Jan 10, 2015, 9:20 pm

Jan 10, 2015, 9:20 pm

Last edit by: NoonRadar

Nov 24, 2015

Dear XXXXXXXXX,

We want to let you know that we are making a change to your Target Prepaid REDcard� by American Express, and you will no longer be able to add money from your debit card at Target stores. As always, you can continue to add money to your Prepaid REDcard by using:

� Your debit card online through your Account

� Cash at a Target Store

� Direct Deposit (You can automatically add all or part of your paycheck, government benefits and federal tax refunds to your Prepaid REDcard)

DEAD FOR DEBIT CARD LOADS EFFECTIVE 10/12/2015 - MEMO: http://frequentmiler.boardingarea.co...uests-can-use/

DEAD FOR CREDIT CARD LOADS. (Amex GCs Included)

Effective May 6, 2015 registers are hard-coded to not allow credit card reload. PIN-based debit cards are working, however YMMV. PIN-based debit cards may be refused by cashiers.

WHAT IS TARGET PREPAID REDCARD?

Prepaid Redcard is a reloadable American Express card. It is only available to purchase at select Target stores.

WEBSITE:

This site may error when in Firefox, especially with adding payees / bill pay. Customer service says to use Chrome or Internet Explorer.

https://amex.serve.com/prepaidredcard

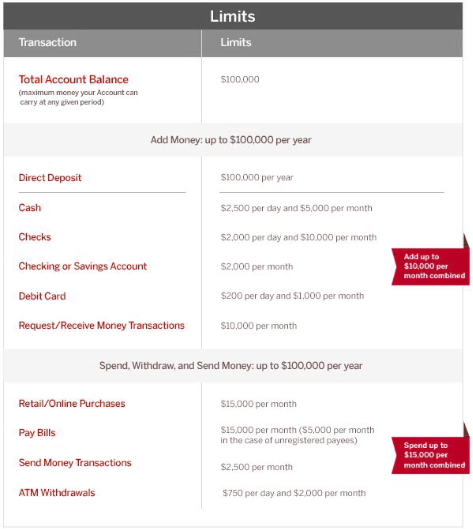

PREPAID REDCARD LOAD LIMITS

Cash (or debit card) loading at Target: ** - $1,000/transaction, $2,500/day and $5,000/month

Online Debit Card Load * - $200/day and $1,000/month

Checking/Savings Account - $2,000/month

Checks - $2,000/day and $10,000/month

ATM Withdrawals - $750/day and $2,000/month

All "Monthly" limits are per calendar month and reset on the 1st of each month.

Daily limits reset at midnight Eastern time, 9 PM Pacific time.

*For online debit load, only use of bank-issued cards is allowed. The use of pre-paid debit cards (Netspend, Paypower, Univision, Paypal, etc.) and VGC/MGC/AGCs is not allowed. Your account will be flagged upon first/second attempt.

ATM Withdrawals:

No-fee ATM usage at US Target stores* and U.S. Allpoint network ATMs. (ATM usage not available at any other ATMs.) Find an Allpoint ATM at: www.allpointnetwork.com Note that some ATMs only allow $400/transaction. There is a $750/day and $2,000/month limit to ATM withdrawals.

RedCard is only available in specific Target stores and is not available in all states. Go to this site to find a list of available locations:https://amex.serve.com/prepaidredcard

FREQUENTLY ASKED QUESTIONS

Q: Can I reload a RB at a Target that doesn't sell RB?

Yes. However, the cashier may not know how to do it. You may be able to coach them through it by saying "It's like reloading a Starbucks (or Gift) card". For step-by-step instructions on one method of 'coaching' new cashiers see Post#1904

Q: Can I buy or reload a RB in North Carolina?

See post here: http://www.flyertalk.com/forum/manuf...a-63.html#2520

There is currently a software issue preventing any reload of any kind in NC. It is a known issue but there is no ETA on a fix.

Q: Can I reload the RB at any register, or just at the Customer Service desk?

It can be done at any register, however some cashiers are not trained on how to do this and you may have to go to Customer Service.

Q: What is the most efficient way to drain a RedCard?

Use BillPay to pay bills. For example, pay the credit card you used to load RedCard with. You can also withdraw money at ATMs.

Q: I cant access the BillPay feature through the RB website!

