Investor Day Highlights

Feb 8, 2019, 11:11 am

Feb 8, 2019, 11:11 am

#1

Original Poster

Join Date: Apr 2017

Programs: AS 100k, DL PM, New Sagaya

Posts: 1,292

Investor Day Highlights

Not sure the Investor Day materials were shared. This pre-dates the Q4 Earnings call transcript I shared earlier. Here is a link to the presentation:

http://investor.alaskaair.com/static...a-452723220c5b

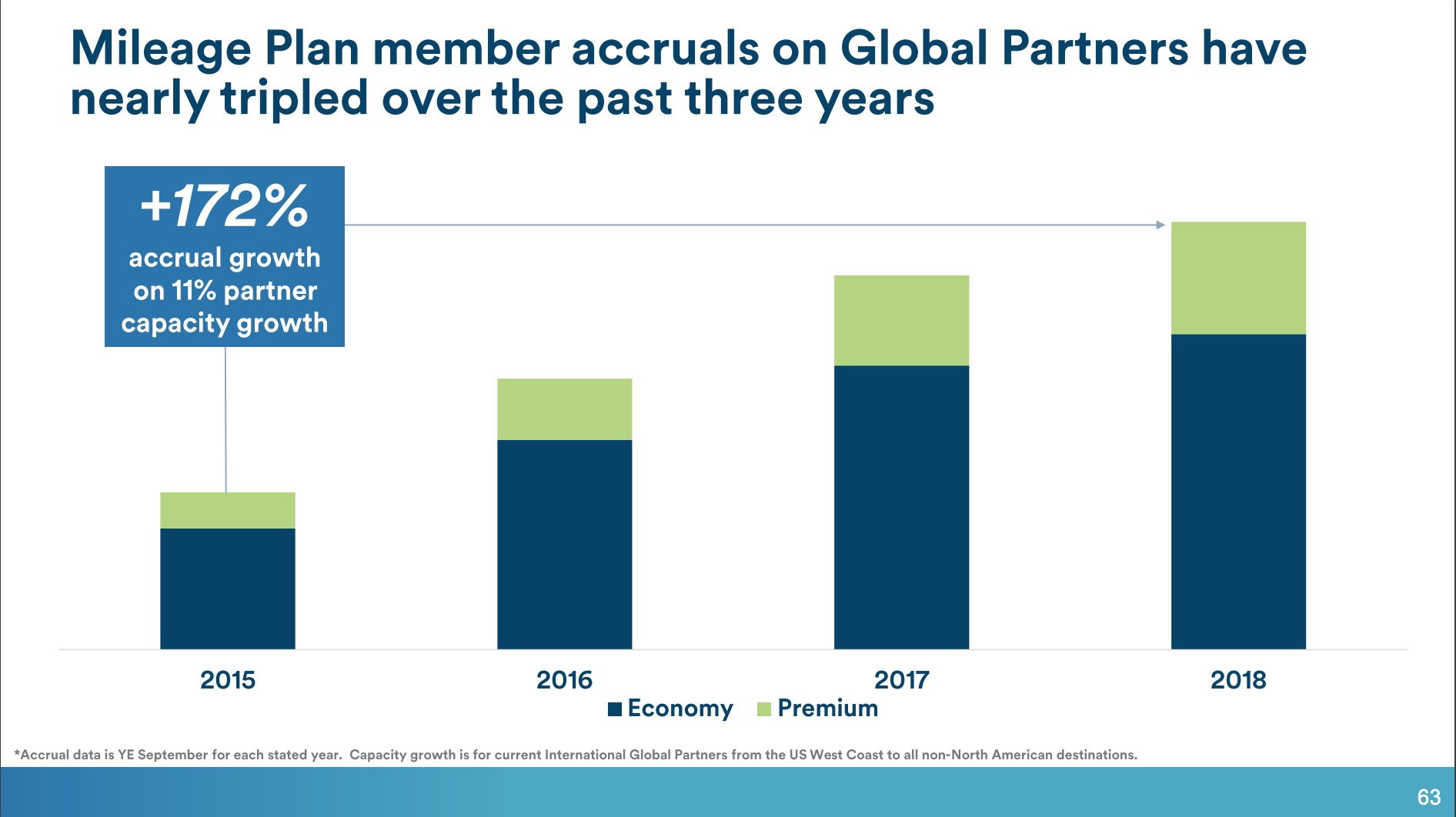

Here are some snapshots from the presentation I think FT'ers would appreciate. Some discussion of the revenue side, staffing, the VISA card, and partner accruals.

http://investor.alaskaair.com/static...a-452723220c5b

Here are some snapshots from the presentation I think FT'ers would appreciate. Some discussion of the revenue side, staffing, the VISA card, and partner accruals.

Feb 8, 2019, 10:10 pm

Feb 8, 2019, 10:10 pm

#5

Join Date: Dec 2007

Location: USA

Programs: AS MVPG75k

Posts: 330

Feb 9, 2019, 8:49 am

#6

Join Date: Oct 2010

Location: SEA/ORD/ADB

Programs: TK ELPL (*G), AS 100K (OWE), BA Gold (OWE), Hyatt Globalist, Hilton Diamond, Marriott Plat, IHG Plat

Posts: 7,764

Indeed. Which is why "average F fare" is a rather meaningless metric - it's a much better indicator of average stage length of revenue F tickets compared to premium cabin yields.

