DCC: Dynamic Currency Conversion (2017-2025)

Jan 9, 2023 | 4:05 am

Jan 9, 2023 | 4:05 am

#976

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

Another interesting difference is that the receipt showed (T) instead of (W) next to the card number.

Jan 13, 2023 | 10:53 am

Jan 13, 2023 | 10:53 am

#977

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

Outside of the UOB ATM, I haven't seen any DCC prompts in Singapore, including the preauth on my World of Hyatt Visa at the Andaz.  Most of my credit card transactions have been contactless, which may be bypassing DCC still.

Most of my credit card transactions have been contactless, which may be bypassing DCC still.

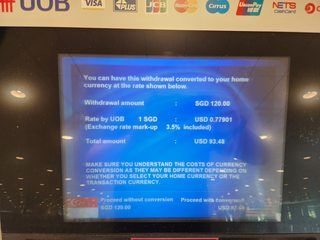

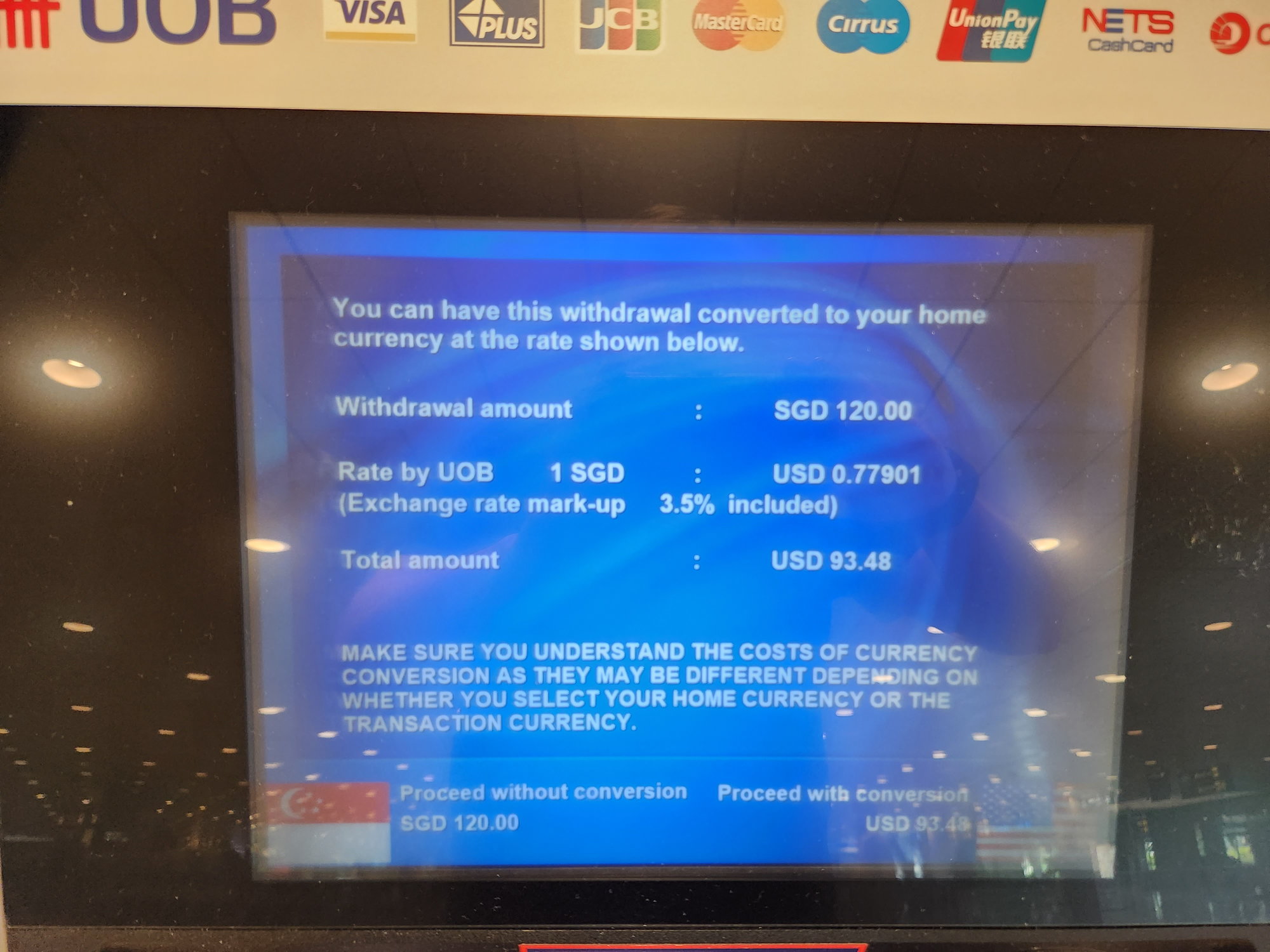

The UOB ATM quoted 93.48 USD for 120 SGD. The Visa rate was 90.32 USD, so this was the 3.5% that the ATM quoted. Usually the quoted % does not match the Visa or MC rate. The screen even had language about understanding the costs of currency conversion. I would say this is probably the most compliant implementation of DCC that I've ever seen. (I'm still not a fan of course.)

Most of my credit card transactions have been contactless, which may be bypassing DCC still.The UOB ATM quoted 93.48 USD for 120 SGD. The Visa rate was 90.32 USD, so this was the 3.5% that the ATM quoted. Usually the quoted % does not match the Visa or MC rate. The screen even had language about understanding the costs of currency conversion. I would say this is probably the most compliant implementation of DCC that I've ever seen. (I'm still not a fan of course.)

Jan 16, 2023 | 9:28 am

Jan 16, 2023 | 9:28 am

#978

Join Date: Jun 2011

Location: NYC

Programs: Just a peon

Posts: 4,569

Last month I went back to Canada for the first time in 3 years. Stopped in a Canadian TD bank near the US border and was surprised the ATM offered DCC. Very easy to decline of course. Didn't encounter DCC anywhere else on the trip , but there were plenty of signs in Niagara Falls ON stating that US$ was accepted (at a worse rate of course)

Sadly, Desjardins didn't even give me the option of conducting the transaction in French (