Verify that your account information correctly reflects a 10-digit phone number (including area code). Numerous people have reported that their account only had a 7-digit phone number (no area code) and that, after updating to a 10-digit phone number, BillPay miraculously started working.

Q: Can we buy a temporary Redbird card while we still have a Bluebird or Serve account?

Yes.

Q: How many Redbird cards can you purchase at once?

You can only purchase one Redbird card a day per SSN. If you plan to purchase more than one, be sure to use a different SSN for each purchase to avoid activation issues.

Q: Can we register our temporary Redbird online while we still have a Bluebird or Serve account?

No. You will have to cancel your Bluebird or Serve account first before registering.

Q: How do I cancel my BlueBird or Serve Account online? Do I need to call them?

Frequent Miler posted a useful trick that will help you cancel online How to cancel Bluebird online This works for both BlueBird and Serve.

Q: Cancelled Bluebird, why does registering Redbird error out saying Bluebird is still active?

If you have open transactions that have not been settled, like BillPay checks that have not yet been cashed, the account cannot settle and will not be truly closed. Thus Target will reject it until it's permanently closed.

Q: Can we get Redbird online?

No. The only way to get Redbird is to find a participating Target store and buy a temporary card there. Some people have purchased RB on Ebay, Amazon, or through private deals. Be aware that doing so may violate the TOS of one or more of these services. Also be aware that buying an un-activated RB, you are potentially buying "stolen" merchandise; the seller *may* have simply taken the un-activated RB cards from a target store without permission. At best they got permission from a low-level employee; they certainly are not getting permission from someone authorized to allow sale of RB outside of the current Target-authorized roll out markets. It is highly recommended to only buy already activated Redbirds because many Targets which do not offer Redbirds also will not be able to activate them and you will spend a month with the Customer Service line trying to get a new one.

Q: Does the initial load you put in when purchasing the Redbird count against the monthly limit?

No. After registering the Redbird online, any loads done will count against your monthly limit, even on your temp card.

Q: Can we load Redbird with Target gift cards at Target?NO.

When loading, the register displays a large message saying that gift cards cannot be used to pay for this transaction.

Q: What are the card�s load limits per transaction at Target?

[B]As of 2/2/2015 there is a maximum $1,000 load per transaction. You can no longer load the same RB multiple times (multiple swipes) in 1 transaction. Likewise, you can no longer load multiple RBs (say your's and your spouse's) in 1 transaction. Maximum of 1 load, for $1,000 per debit card payment. End of story.

Q: What credit cards can I use to reload RedCard in Target stores?

NONE. As of May 6, 2015, credit cards cannot be used to reload.

Q: Can I reload with a debit card?

Yes, but only if the debit card can be authenticated with PIN-number. Signature-based debit that processes on the Visa/MasterCard/AmEx networks will NOT work.

Q: Can I reload with a prepaid debit card or Vanilla Visa?

Yes, but only if you have a PIN for that card.

Q: How can I load 2 debit cards in one transaction? Example 2x$500.

1. Swipe debit card on my terminal after total comes up $1000.

2. PIN pad comes up. Enter 4 digit PIN.

3. Do you want cash back? press NO

4. Do you want full amount on this card? press NO <<<Note: I pressed YES and did not have a step 5. - PHLisa

5. Cashier reads something on register, asks how much on this card. $500. They push something to continue.

6. Swipe card #2. Enter PIN

7. Repeat 3 to 5. Total: 0.00

8. Receipt prints. Thank cashier. The end.

(thanks to Mamibear)

Q: Can someone else buy a Redbird card for you?

Yes. When you buy a temp Redbird card at Target, you have to give them your drivers license info, your SSN (can be any set of numbers, does not need to be real), birthdate, and more. Then, you have to register the card online in order to get a permanent card. In the process of registering online, they ask for the birthday of the original buyer on the first screen, but you can put your own and it will still work. Either way, you can still change the details on the following screens. I did this for my wife. I bought the card at Target and used my own driver�s license, SSN, etc. But, when I got home, I registered the card to my wife. I can�t promise this will work for everyone, but it worked for me.

Q: Can you reload Serve/Bluebird at Target?

No.

Q: How do I contact Target's support team to resolve an issue with my RedCard?

Call Target's Prepaid Resolution Team, their direct telephone number is 800 438 6468 (open from 8AM to 430PM MST).

