Originally Posted by

yoloswag420

1. Unless you have access to the entire schedule's fare data, I don't think you can specifically know if the front of the cabin is consistently filled or not. Browsing a few seat maps anecdotally or using your own flight is not representative at all. In isolation, I could point to the fact that the Delta One cabin is completely sold out for tomorrow's flight, but that doesn't actually mean anything in the broader picture.

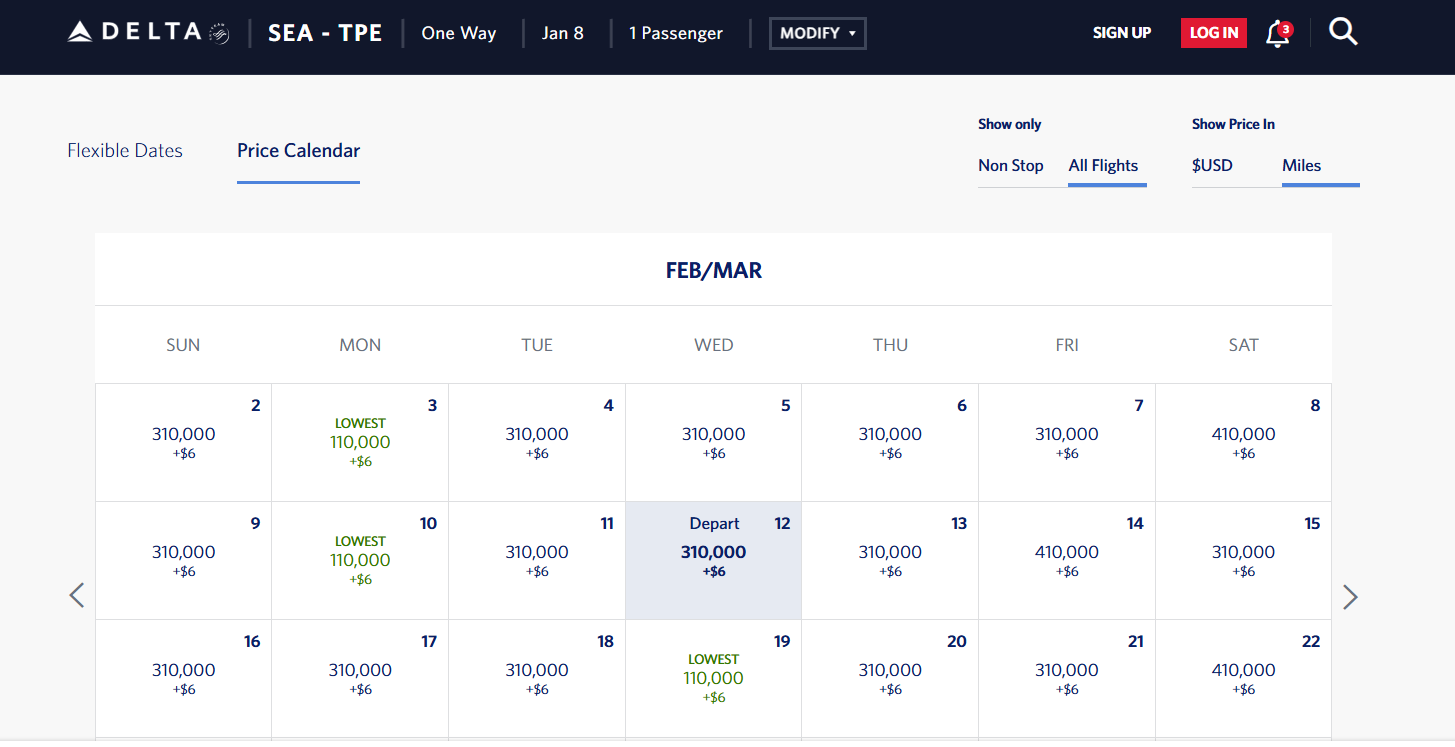

All he was suggesting is that Delta, and especially Delta, doesn't unload business class award seats on the cheap unless it is nearly certain that nobody is going to give them cash for them; i.e. I don't know of a single other tpac in which they sell them for 110k.