), but Dynamic Language Conversion is another topic entirely.

Feb 22, 2023 | 7:23 am

), but Dynamic Language Conversion is another topic entirely.

Feb 22, 2023 | 7:23 am

#979

Join Date: Feb 2001

Programs: IHG Diamond, HH Gold, Marriott Silver

Posts: 4,346

The only examples I've encountered of DCC in the Philippines have been at SM Supermarkets. The cashiers tend to hold the device away from you and ask if you want to pay in pesos or USD, so it's very hard to see how bad the rate is. I don't know if they are deliberately being sneaky or are just clueless. From a distance, at an angle, I think it said 5% mark-up, but I can't be sure. (Metro Supermarkets don't do DCC, but they make you sign two receipts as part of some crazy, slow bureaucracy they have going.)

Feb 22, 2023 | 4:09 pm

#980

Original Member

Join Date: May 1998

Location: NYC

Programs: AA 2MM, Bonvoy LTT, Hilton Gold

Posts: 15,011

As another Canadian data point, I'm in Quebec this week, used my US debit card to get cash from both a Scotia and Desjardins ATM, and no DCC at all.

Sadly, Desjardins didn't even give me the option of conducting the transaction in French (), but Dynamic Language Conversion is another topic entirely.

Sadly, Desjardins didn't even give me the option of conducting the transaction in French (

), but Dynamic Language Conversion is another topic entirely.

Feb 22, 2023 | 8:57 pm

#981

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

Feb 22, 2023 | 9:32 pm

#982

FlyerTalk Evangelist

Join Date: Mar 2010

Programs: DL, OZ, AC, AS, AA, BA, Hilton, Hyatt, Marriott, IHG

Posts: 21,005

The only examples I've encountered of DCC in the Philippines have been at SM Supermarkets. The cashiers tend to hold the device away from you and ask if you want to pay in pesos or USD, so it's very hard to see how bad the rate is. I don't know if they are deliberately being sneaky or are just clueless. From a distance, at an angle, I think it said 5% mark-up, but I can't be sure. (Metro Supermarkets don't do DCC, but they make you sign two receipts as part of some crazy, slow bureaucracy they have going.)

