Loyaltylobby has published the entire powerpoint presentation of the

Finnair Capital Market update on November 13. The full slides can be viewed there.

Some interesting quotes and slides that I think are noteworthy (and in some cases damning!):

“Key assumptions in our strategy2026-2029

- Russian airspace will remain closed for the time being

- Finnair will create value to customers and shareholders as a standalone company”

"Ancillary revenue per passenger ~17€ Q4 2024–Q3 2025"

“Finnair is cost competitive against full-service carriers”

“Finnair has a proven track record for cost discipline

- Continuous dialogue with labour unions

- Reassess non-core activities

for insourcing

- Maintaining good on-time performance and regularity

- Efficiency through Al utilisation and digital development

- Optimised end-to-end processes

- Opportunistic approach on aircraft transactions”

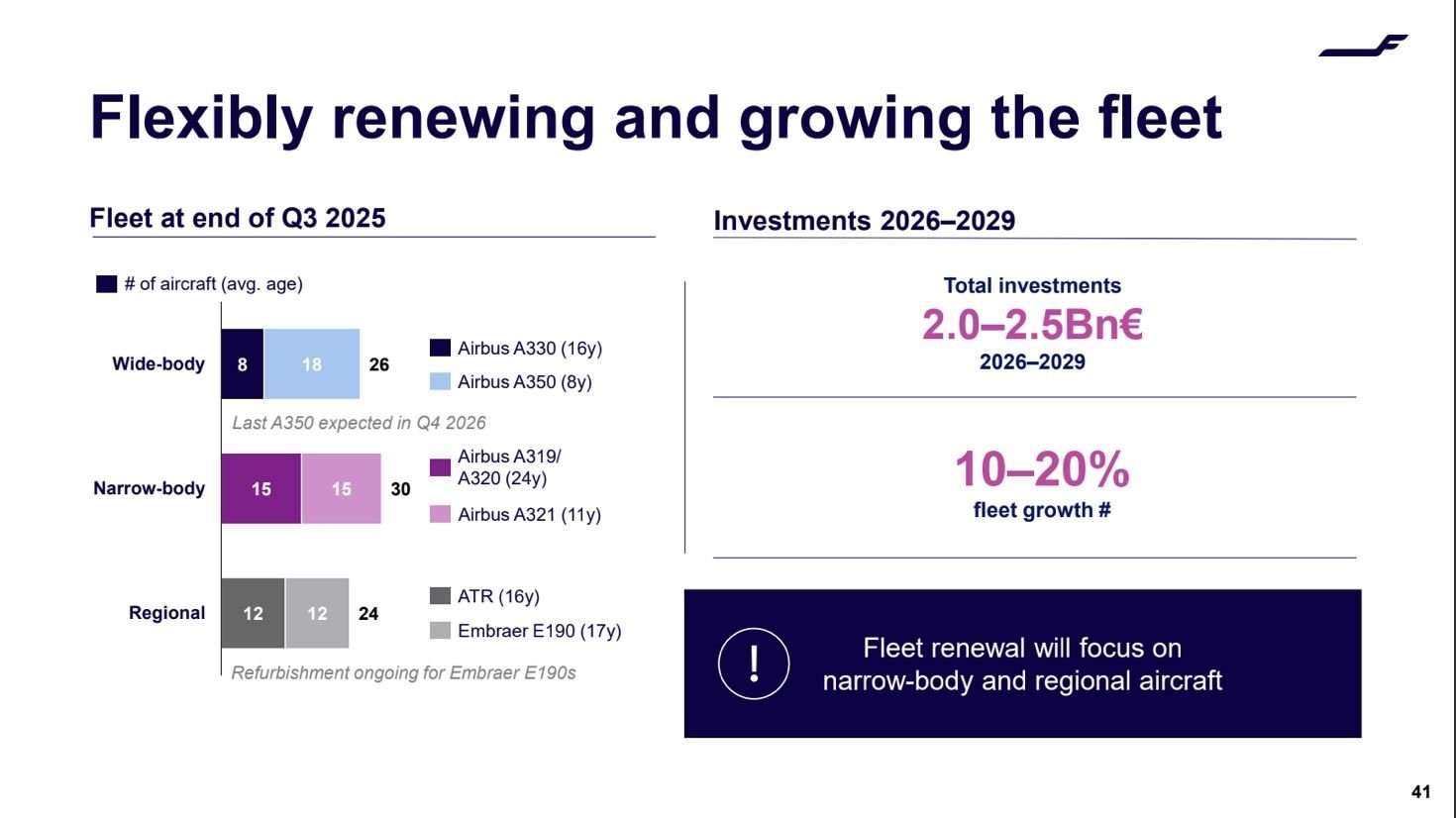

I don't think Finnair has a proven track record for dialogue with unions, as the long strike period proved!"Airbus A330 (16y)

Airbus A350 (8y)

Airbus A319/

A320 (24y)

Airbus A321 (11y)

ATR (16y)

Embraer E190 (17y)"

24 year average age for A319/A320 is a disgrace! And Finnair would have improved profitability with more fuel efficient A320neo family aircraft.

