DCC: Dynamic Currency Conversion (2017-2025)

Aug 4, 2022 | 7:11 pm

Aug 4, 2022 | 7:11 pm

#916

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

For smaller transaction amounts, it is about the principle, but there has got to be a threshold where most people would complain. For instance, if you had a restaurant bill of $90, paid $100 cash, and only received $5 in change, I'm sure you would speak up.

Aug 5, 2022 | 1:08 am

Aug 5, 2022 | 1:08 am

#919

FlyerTalk Evangelist

Join Date: Mar 2010

Programs: DL, OZ, AC, AS, AA, BA, Hilton, Hyatt, Marriott, IHG

Posts: 21,005

Aug 5, 2022 | 1:20 am

#920

Join Date: Feb 2012

Posts: 4,631

Hell NO! By that logic any banking operation would be shut down, since they're all taking cuts without delivering goods or useful services. DCC must at least disclose the actual charge, which is not the case with bank spreads. CitiGold at one point advertised "No Fee" ForEx with free mail delivery. After some digging I learned that "Free" really meant a 10% Buy/Sell spread. And if "consumer friendly" is now a requirement, how come airport exchange offices are still in business?

Aug 5, 2022 | 9:10 am

#921

Join Date: Aug 2017

Location: LTN

Programs: Aeroflot Bonus, British Airways Executive Club

Posts: 524

Aug 5, 2022 | 11:30 am

#922

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

Aug 5, 2022 | 11:34 am

#923

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,749

Banks provide a safe place to store your money and also help provide a safe way to transact with it (e.g. by providing credit and debit cards). DCC, on the other hand, is only good for shoveling money into the pockets of merchants and the processors that support it.

Aug 5, 2022 | 2:48 pm

#924

Join Date: Feb 2012

Posts: 4,631

I find this thread useful in helping fellow travelers to avoid the pitfalls of DCC or deceptive practices (if they still occur). If it loses focus or devolves into grandstanding, it would be a loss for all who reads it. When we travel we should also not lecture the locals how to run their businesses. There's nothing wrong for them to make money, especially when it doesn't affect us or we engage with them voluntarily.

Oct 18, 2022 | 7:42 am

#925

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

I just saw DCC for a transaction in front of me at Harrods at LHR. The rate was �52.95 @ 1.1777 USD/GBP and quoted on the register as $62.37. I couldn't see whether the card was a Visa or Mastercard, so I don't know the exchange rate that would have been used. However, the markup would be close to 4% using the current exchange rate. The cashier didn't mention anything, so my guess is that the prompt appeared on the credit card terminal.

I paid with a Visa and used contactless. This avoided DCC automatically for my �35 purchase.

I paid with a Visa and used contactless. This avoided DCC automatically for my �35 purchase.

Oct 19, 2022 | 6:12 am

#926

FlyerTalk Evangelist

Join Date: Aug 2001

Location: RSW

Programs: HHonors - Diamond; IHG - Diamond; Marriott Bonvoy - Platinum

Posts: 14,293

I had only a couple of transactions (taxi and gift shop) recently in Netherlands and France, with no DCC encountered.