Can't you ask for the terminal?

Feb 23, 2023 | 1:57 pm

#983

Flyertalk Posting Legend Moderator: Credit Card Programs, American Express, Capital One, Chase, Citi, Diners Club, Eco Travel, Signatures

Join Date: Jun 2003

Location: Miami, Mpls & London

Programs: AA, IHG & Marriott Platinum; DL & HH Gold

Posts: 51,905

Mar 31, 2023 | 6:15 pm

#984

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

I've been in Ireland this week, which is the origin of this whole mess of DCC. I hadn't seen it on payments until having dinner tonight at Madigan's. I actually noticed it since a customer was paying at the bar with a GBP denominated card. He tapped the payment, and I saw the EU and UK flag appear on the handheld terminal's touchscreen. The customer quickly walked away without selecting, but the bartender selected EUR proactively.

When it came time to pay, the bartender maintained control of the terminal when I tapped the card and pressed the softkey which I knew was the DCC opt out selection. I verified by asking for a copy of the receipt that it was in EUR.

Thanks to the bartender for helping customers opt out of DCC!

When it came time to pay, the bartender maintained control of the terminal when I tapped the card and pressed the softkey which I knew was the DCC opt out selection. I verified by asking for a copy of the receipt that it was in EUR.

Thanks to the bartender for helping customers opt out of DCC!

Last edited by Majuki; Apr 1, 2023 at 11:11 am

Apr 30, 2023 | 8:11 am

#985

Join Date: Jan 2013

Location: Hawai'i Nei

Programs: Au: HA, UA, Marriott, Hilton; GE

Posts: 7,820

Is this a DCC Situation?

I�m currently on a cruise ship, and received notice that onboard charges would be processed through a UK bank, but would be charged in dollars. The ship said that if we wanted to change the card on file to let them know.

Initially, I ignored the message, but started wondering whether this would somehow be a DCC situation, and whether I should change my card on file from JP Morgan to Amex.

Sound like a disguised DCC to the experts here? Suggestions?

Many thanks.

Initially, I ignored the message, but started wondering whether this would somehow be a DCC situation, and whether I should change my card on file from JP Morgan to Amex.

Sound like a disguised DCC to the experts here? Suggestions?

Many thanks.

Apr 30, 2023 | 10:49 am

#986

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

BA processes (or at least did in the past) their US website transactions in the UK even though the transactions are in USD. This used to be frustrating before the days of 0% FTFs since you'd get hit with a FTF on a USD transaction.

Apr 30, 2023 | 12:21 pm

#987

Join Date: Jan 2013

Location: Hawai'i Nei

Programs: Au: HA, UA, Marriott, Hilton; GE

Posts: 7,820

Are prices on board denominated in USD? If so, I imagine this is like what BA does with their ticketing. It's fine to keep the current card on file in that case as long as it doesn't have a FTF.

BA processes (or at least did in the past) their US website transactions in the UK even though the transactions are in USD. This used to be frustrating before the days of 0% FTFs since you'd get hit with a FTF on a USD transaction.

BA processes (or at least did in the past) their US website transactions in the UK even though the transactions are in USD. This used to be frustrating before the days of 0% FTFs since you'd get hit with a FTF on a USD transaction.

May 1, 2023 | 12:41 pm

#988

Join Date: Apr 2014

Location: San Jose, CA

Posts: 111

I'll just add my $.02 (or �.02 if it goes through UK  ). Generally speaking, if you have a 0%FTF card, the only situation where you have to worry is when you're presented with a price in one currency, but the transaction runs in another. If you see a price that's posted in the card's currency, it's not DCC. In certain cases you may see prices posted in multiple currencies — then you can do your math and choose the one that's more beneficial. That was my situation when I was in Jordan — there were places that had prices in both US dollars and Jordanian dinars and in some cases they ended up being slightly better (a few cents) in $$. So if you chose the $$ price and paid in $$, you knew the exact amount and you could see what the dinars would convert to, so that wasn't a DCC situation either. Now if you chose to pay in dinars and THEN they would charge you in $$, that would have been DCC, but they never tried that.

