USA Merchants Reach Credit Card Surcharge Rights Agreement [Effective 1.27.2013]

Dec 11, 2019, 2:35 pm

Dec 11, 2019, 2:35 pm

#481

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,508

Not directly related, but we in HK has also noticed a slight reluctance by small merchants to take mobile payments https://www.hongkongcard.com/forum/show/27036?page=1, probably cos acquirers here have to also pay Apple/Google for the use of Apple/Google Pay, and pass it on to merchants.

Additionally, without specific setup, contactless tends to always run over Visa and MC for debit cards in the US. Depending on the store, this can significantly increase processing costs despite Durbin's caps. This may be at least in part why some of the remaining holdouts haven't enabled support.

If a card actually gives elite benefits, I understand the layers. Apple Card is one of the worst not just because it has limited extra rewards options, but they removed almost all of the insurance benefits that the issuer would otherwise need to pay for from the merchant fee. It does appear in the US that the power is with the banks and acquirers - the networks are just signing off on whatever those entities want. I believe it was required at some point for the physical card to indicate the level (which could theoretically be used to discriminate card level acceptance, which is now allowed in the US), but again, Apple Card was able to remove that level print (WE or related) on the physical card. It probably was meaningless anyway because the mobile apps don't show it anyway (going back to the HK hesitancy).