“Fleet renewal will focus on narrow-body and regional aircraft”

“CapEx-light retailing and loyalty” (I suppose our loyalty is worth as little cost to AY as possible!)

“We are the pioneer of product

bundles in the industry

“Combos” introduced on 16 September 2025”

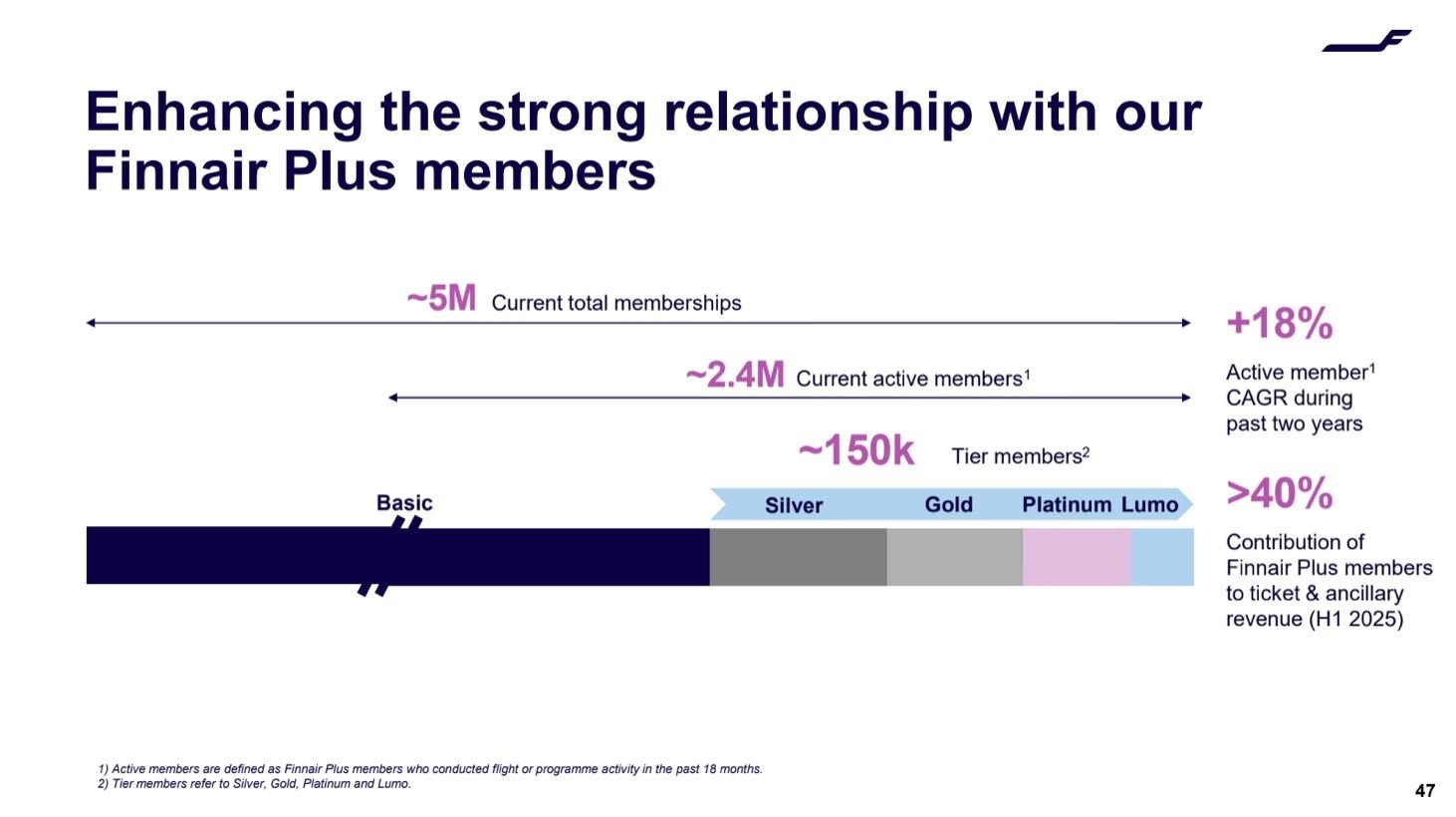

Interesting insight that I think helps see the attitude Finnair management has towards us "active Finnair plus members"