Oct 20, 2022 | 1:38 pm

#927

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,749

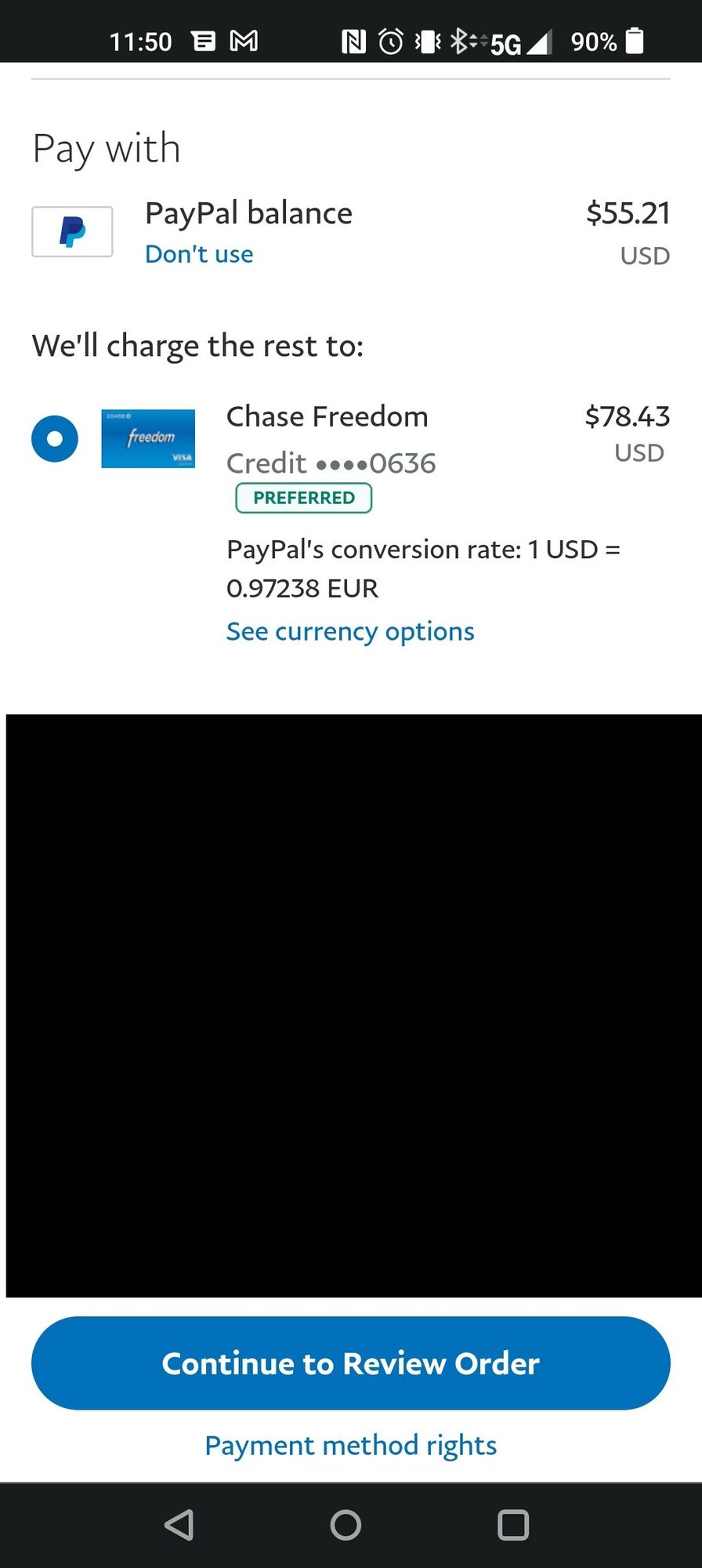

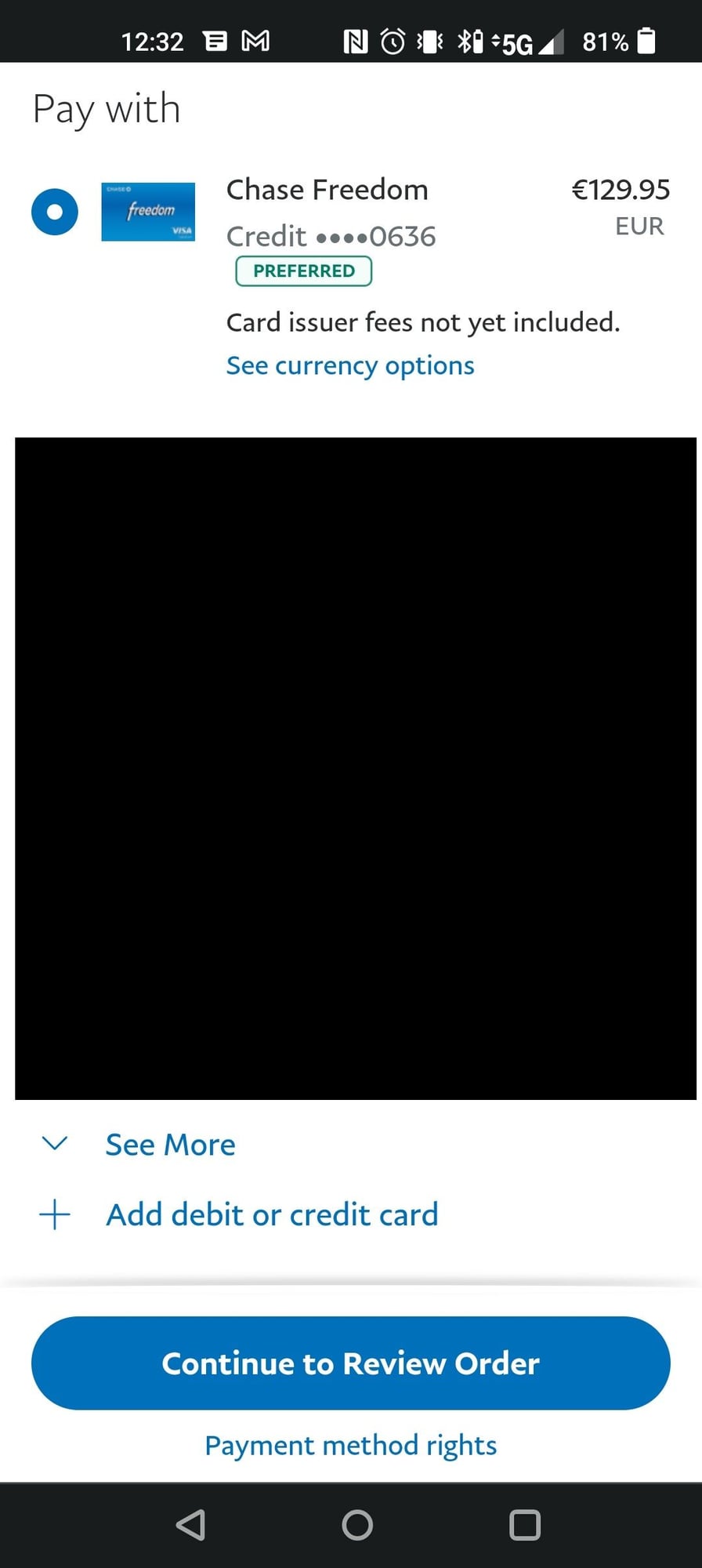

Apparently you have no choice but to opt into DCC if you want to use your PayPal balance. For example, while the option to use your balance does appear if you opt to be charged in USD:

it does not appear if you opt out of DCC:

Probably not a new thing they're doing but figured I'd let people know.

(�129.95 is $127.03 at current exchange rates per Google, so PayPal's conversion would result in paying $133.64 - 127.03 = $6.61 extra, not taking into account the existing PayPal balance.)

it does not appear if you opt out of DCC:

Probably not a new thing they're doing but figured I'd let people know.