Feb 9, 2019, 10:33 am

#8

Original Poster

Join Date: Apr 2017

Programs: AS 100k, DL PM, New Sagaya

Posts: 1,292

@AndyPatterson: If you want to dive deep, here is the transcript of the presentation and Q&A from the Investor Day:

http://investor.alaskaair.com/static...2-deaac374899a

Re: PRASM - the presentation was a little cagey about this. And it shows in the transcript above where analysts ask about RASM. The presentation suggests RASM for 4Q at 3-5%. But the analysts pushed back a bit suggesting that 2% load capacity growth should show more growth. They definitely do not breakout by segment - its aggregated across all the revenue streams to get to a system level number.

Revenue discussion starts at slide 75 of the presentation: http://investor.alaskaair.com/static...a-452723220c5b

Another element they are clearly still figuring out is the cost side of things, and cross-fleeting is a large part of this. The flight attendants can be cross-fleeted, but not pilots. So they productivity drags from the merger are still there and probably won't get back to pre-merger based on the costs of pilot productivity.

http://investor.alaskaair.com/static...2-deaac374899a

Re: PRASM - the presentation was a little cagey about this. And it shows in the transcript above where analysts ask about RASM. The presentation suggests RASM for 4Q at 3-5%. But the analysts pushed back a bit suggesting that 2% load capacity growth should show more growth. They definitely do not breakout by segment - its aggregated across all the revenue streams to get to a system level number.

Revenue discussion starts at slide 75 of the presentation: http://investor.alaskaair.com/static...a-452723220c5b

Another element they are clearly still figuring out is the cost side of things, and cross-fleeting is a large part of this. The flight attendants can be cross-fleeted, but not pilots. So they productivity drags from the merger are still there and probably won't get back to pre-merger based on the costs of pilot productivity.

Feb 9, 2019, 10:43 am

#9

Join Date: Apr 2003

Programs: B6 Mosaic, Bonvoy LT Titanium (x SPG LT), IHG Spire, UA Silver

Posts: 5,851

It is not even an indicator or average state length as they don't define how they are calculating the average. Is a $50 fee to upgrade at the gate counted in the average? Would the coach portion of the fare be added to the $50 to make it look higher? If 15 people are getting free upgrades and 1 person pays $179 for F, the average is actually only $11.19 in extra revenue per F seat that the F cabin on that flight generated. There are numerous ways to make it look better or worse to get whatever result you like. AS is also not selling $10,000 one way international flights like the legacies do so if AS had the same average as competitors, their stock price would be much higher that it has ever been.

Feb 9, 2019, 10:46 am

#10

Original Poster

Join Date: Apr 2017

Programs: AS 100k, DL PM, New Sagaya

Posts: 1,292

On a product with a pretty big spread in value ($200 F on numerous short runs vs $1600 F on a smaller set of longer runs) a mean is a crummy measure. (Ideally median or some other statistic to represent the distribution...) But it is for comparison purposes here - which could be more meaningful IF we can assume similar routes and price distributions. So, yeah take a block of salt with that number....

Feb 9, 2019, 11:40 am

#11

Join Date: Jan 2008

Location: Seattle, WA

Programs: AS MVPG, 1MM

Posts: 377

@AndyPatterson: If you want to dive deep, here is the transcript of the presentation and Q&A from the Investor Day:

http://investor.alaskaair.com/static...2-deaac374899a

Re: PRASM - the presentation was a little cagey about this. And it shows in the transcript above where analysts ask about RASM. The presentation suggests RASM for 4Q at 3-5%. But the analysts pushed back a bit suggesting that 2% load capacity growth should show more growth. They definitely do not breakout by segment - its aggregated across all the revenue streams to get to a system level number.

Revenue discussion starts at slide 75 of the presentation: http://investor.alaskaair.com/static...a-452723220c5b

Another element they are clearly still figuring out is the cost side of things, and cross-fleeting is a large part of this. The flight attendants can be cross-fleeted, but not pilots. So they productivity drags from the merger are still there and probably won't get back to pre-merger based on the costs of pilot productivity.

http://investor.alaskaair.com/static...2-deaac374899a

Re: PRASM - the presentation was a little cagey about this. And it shows in the transcript above where analysts ask about RASM. The presentation suggests RASM for 4Q at 3-5%. But the analysts pushed back a bit suggesting that 2% load capacity growth should show more growth. They definitely do not breakout by segment - its aggregated across all the revenue streams to get to a system level number.

Revenue discussion starts at slide 75 of the presentation: http://investor.alaskaair.com/static...a-452723220c5b

Another element they are clearly still figuring out is the cost side of things, and cross-fleeting is a large part of this. The flight attendants can be cross-fleeted, but not pilots. So they productivity drags from the merger are still there and probably won't get back to pre-merger based on the costs of pilot productivity.

Feb 9, 2019, 2:39 pm

#12

A FlyerTalk Posting Legend, Moderator, Information Desk, Ambassador, Alaska Airlines

Join Date: Dec 2006

Location: FAI

Programs: AS MVP Gold100K, AS 1MM, Maika`i Card, AGR, HH Gold, Hertz PC, Marriott Titanium LTG, CO, 7H, BA, 8E

Posts: 42,957

Yes I think AS would like to get back to a single fleet type. But this will take time, as additional frames need to be acquired, plus more pilot training. We'll see how the 737-MAX performs for AS once it's on property.

Feb 9, 2019, 5:02 pm

#13

Join Date: May 2003

Location: SFO, mostly

Posts: 2,204

I�d expect they will get rid of A319s and A320s as their leases expire, but that will take some years. The A321NEOs are an attractive plane for transcons, so it wouldn�t surprise me to see those stay in the fleet, unless it doesn�t perform up to expectations.