob employee cut a MO for 499.99, but only debit me 499.00. I gave them $1 cash to balance their till so no hassles later.

2. the bank/CU does not like the way you endorse the MO, when you deposited via mobile deposit / ATM method, and no teller was there to review/edit at the time of deposit. I had this happen once, when the LARGEST CU in the world (lets call this CU #1 ) decided to reverse my MO deposit to an ATM because I did a shared branch deposit (from another CU -CU#2 - not convenient at the time) and the rubber stamp said "mobile deposit only". The receiving CU #1 accepted the MO deposits for 5 days, then reversed them without explanation. By now I had already transferred the money out, that had deposited in CU#2 via CU#1 's ATM. CU#2 reversed the deposit, and demanded me to bring up my now negative balance. AND CU#1 MAILED the rejected MOs back to me, for possible re-deposit at CU#2 since that was the intended destination of the MOs. This whole process took about 2 weeks, and a visit to the local CU#1 and talk with branch manager to get them to reverse the reversal of the MO deposit, when they realized they were overzealous in rejecting MOs that were perfect in every way expect a word "mobile" in the endorsement. Are you confused yet? Bottom line, I got all the money back, but it wasted a few hours.

It happened, even though it has not happened to you (or me, or many of us here) in the long history of such activities, much longer than your 5 years I may add. There are still incidents like that happened. That is why cold hard cash is always a welcome refund. Sure everyone here has more than one financial account to handle deposits.

Nov 21, 2019, 6:03 pm

#1572

FlyerTalk Evangelist

Join Date: Jul 2003

Location: Florida

Posts: 29,762

Never tried it before, but I was being serious. Bad news? It's a bank teller essentially applying MO to a cc payment.

From a website:

"You can pay your credit card balance online through the bank's website or app, call the credit card customer service hotline for help, mail in a check or money order or stop by a branch. Choose a method that makes sense for you, taking into account how long it will take to receive the payment and any costs involved, including stamps and online data fees."

From a website:

"You can pay your credit card balance online through the bank's website or app, call the credit card customer service hotline for help, mail in a check or money order or stop by a branch. Choose a method that makes sense for you, taking into account how long it will take to receive the payment and any costs involved, including stamps and online data fees."

In the past when banks start not liking the MO payments one too many, someone from the bank might give you a call. Nowadays it would be a shut down that you only find out when your card stopped working.

Nov 21, 2019, 7:11 pm

#1573

Join Date: Oct 2004

Programs: Amtrak Guest Rewards, Starwood Preferred Guest, Marriott Rewards, Hilton Honors

Posts: 255

You may be OK to do a few times of MO payments to your credit card. But it is a proven method to eventually get your account flagged. You can speculate the consequence.

In this game, your primary goal is to stay under radar as much as possible, i.e. prevent tripping wire in the system and caused your account being flagged, either automatically by algo or by human.

In this game, your primary goal is to stay under radar as much as possible, i.e. prevent tripping wire in the system and caused your account being flagged, either automatically by algo or by human.

Nov 21, 2019, 9:33 pm

#1574

Join Date: Nov 2019

Location: RDU

Programs: HH Diamond, AA Gold, Marriot Plat

Posts: 209

I found my store of $500 VGC (@Giants) and Waltmart Neighborhood Market for MO. Only doing 1 or 2 MO per wk and avoid any suspicious by depositing between two banks. I also buy stuff with the current CC I am MS.

Nov 22, 2019, 12:39 am

#1575

Suspended

Join Date: Nov 1999

Posts: 24,153

Thanks for the heads up, I appreciate it. But, a follow-up question: I always felt that large amounts of MO deposits into a bank account would get your account flagged pretty quickly. Isn't that true? And yet, it seems that people here are doing big amounts with no problems. I'd think paying a cc directly would draw less suspicion versus directly depositing into an account.

simply do whatever you are comfortable doing, some folks may have very high balances and top status with say Bank Two and can get away with most things or will be warned. Others without that clout will be shut down 1-2-3

There are some folks that simply pay off their debt using the cards. its a YMMV issue

And from the way you post and what you ask it seems youd do yourself a favor reading or rereading in the Sticky Welcome to MSing