Q: Can you have both Redbird and AFT cards?

Yes.

You can have both Redbird and AFT since they are independent products.

Q: I got a "Pending" notice that the registration is being reviewed, what now?

Add [email protected] to your address book, and check your spam folder for an email about it. You can also call in. They will need images or faxes of:

� Social Security Documentation (must clearly show full 9 digit Social Security Number). Choose 1 of the following options:

◦ Social Security Card, OR

◦ A Medicare insurance card

Plus...

� Picture ID

◦ A valid driver's license card OR

◦ A valid state issued ID OR

◦ A valid United States Government ID Card (e.g. Green Card) OR

◦ A valid United States Passport (photo page only)

◦ Social Security Card, OR

◦ A Medicare insurance card

Plus...

� Picture ID

◦ A valid driver's license card OR

◦ A valid state issued ID OR

◦ A valid United States Government ID Card (e.g. Green Card) OR

◦ A valid United States Passport (photo page only)

Secure Document Upload

Here's the link to upload secure documents to REDcard: https://secure.prepaidredcard.com/User/SecureFileUpload

Prepaid REDcard (Target) 2015-2016

Feb 8, 2015, 1:07 pm

#1951

Join Date: Jan 2013

Location: NYC

Programs: Delta Plat, SPG Plat, Hyatt Gold, Hertz Presidents

Posts: 20

RedCard Reload Denied at Brooklyn (Atlantic Ave) Location

Yes, this afternoon, I went to the Customer Service department to try a reload and was told by the CSR that there will be no Redcard reloads using credit cards, only debit cards. The CSR also added that this policy went into effect last Sunday. Unsure if this is only for the Atlantic Ave store or all Target stores in the NYC area. I didn't have a chance to go the Flatbush store or the Harlem store since they are both far away. Will attempt to head out to the Harlem store this week.

Feb 8, 2015, 1:41 pm

Feb 8, 2015, 1:41 pm

#1952

Join Date: Feb 2012

Location: The place where it gets so hot in the summer some planes can't take off.

Programs: Marriott LT Titanium, WoH Globalist, National EE, United Platinum

Posts: 1,446

Quote:

Originally Posted by slivrflyr

So hoping that chase isn't as vigilant on multiple near-$1k swipes given that I'm focusing on one card only due to travel plans.

I know Amex tends to be a bit more sensitive to MS

The alternative would be to buy Amex GCs via portal and use those at target. I haven't bought Amex GC Since right before bluebird dropped OV and I narrowly missed being stick w $5k of Amex GCs

This week when I first found I couldn't do $1k + $1K + $500, I did a $1k transaction with an AMEX card, then got turned down for an immediate second $1k transaction with the same card. I didn't call in, I just left it at that. The next day a single $1k transaction with that AMEX card went thru immediately. Since then I've done the same thing with US Bank with no problems.

So unless your Target is a long drive away, you can probably finish your full $5K in 5 days.

Originally Posted by slivrflyr

So hoping that chase isn't as vigilant on multiple near-$1k swipes given that I'm focusing on one card only due to travel plans.

I know Amex tends to be a bit more sensitive to MS

The alternative would be to buy Amex GCs via portal and use those at target. I haven't bought Amex GC Since right before bluebird dropped OV and I narrowly missed being stick w $5k of Amex GCs

This week when I first found I couldn't do $1k + $1K + $500, I did a $1k transaction with an AMEX card, then got turned down for an immediate second $1k transaction with the same card. I didn't call in, I just left it at that. The next day a single $1k transaction with that AMEX card went thru immediately. Since then I've done the same thing with US Bank with no problems.

So unless your Target is a long drive away, you can probably finish your full $5K in 5 days.

Fortunately I spend another few thousand a month on that card so I'm really not that worried about 6 target transactions a month.

Feb 8, 2015, 2:46 pm

#1953

Join Date: Aug 2011

Posts: 118

I dont value points in a concept that is so prevailing among bloggers that it is worth x cent per pt. I count them as the ACTUAL money they can save me.

Case in point, in our recent trips we were able to use HHonors redemption between 10K to 30K a night in various places we needed hotel nights around the world when the paid night would be between $120 to $250 a night.

