These new additional routes will eat in the profits of each Taiwanese airline.

A glance at China Airlines financial reports.

Financial and Operational Results (YoY)

2019

Passenger 96,176,865K (2.0%)

Cargo 43,406,487K (-12.2%)

Other 6,789,049K (3.0%)

Pax # 15,628,114

Pax Load Factor 80.8%

Pax Yield 2.226

2024

Passenger 107,420,017K (8.4%)

Cargo 60,444,475K (6.3%)

Other 7,317,963K (26.9%)

Pax # 11,464,422

Pax Load Factor 78.7%

Pax Yield 2.88

2025 (until Sep)

Passenger 77,731M (-4.4%)

Cargo 48,518M (13.7%)

Other 6,352M (22.3%)

Pax # 8,646,018

Pax Load Factor 77.9%

Pax Yield 2.80

2024 (until Sep)

Passenger 81,325M

Cargo 42,661M

Other 5,196M

Pax # 8,589,544

Pax Load Factor 79.2%

Pax Yield 2.90

Number of passengers carried in 2025 increased in comparison to 2024. However, passenger revenue dropped (so as load factor and yield).

Since load factor is using RPK as the measurement, it means the empty seats in long haul has eaten into the overall loading.

https://2025itf.china-airlines.com/?...jE3NjAyNzIyMTQ.

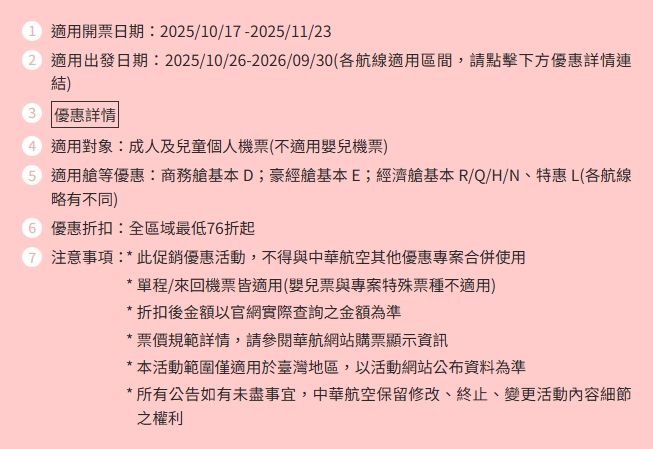

Overall fares have dropped in comparison to 2024. Even though Japan-Taiwan remains strong and carried more passengers than over, the fare is not the same as 2024. ITF promotion was suppose to be over on Monday, but I guess the sales was not great so CI has extended to 11/23. Overall fares have dropped during promotion. Long hauls such as TPE-ONT, LAX, SFO, PHX, SEA all have Business Class D available during off peak periods and the fare is ~120K (about 10-15K drop in comparison to last year). Short hauls in Southeast Asia already had cheap prices last year's ITF promotion, but this year has decreased by 1-1.5K in Economy N (so dropping to 7K ish on non redeye) and by 2K in Business D (so dropping to 24-26K ish). Popular cities in Japan have remained strong, but the price has also dropped to near 10K for Osaka (compare to 15K last year). Places such as Nagoya, Kumamoto, Takamatsu has dropped to as low as 7-8.5K.

https://ci-itf.passion-ad.com/flight-line.html

https://ci-itf.passion-ad.com/flight-line.html