). Generally speaking, if you have a 0%FTF card, the only situation where you have to worry is when you're presented with a price in one currency, but the transaction runs in another. If you see a price that's posted in the card's currency, it's not DCC. In certain cases you may see prices posted in multiple currencies — then you can do your math and choose the one that's more beneficial. That was my situation when I was in Jordan — there were places that had prices in both US dollars and Jordanian dinars and in some cases they ended up being slightly better (a few cents) in $$. So if you chose the $$ price and paid in $$, you knew the exact amount and you could see what the dinars would convert to, so that wasn't a DCC situation either. Now if you chose to pay in dinars and THEN they would charge you in $$, that would have been DCC, but they never tried that.

). Generally speaking, if you have a 0%FTF card, the only situation where you have to worry is when you're presented with a price in one currency, but the transaction runs in another. If you see a price that's posted in the card's currency, it's not DCC. In certain cases you may see prices posted in multiple currencies — then you can do your math and choose the one that's more beneficial. That was my situation when I was in Jordan — there were places that had prices in both US dollars and Jordanian dinars and in some cases they ended up being slightly better (a few cents) in $$. So if you chose the $$ price and paid in $$, you knew the exact amount and you could see what the dinars would convert to, so that wasn't a DCC situation either. Now if you chose to pay in dinars and THEN they would charge you in $$, that would have been DCC, but they never tried that.

May 1, 2023 | 1:55 pm

#989

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

There are destinations where there's a local currency but transactions are primarily in another currency. Two such examples are the Cayman Islands and Aruba. Unless you have a local card, payment processors will process credit card transactions in USD, regardless of the currency denomination of the card. Menu prices in the Cayman Islands usually reflect a KYD price with 1 KYD = 1.25 USD even if the official exchange rate is 1 KYD = 1.2 USD. In Aruba, most menu prices where tourists would be are denominated in USD. Some show AWG at the official exchange rate and others show < 3% markup to USD. However, these are all disclosed before you give payment, so, like with your examples in Jordan, you can decide if you want to pay cash or whatever the merchant decides the USD price would be if making a card payment.

May 1, 2023 | 5:51 pm

#990

Join Date: Jun 2011

Location: NYC

Programs: Just a peon

Posts: 4,569

I'll just add my $.02 (or �.02 if it goes through UK ). Generally speaking, if you have a 0%FTF card, the only situation where you have to worry is when you're presented with a price in one currency, but the transaction runs in another. If you see a price that's posted in the card's currency, it's not DCC. In certain cases you may see prices posted in multiple currencies � then you can do your math and choose the one that's more beneficial. That was my situation when I was in Jordan � there were places that had prices in both US dollars and Jordanian dinars and in some cases they ended up being slightly better (a few cents) in $$. So if you chose the $$ price and paid in $$, you knew the exact amount and you could see what the dinars would convert to, so that wasn't a DCC situation either. Now if you chose to pay in dinars and THEN they would charge you in $$, that would have been DCC, but they never tried that.

). Generally speaking, if you have a 0%FTF card, the only situation where you have to worry is when you're presented with a price in one currency, but the transaction runs in another. If you see a price that's posted in the card's currency, it's not DCC. In certain cases you may see prices posted in multiple currencies � then you can do your math and choose the one that's more beneficial. That was my situation when I was in Jordan � there were places that had prices in both US dollars and Jordanian dinars and in some cases they ended up being slightly better (a few cents) in $$. So if you chose the $$ price and paid in $$, you knew the exact amount and you could see what the dinars would convert to, so that wasn't a DCC situation either. Now if you chose to pay in dinars and THEN they would charge you in $$, that would have been DCC, but they never tried that.