Upcoming trip has 6 HHonors nights that are 12K + roughly $50 cash or are 30K a night. Retail cost is 120 euro to 250 euro. You can do the math yourself to see whether your 2x cash rebate worth more or the HHonors pts worth more in the way we use them. Hint: they give me the value between $0.005 to $0.017 per HHonors pt depends on which hotel value to use. And one can earn between 5x to 6x on each $1 charge - this gives a return rate between $0.025 to $0.034 - obviously better than earning the 2 pennies from cash rebates to pay for the hotel stays.

We also prefer to rotate the usage of our cards so we would not overburden a limited number of cards as that could cause troubles.

The value of the miles and points are 100% depending on HOW you use them. A good value to one may be a bad value to another person. I would never pay $0.007 per UR pt by MSing thru the Staple.com regardless what the bloggers touted, and also the fact one UR pts actually worth 0.01 so you essentially are still ahead for the $0.003... a 50% gain in theory but in absolute $ term it is hardly much - but that is because we have a lot of Avios and UA miles plus UR pts themselves that we could not possibly use up before the next round of eligibility of sign up bonuses. OTOH, an FTer friend would gladly pay for that $0.007 cost for his URs because he takes many Avios shorthaul flights that tend to be quite expensive - with the Avios the cost to fly PHL-FLL is $115 round trip but the pay ticket would be twice as that. The shorter distance flights in the 4500 and 7500 zones actually yield bigger value as the flights are more expensive than the flight to FLL.

It really is a very simple and basic concept but it seems most everyone else wants to put a "fixed" value on pts and miles - they dont work this way!

How you use each "currency" determines how much the value is to you, not a fixed value like so many are led to believe,

Case in point, in our recent trips we were able to use HHonors redemption between 10K to 30K a night in various places we needed hotel nights around the world when the paid night would be between $120 to $250 a night.

Upcoming trip has 6 HHonors nights that are 12K + roughly $50 cash or are 30K a night. Retail cost is 120 euro to 250 euro. You can do the math yourself to see whether your 2x cash rebate worth more or the HHonors pts worth more in the way we use them. Hint: they give me the value between $0.005 to $0.017 per HHonors pt depends on which hotel value to use. And one can earn between 5x to 6x on each $1 charge - this gives a return rate between $0.025 to $0.034 - obviously better than earning the 2 pennies from cash rebates to pay for the hotel stays.

We also prefer to rotate the usage of our cards so we would not overburden a limited number of cards as that could cause troubles.

The value of the miles and points are 100% depending on HOW you use them. A good value to one may be a bad value to another person. I would never pay $0.007 per UR pt by MSing thru the Staple.com regardless what the bloggers touted, and also the fact one UR pts actually worth 0.01 so you essentially are still ahead for the $0.003... a 50% gain in theory but in absolute $ term it is hardly much - but that is because we have a lot of Avios and UA miles plus UR pts themselves that we could not possibly use up before the next round of eligibility of sign up bonuses. OTOH, an FTer friend would gladly pay for that $0.007 cost for his URs because he takes many Avios shorthaul flights that tend to be quite expensive - with the Avios the cost to fly PHL-FLL is $115 round trip but the pay ticket would be twice as that. The shorter distance flights in the 4500 and 7500 zones actually yield bigger value as the flights are more expensive than the flight to FLL.

It really is a very simple and basic concept but it seems most everyone else wants to put a "fixed" value on pts and miles - they dont work this way!

How you use each "currency" determines how much the value is to you, not a fixed value like so many are led to believe,

No kidding. Thanks for stating the obvious.

Feb 8, 2015, 3:11 pm

#1955

Join Date: Jan 2015

Posts: 38

Alright so I have a little problem, I tried to load my Arrival+ twice today and got fraud alerts on both transactions but upon getting home it seems they actually when through (though declined at the register) but my available credit doesn't reflect the transactions. Do you think these will be removed when the transactions post? Floating the money isn't an issue but I would like to know whats the deal.

Last edited by Nepasser; Feb 8, 2015 at 4:02 pm

Feb 8, 2015, 5:21 pm

#1957

Join Date: Feb 2015

Posts: 1

Read through at least 30 pages and still didn't find the answer I was looking for...

Say I swipe $1k from one credit card onto RC, billpay that $1k to another credit card, then take that $1k, swipe it back onto the RC and billpay back to original credit card?

