Originally Posted by

moondog

All he was suggesting is that Delta, and especially Delta, doesn't unload business class award seats on the cheap unless it is nearly certain that nobody is going to give them cash for them; i.e. I don't know of a single other tpac in which they sell them for 110k.

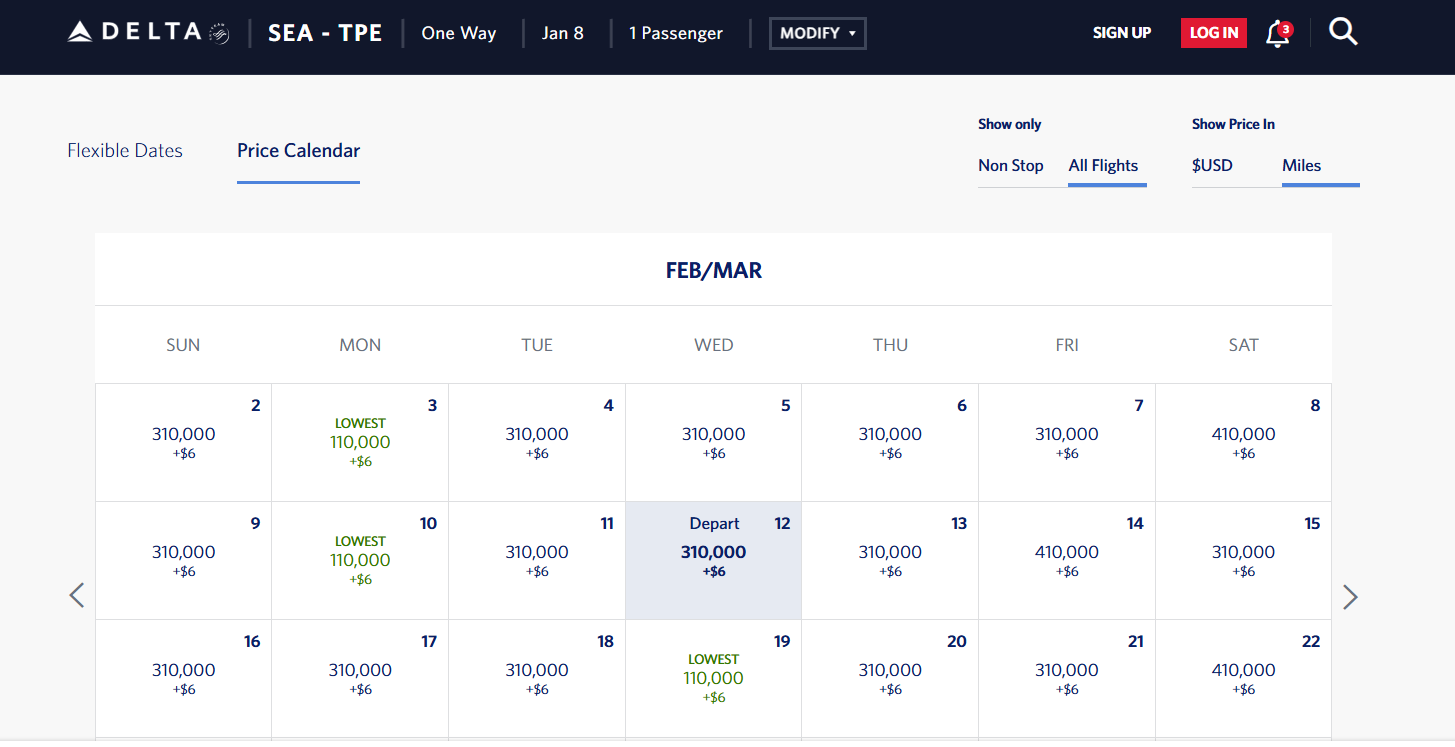

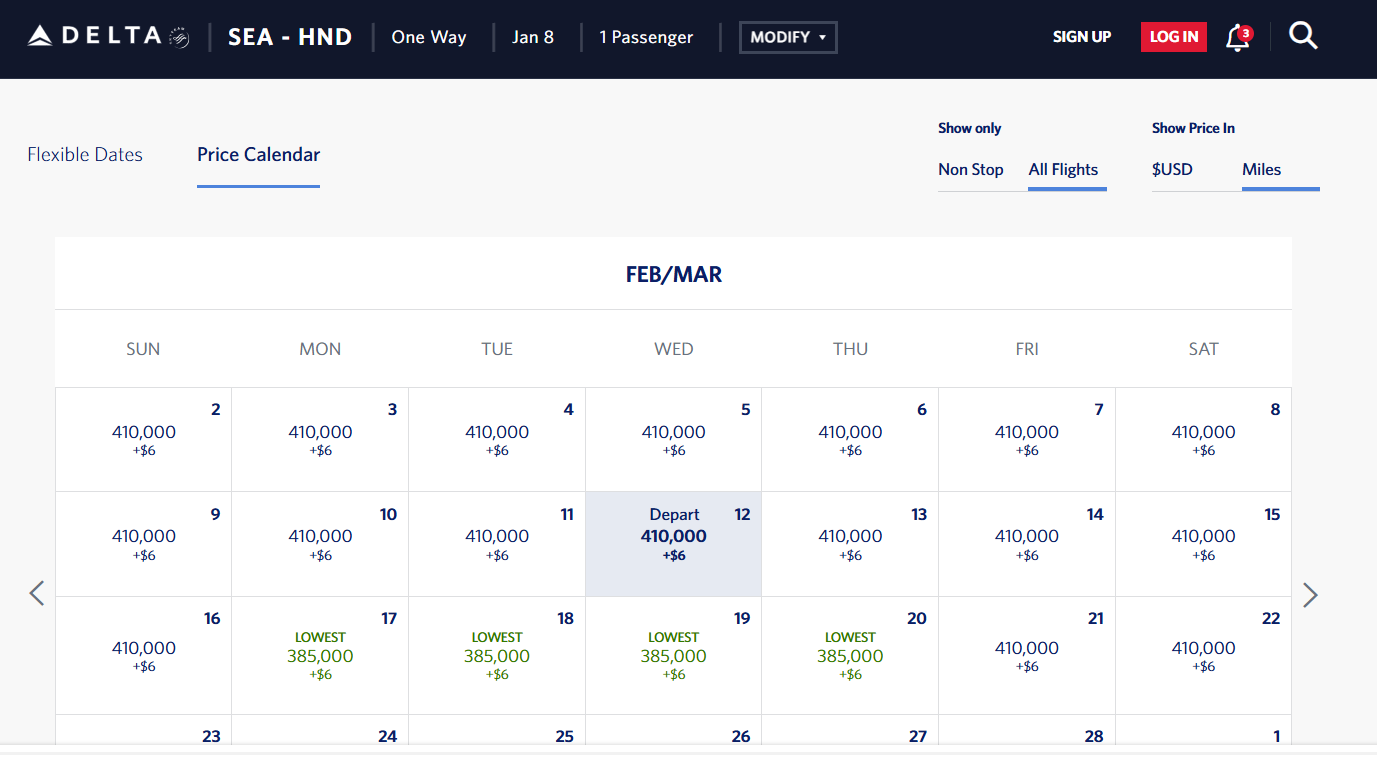

Here's SEA-HND (a route that does sell), for comparison purposes:

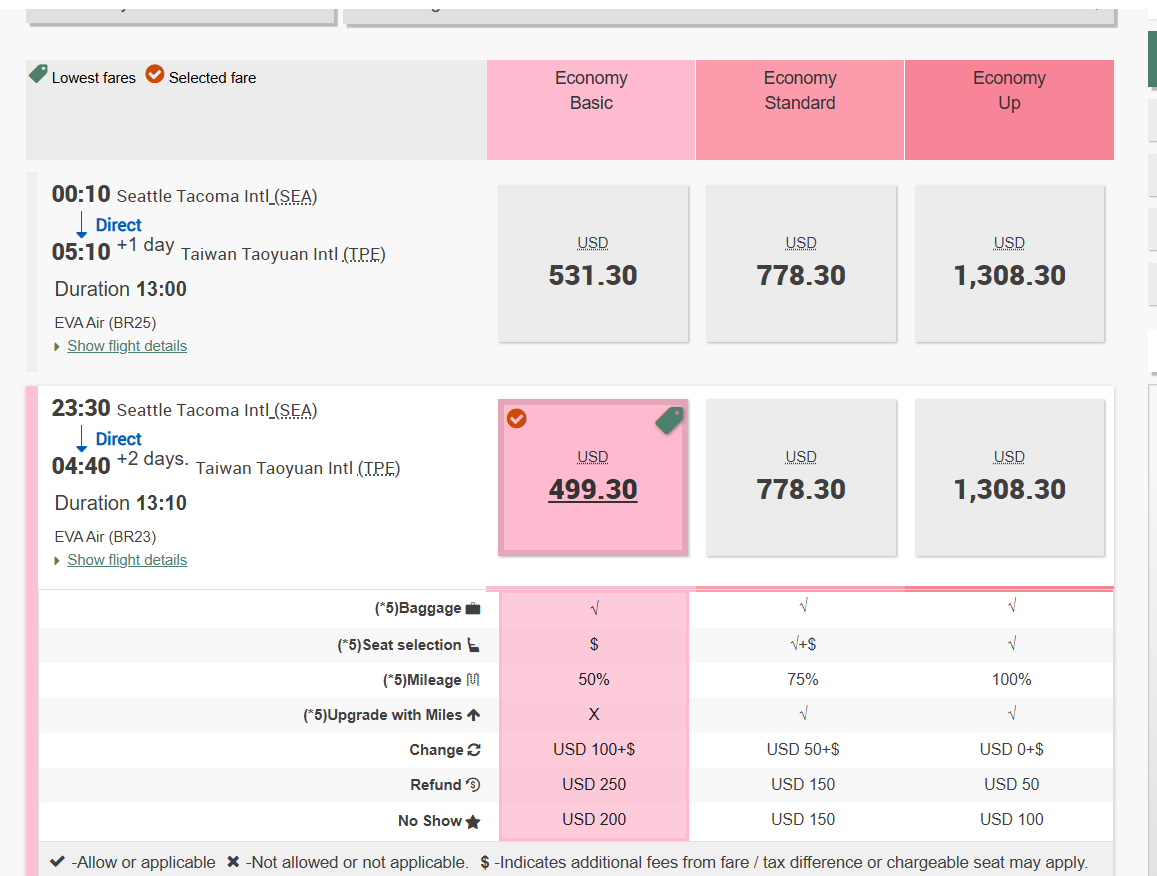

As you can see here, Delta charges less for Main Cabin than EVA does for Basic. Since both of their basic fares include baggage (CI has some fares that don't), I think it makes the most sense to compare those instead of standard (i.e. get your seats at t-24).

The only conclusion I'm able to possibly draw from Delta's ramp-up at SEA is that it reaffirms their desire/commitment to transform it into their SFO.

- O&D passengers simultaneously pay the more and cost the least to service on pretty much every route in existence, and without strong O&D, routes die off.

- There are at least 30 different ways to get from NYC to TPE with a single connection, including DL and DL+KE. Their fares are in line with the competition in that market. So, what?

- Since this thread is specifically about TPE-SEA, it makes sense to focus on that market in isolation (i.e. without all of the white noise).

- Still, it is somewhat useful to sanity check DL v UA in markets like SLC-TPE or the Taiwanese carriers against each other in markets like SEA-BKK. There aren't any real shockers in this regard, btw.

- Some of you guys seem to have problems with one way fares and/or US POS. As I mentioned previously, you're welcome to employ a different baseline approach yourself, but you'll arrive at pretty much the same conclusions. I will note that RTs are a bit of a PITA for comparison purposes, though, because you often run into various restrictions that further muddy the waters.

Flawed methodology leads to flawed conclusions.

- Many people booking international flights are not booking one-ways, they book RTs, so citing one-ways as a way to abstract data is just wrong.

- Of course, O&D matters a lot, but we would all agree the current level of daily capacity far exceeds the Seattle MSA's PDEW for TPE. Yet based on LFs, all of their planes are still majority filled, which means many people are connecting passengers, either connecting from outside of SEA or connecting beyond TPE. If this route's success was purely determined by O&D, your methodology would make sense, but we know that it's very much not the case.

- And this is exactly why I've emphasized many times, airlines have networks not individual routes. In the same way Taiwanese airlines are using this to feed their onward flights, Delta is using their domestic network from their SEA hub to directly feed this TPE flight. They even specifically retimed this flight to make it better suited for domestic connections on both ends. That's why bringing up their connecting fares, which appear to be competitive, is extremely relevant and not "white noise".

At the end of the day, it's very possible, and even probable that Delta's TPE yields are not strong and/or weaker than the competition. The lower load factors do indicate weakness, however, since you do not have direct access to the entirety of the fare data, you cannot accurately assess what the yields are on this route. The overall success of a route is still determined largely by the yields, we've agreed above that even if planes are not massively full, they can still be lucrative like UA operating PEK or KIX.

I'm not claiming to know how well the route is doing, so I'm not sure how anyone else is conclusively saying how successful or not this route is.