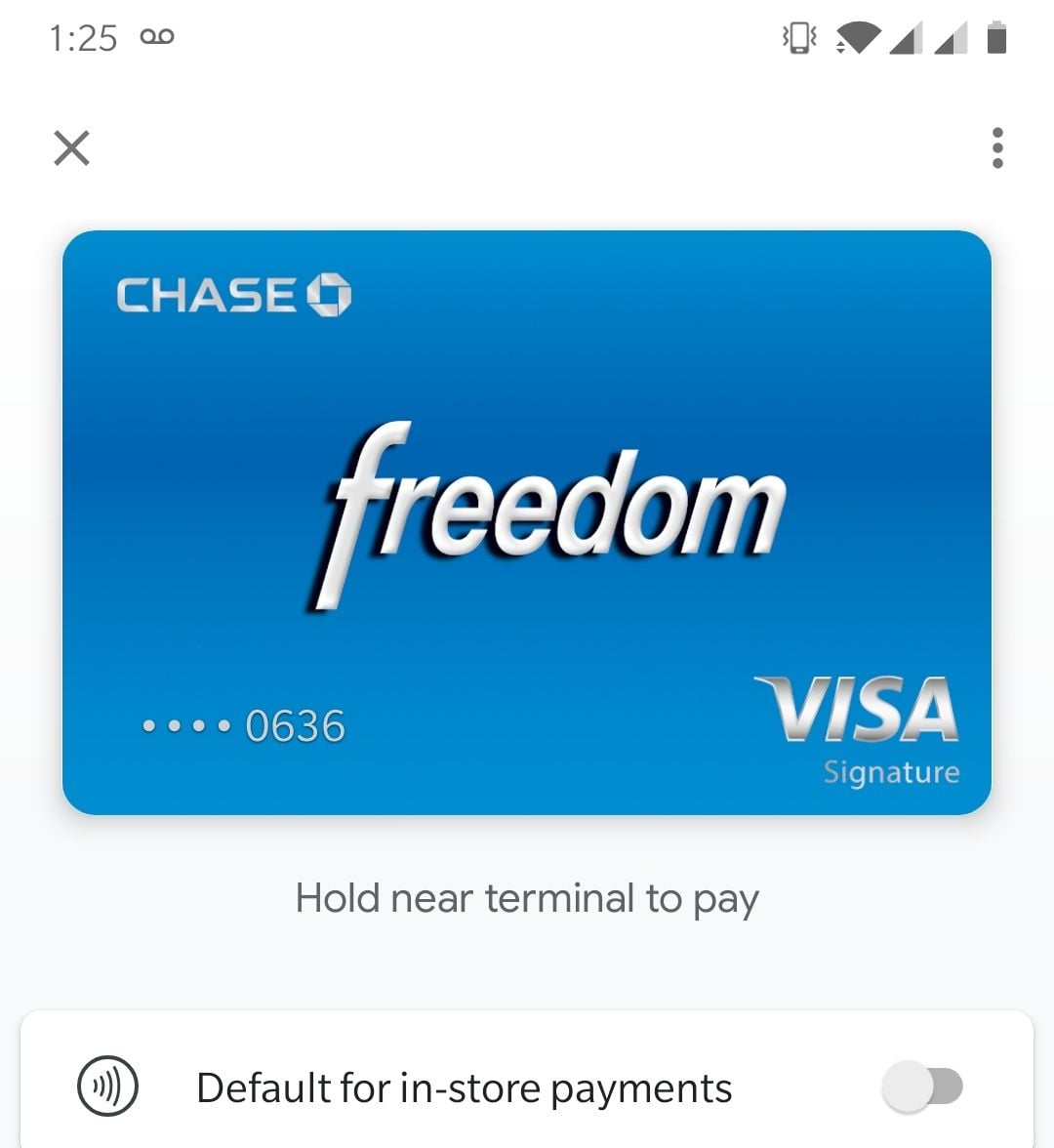

BTW, some cards in mobile wallets do show card type. Here's an example:

That said, making people hand over their phones to verify that they're not using a Visa Signature or whatever would be problematic. I think any sort of effort to restrict card types will probably be done by doing BIN lookups or similar.

I am still looking for some big moves in this space. Apple Card was really in the opposite direction. A so-so product that consumers widely adopted which didn't enhance the merchant or consumer experience. I am sure traditional US issuers are again confused why hype exceeded functionality or benefits.

Dec 16, 2019, 7:34 am

Dec 16, 2019, 7:34 am

#482

Join Date: Sep 2000

Location: OH

Programs: AA Lifetime Plat, Marriot Lifetime Gold

Posts: 9,539

The issuing bank pays Apple (supposedly 0.15% of each transaction for US issuers) to have their cards on Apple Pay. That's why some smaller banks and credit unions still don't support it, never mind issuers in other countries. If it was something networks paid into, I would have expected every card to be able to be added.

AFAIK the "honor all cards" rule is still in effect in the US (minus some possible exceptions such as Costco). Some merchants want to change that, though. I'm not sure how well that'll work out if they manage to succeed. Will it just be one more tool merchants could theoretically use (like surcharging and minimums for the most part have been), or will some actually discriminate based on card type?

AFAIK the "honor all cards" rule is still in effect in the US (minus some possible exceptions such as Costco). Some merchants want to change that, though. I'm not sure how well that'll work out if they manage to succeed. Will it just be one more tool merchants could theoretically use (like surcharging and minimums for the most part have been), or will some actually discriminate based on card type?

2. Honor all cards is still in effect in the US.

Dec 16, 2019, 8:08 am

#483

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,508

Some of the smaller banks and CUs don't have the mobile wallets mostly because of the implementation costs, not so much the fees. But it is short-sighted since cards that are enabled on the mobile wallets are more active and stickier (less likely to attrite) and thus more profitable over the long run

Dec 16, 2019, 11:31 am

#484

Join Date: Sep 2000

Location: OH

Programs: AA Lifetime Plat, Marriot Lifetime Gold

Posts: 9,539

Speaking as someone in the industry, I doubt those institutions have the analytics to know if it makes a difference

Dec 16, 2019, 2:11 pm

#485

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,508

Dec 17, 2019, 4:01 pm

#486

Join Date: Oct 2007

Programs: AA, WN, UA, Bonvoy, Hertz

Posts: 2,491

Sorry, this is not true in states where surcharges are allowed. It appears one of the options for merchants is that they can prohibit one or more tiers of cards that map to the different interchange fees in their agreement.

That would be like a merchant saying they don't accept Visa Signature or Infinite. Or Mastercard World or World Elite. They could have the terminal programmed to look up the BIN (the term qualified is sometimes used for the lower tiers) and then decline the card before auth when used for the transaction.

I have not yet seen this put into action anywhere yet in the US, but honor all cards is no longer accurate. I have the links in my surcharge thread to some of the language from both the acquirer and network perspectives.

The thinking is surcharges which may unfairly target lower tier / interchange fee credit cards equally as well as the reward ones will likely be more prevalent than blocking cards.

That would be like a merchant saying they don't accept Visa Signature or Infinite. Or Mastercard World or World Elite. They could have the terminal programmed to look up the BIN (the term qualified is sometimes used for the lower tiers) and then decline the card before auth when used for the transaction.

I have not yet seen this put into action anywhere yet in the US, but honor all cards is no longer accurate. I have the links in my surcharge thread to some of the language from both the acquirer and network perspectives.

The thinking is surcharges which may unfairly target lower tier / interchange fee credit cards equally as well as the reward ones will likely be more prevalent than blocking cards.