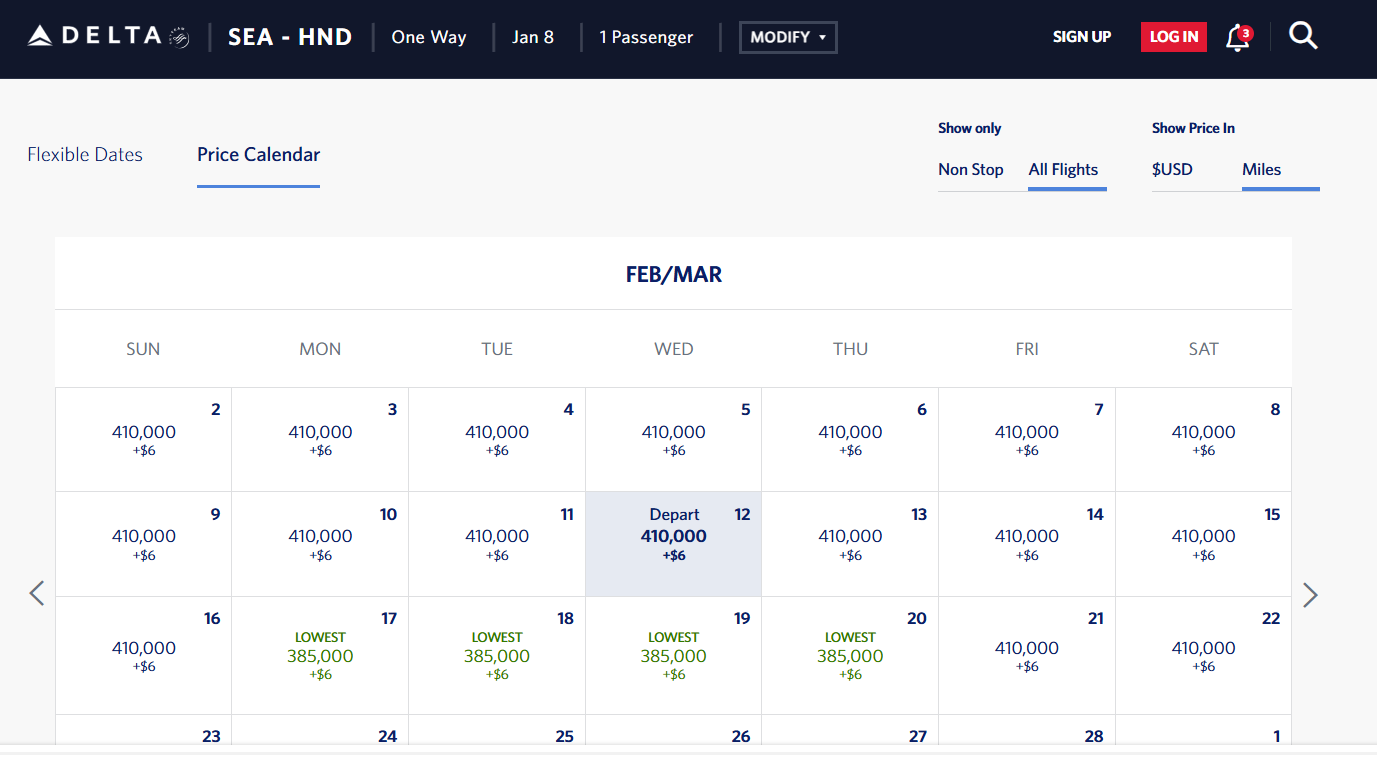

Here's SEA-HND (a route that does sell), for comparison purposes:

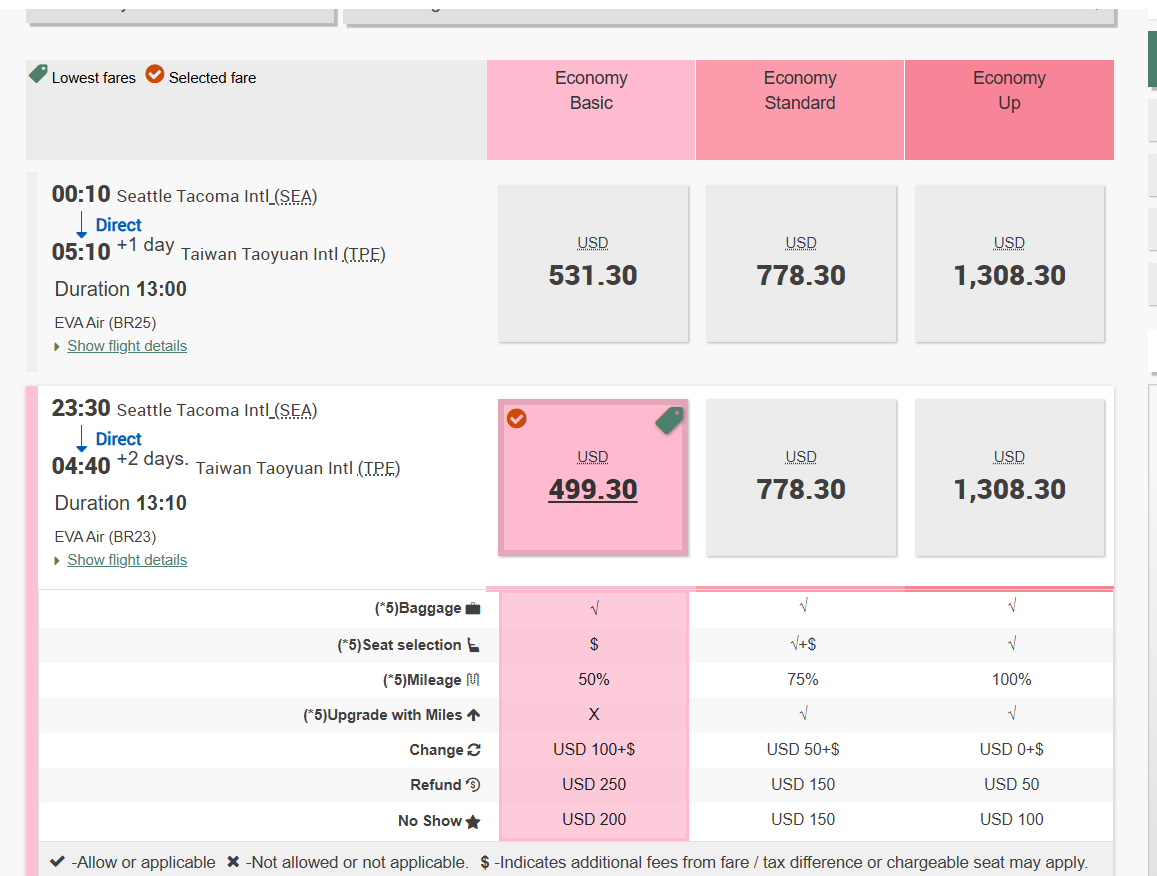

I'd also add you're looking at Basic Economy fares for Delta, their proper Main Cabin pricing is inline with the competition, which doesn't quite have the same concept. US carriers sometimes even earn back the difference or more from ancillary services by upselling addons from Basic Economy, which is a very successful concept.

As you can see here, Delta charges less for Main Cabin than EVA does for Basic. Since both of their basic fares include baggage (CI has some fares that don't), I think it makes the most sense to compare those instead of standard (i.e. get your seats at t-24).

2. Delta is opening up an A350 pilot base out of SEA for their Asia flights. I don't think the inference is citing the addition of premium seats as this route is successful, but rather that's a tool Delta is employing to improve their returns on this route. If they do somehow fill up their premium seats, then they will be able to tradeoff the lower LFs in economy and bring in more revenue.

The only conclusion I'm able to possibly draw from Delta's ramp-up at SEA is that it reaffirms their desire/commitment to transform it into their SFO.

3. Finally, I have to keep emphasizing this, airlines sell networks, not individual routes. If SEA-TPE is boosting the rest of their domestic network, that's a net win, and not something you can easily discern. For example, Delta is selling seats that connect onto this flight from the East Coast for 6k+ RT in business class, which clearly provides a lot of value. Delta's schedule makes it more focused on US domestic connections from both sides vs Taiwanese carriers are focused on serving local population + onwards Asia connections, different markets, so it's hard to point to conclusively say what the results are by cherry-picking one-way marketed fares.

- O&D passengers simultaneously pay the more and cost the least to service on pretty much every route in existence, and without strong O&D, routes die off.

- There are at least 30 different ways to get from NYC to TPE with a single connection, including DL and DL+KE. Their fares are in line with the competition in that market. So, what?

- Since this thread is specifically about TPE-SEA, it makes sense to focus on that market in isolation (i.e. without all of the white noise).

- Still, it is somewhat useful to sanity check DL v UA in markets like SLC-TPE or the Taiwanese carriers against each other in markets like SEA-BKK. There aren't any real shockers in this regard, btw.

- Some of you guys seem to have problems with one way fares and/or US POS. As I mentioned previously, you're welcome to employ a different baseline approach yourself, but you'll arrive at pretty much the same conclusions. I will note that RTs are a bit of a PITA for comparison purposes, though, because you often run into various restrictions that further muddy the waters.