I am using Chase Southwest CC's

My name is on both but would be using "account numbers" to billpay, not my name

Trying to rack up the points as quick as possible

Say I swipe $1k from one credit card onto RC, billpay that $1k to another credit card, then take that $1k, swipe it back onto the RC and billpay back to original credit card?

I am using Chase Southwest CC's

My name is on both but would be using "account numbers" to billpay, not my name

Trying to rack up the points as quick as possible

Feb 8, 2015, 5:24 pm

#1958

Join Date: Dec 2014

Posts: 34

Alright so I have a little problem, I tried to load my Arrival+ twice today and got fraud alerts on both transactions but upon getting home it seems they actually when through (though declined at the register) but my available credit doesn't reflect the transactions. Do you think these will be removed when the transactions post? Floating the money isn't an issue but I would like to know whats the deal.

Feb 8, 2015, 7:08 pm

#1959

Join Date: Dec 2014

Location: Redbird Wasteland of NC

Posts: 62

Read through at least 30 pages and still didn't find the answer I was looking for...

Say I swipe $1k from one credit card onto RC, billpay that $1k to another credit card, then take that $1k, swipe it back onto the RC and billpay back to original credit card?

I am using Chase Southwest CC's

My name is on both but would be using "account numbers" to billpay, not my name

Trying to rack up the points as quick as possible

Say I swipe $1k from one credit card onto RC, billpay that $1k to another credit card, then take that $1k, swipe it back onto the RC and billpay back to original credit card?

I am using Chase Southwest CC's

My name is on both but would be using "account numbers" to billpay, not my name

Trying to rack up the points as quick as possible

Feb 8, 2015, 7:18 pm

#1960

Join Date: Dec 2014

Location: NY

Posts: 28

Yes, this afternoon, I went to the Customer Service department to try a reload and was told by the CSR that there will be no Redcard reloads using credit cards, only debit cards. The CSR also added that this policy went into effect last Sunday. Unsure if this is only for the Atlantic Ave store or all Target stores in the NYC area.

As I was loading my card, another man tried loading his REDcard at another line. He had a stack of cards with him, all with activation stickers on them, and the only reason I even noticed him was because he was having an argument with the people behind the counter. I wanted to tell the guy to just be cool, but I thought that would be weird.

Anyway, the point is that people should be a lot cooler when loading by CC. Stores can and will implement policies if they think something weird is going on or if they find it difficult to deal with rude/demanding customers.

Feb 8, 2015, 7:21 pm

#1961

Join Date: Feb 2015

Posts: 12

Yes, this afternoon, I went to the Customer Service department to try a reload and was told by the CSR that there will be no Redcard reloads using credit cards, only debit cards. The CSR also added that this policy went into effect last Sunday. Unsure if this is only for the Atlantic Ave store or all Target stores in the NYC area. I didn't have a chance to go the Flatbush store or the Harlem store since they are both far away. Will attempt to head out to the Harlem store this week.

Feb 8, 2015, 7:24 pm

#1962

Join Date: Jan 2014

Location: Chicago

Programs: United MileagePlus, Hyatt Platinum

Posts: 148

As I was loading my card, another man tried loading his REDcard at another line. He had a stack of cards with him, all with activation stickers on them, and the only reason I even noticed him was because he was having an argument with the people behind the counter. I wanted to tell the guy to just be cool, but I thought that would be weird.

Feb 8, 2015, 7:32 pm

#1964

Join Date: Feb 2014

Posts: 215

I went to a local Target store to load my redbird this Friday. The customer rep told me they don't allow to load Redbird & AFT anymore. I went to another Target store 5 miles away and I loaded Redbird without any issue. I am not sure if this issue only apply to that specific target store or will become a new Target policy.

Feb 8, 2015, 7:43 pm

#1965

FlyerTalk Evangelist

Join Date: Jul 2003

Location: Florida

Posts: 29,763

Alright so I have a little problem, I tried to load my Arrival+ twice today and got fraud alerts on both transactions but upon getting home it seems they actually when through (though declined at the register) but my available credit doesn't reflect the transactions. Do you think these will be removed when the transactions post? Floating the money isn't an issue but I would like to know whats the deal.

NO transaction would be posted if the loads are unsuccessful. The pending will fall off in a few days.

Have you called Fraud Alert to clear the block? I am surprised you do not mention seeing a message instruct you to call. If you do not clear the Fraud Alerts, your card will be declined in future transactions.