Dec 17, 2019, 6:00 pm

#487

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,508

BTW, surcharges are going to be in effect allowed nationwide soon (if not already) thanks to various states deciding to no longer enforce their existing laws around those (probably thanks to recent SCOTUS decisions).

Dec 18, 2019, 11:20 am

#488

Join Date: Oct 2007

Programs: AA, WN, UA, Bonvoy, Hertz

Posts: 2,491

Source? AFAIK merchants can't outright reject certain cards (the definition of "honor all cards") but can surcharge different tiers at different rates.

BTW, surcharges are going to be in effect allowed nationwide soon (if not already) thanks to various states deciding to no longer enforce their existing laws around those (probably thanks to recent SCOTUS decisions).

BTW, surcharges are going to be in effect allowed nationwide soon (if not already) thanks to various states deciding to no longer enforce their existing laws around those (probably thanks to recent SCOTUS decisions).

So, the concept that is the exception of Honor All Cards is called Limited Acceptance which also came as a result of the various legal settlements. Basically, a merchant in the US can take only Visa and MC debit (as an example) and still run them on the Visa/MC networks, but can reject all of the Visa/MC credit cards. There is a lot of loopholes (such as a US merchant still has to accept all types of non-US issuer Visa/MC cards in that circumstance).

Further, I saw something interesting that even if the customer thought they were using their card over say the Visa network, the merchant could route it via a non-Visa option without having to tell the customer upfront (this must be related to the routing rule changes).

Costco is likely the closest to a Limited Acceptance merchant for things like MC debit (can you use Discover debit at Costco?). This is specifically under the concept that there is no alternative listed debit network on the card (even if still owned by Visa/MC). This is almost never the case in the US, but the rules seem to address it. Such Limited Acceptance rules are also found in other parts of the world, but they have to take the US credit card even if they prohibit regional variations so those of us using our cards overseas would not see this issue come up. I think some Maestro issues were the closest examples. I think there was some conversation that someone was able to use their Canada MC credit card at a US Costco. I am unsure if that was limited to the Costco Canada cobrand or if that is a loophole at US Costco warehouses that is not widely known (Costco US warehouses accepting non-US issued MC credit cards as an example). Definitely worth a test I think.

Dec 18, 2019, 12:07 pm

#489

A FlyerTalk Posting Legend

Join Date: Jul 2002

Location: MCI

Programs: AA Gold 1MM, AS MVP, UA Silver, WN A-List, Marriott LT Titanium, HH Diamond

Posts: 52,575

In practice, I wonder if merchants will really start charging various tiers of surcharges to different kinds of cards. That seems confusing to many people, impractical at the checkout process, and likely to be wildly unpopular with customers.

As it is, I avoid any place that charges a surcharge whenever it's humanly possible. We have a restaurant near here we had lunch at once a week at least. They implemented a surcharge about six months ago and we haven't been back. It seems like a merchant would either need a very dominant market position or operate within a small local cartel to implement surcharges and have them stick. I could see gas station owners colluding on surcharges but I have a hard time seeing a city's restaurants doing it.

As it is, I avoid any place that charges a surcharge whenever it's humanly possible. We have a restaurant near here we had lunch at once a week at least. They implemented a surcharge about six months ago and we haven't been back. It seems like a merchant would either need a very dominant market position or operate within a small local cartel to implement surcharges and have them stick. I could see gas station owners colluding on surcharges but I have a hard time seeing a city's restaurants doing it.

Dec 18, 2019, 12:30 pm

#490

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,508

On that note, I'm thinking this is why the NRF wants PIN to be mandatory for all transactions--to make it easier to hide routing decisions from customers. Getting rid of "honor all cards" would make CC use a lot more of a pain and likely would push most people (back to?) debit cards or cash, reducing costs further. It was never about improved security.

In practice, I wonder if merchants will really start charging various tiers of surcharges to different kinds of cards. That seems confusing to many people, impractical at the checkout process, and likely to be wildly unpopular with customers.

As it is, I avoid any place that charges a surcharge whenever it's humanly possible. We have a restaurant near here we had lunch at once a week at least. They implemented a surcharge about six months ago and we haven't been back. It seems like a merchant would either need a very dominant market position or operate within a small local cartel to implement surcharges and have them stick. I could see gas station owners colluding on surcharges but I have a hard time seeing a city's restaurants doing it.