(�129.95 is $127.03 at current exchange rates per Google, so PayPal's conversion would result in paying $133.64 - 127.03 = $6.61 extra, not taking into account the existing PayPal balance.)

Oct 20, 2022 | 3:57 pm

#928

Original Poster

Join Date: Jul 2009

Location: SJC

Programs: AA, AS, Marriott

Posts: 6,982

Oct 20, 2022 | 4:24 pm

#929

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,749

Anyway, I don't mind transferring the balance to my bank account first. I'd probably end up with more UR points doing that, too, since the charge would be on the full amount rather than the remaining USD balance.

Nov 25, 2022 | 8:54 am

#930

Moderator: Hyatt, American Express; FlyerTalk Evangelist

Join Date: Jun 2015

Location: WAS

Programs: :rolleyes:, DL DM, AA EXP, UA Silver, Hyatt Glob, Mlife Noir (=> Marriott Amb), invol FT beta tester

Posts: 21,704

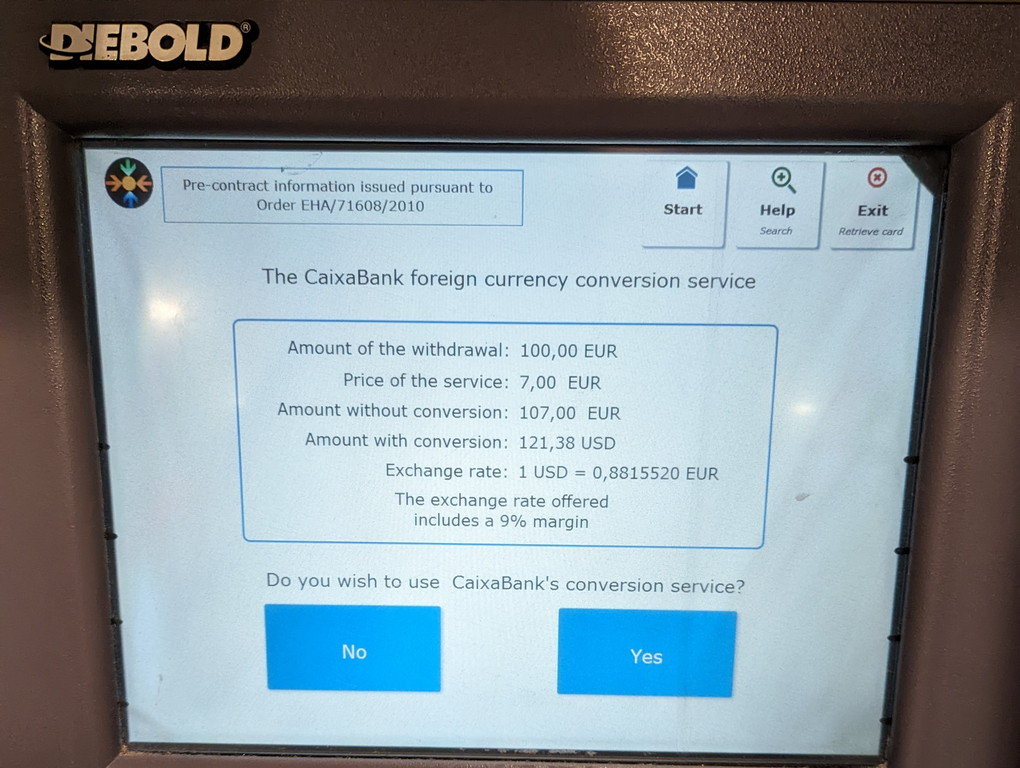

9% at BCN airport ATM