As it is, I avoid any place that charges a surcharge whenever it's humanly possible. We have a restaurant near here we had lunch at once a week at least. They implemented a surcharge about six months ago and we haven't been back. It seems like a merchant would either need a very dominant market position or operate within a small local cartel to implement surcharges and have them stick. I could see gas station owners colluding on surcharges but I have a hard time seeing a city's restaurants doing it.

That said, as previously mentioned, the places that currently surcharge are the types of places that would have been cash only 5-10 years ago and wish they could still be such. I doubt they care about tiers all that much, or even whether a credit card's being used at all.

Dec 19, 2019, 11:41 am

#491

Join Date: Sep 2000

Location: OH

Programs: AA Lifetime Plat, Marriot Lifetime Gold

Posts: 9,539

I avoid any place that charges a surcharge. I even rejected a coffee once at a store that told me about the surcharge only after the coffee was made. I will make my reasons for rejecting to purchase known as well

Jun 28, 2020, 6:22 am

#492

Moderator

Original Poster

Join Date: Jun 2003

Location: Miami, Mpls & London

Programs: AA & Marriott Perpetual Platinum; DL & HH Gold

Posts: 48,958

In this thread you can see how a large merchant has implemented a card surcharge. Verizon Wireless offers an auto-pay discount, but only if you pay with debit card or bank account. Credit card payments are explicitly excluded from the discount. Now Verizon has introduced a co-branded VISA and it becomes the "only" credit card eligible for the auto-pay discount. Verizon is effectively penalizing credit card use, and offering a discount for using their preferred card.

Jun 28, 2020, 9:54 am

#493

Join Date: May 2013

Location: New York

Programs: UA Silver, Marriott LTPP, Hertz Five Star

Posts: 1,079

In this thread you can see how a large merchant has implemented a card surcharge. Verizon Wireless offers an auto-pay discount, but only if you pay with debit card or bank account. Credit card payments are explicitly excluded from the discount. Now Verizon has introduced a co-branded VISA and it becomes the "only" credit card eligible for the auto-pay discount. Verizon is effectively penalizing credit card use, and offering a discount for using their preferred card.

Similarly with the autopay, it's a bit of an odd scenario - generally payment networks have rules that if you have discounting/surcharging that all brands should be on equal footing. But the transaction may be processed on a "Verizon VISA", but the actual transaction when processed at the retailer itself is private label - so rather than paying 2-5% so called "swipe fees" (card not present of course), the transaction processing is basically free. Per Synchrony bank's Fact sheet:

Originally Posted by Synchrony Bank

Our patented Dual Cards are credit cards that function as a private label credit card when used to purchase goods and services from our partners, and as a general purpose credit card when used elsewhere.

Jun 28, 2020, 12:48 pm

#494

A FlyerTalk Posting Legend

Join Date: Jul 2002

Location: MCI

Programs: AA Gold 1MM, AS MVP, UA Silver, WN A-List, Marriott LT Titanium, HH Diamond

Posts: 52,575

Even though it may effectively feel the same, cash/check/other payment method discounting has been legal for years. Gas stations in the US Northeast regularly post cash/credit prices (where credit is 5-12 cents higher per gallon) and have done so for 10+ years before the surcharging settlement, because the cash price is a "cash discount".

If there's ever any question about whether it's a "discount" or a surcharge, it becomes obvious when you find a nearby station that has only one price: it's nearly always the lower price. (Admittedly, gas station collusion is often too strong for there to be a nearby station not cramming customers with the bogus charge.)

This is one scam you can't always avoid, so I guess I'm just thankful that I haven't been buying a lot of gasoline in recent years and even less in 2020.

Jun 28, 2020, 2:46 pm

#495

FlyerTalk Evangelist

Join Date: Jan 2014

Location: San Diego, CA

Programs: GE, Marriott Platinum

Posts: 15,508

If there's ever any question about whether it's a "discount" or a surcharge, it becomes obvious when you find a nearby station that has only one price: it's nearly always the lower price. (Admittedly, gas station collusion is often too strong for there to be a nearby station not cramming customers with the bogus charge.)

As for surcharges vs. cash discounts, perhaps the differentiation is how explicit the encouragement is. Back when paying for stuff in cash was way more common, most people probably got the cash discount by default (whereas a surcharge is something more "in your face", especially since people are now more likely than not to use cards). Of course, the result is still the same either way--card users pay more.

Anyway, it seems that the scenario of "every store has a surcharge" (or close to every store) still hasn't come to pass. I'm not sure that'll happen any time soon, either, especially due to the pandemic.