Originally Posted by

kb1992

Back to this thread, OP here with an update.

After Chase reinstated my CSR in Sept. 2020, I have successfully applied for 3 more Chase cards.

Chase Freedom

United Quest

Marriott Boundless

I loved 80000 United miles and 60000 Marriott points!

I am still keeping my CSR, but my wife and son closed their CSR due to lack of travel.

My current balance for 4 Chase cards is over $30,000 with combined credit exceeding $120,000.

However, my credit score is down to 680 from 830. I only have Chase cards. Why?

Originally Posted by

bgriff

Your credit report doesn't actually "know" whether you pay your cards every month or not -- it mainly just gets a report of what the balance is when the statement closes on each card. So if you spend a lot each month, even if you pay it after statement close every month and never accrue any interest, your credit report can still look similar to that of someone who is financing large balances over time. Try paying all or most of your balance on each card a day or two before statement close for the next month and see what it does to your score.

Also, I assume you have already checked your credit report in general to make sure there isn't an error or any fraud going on that could affect your score.

ETA: Chase of course knows better your payment habits on their cards than what shows up in your general credit report, so they are using more data than just your credit score to assess your request for a credit line increase. But, Chase also tends to be aggressive with credit lines up front (lots of people got $30K+ on their CSPs and CSRs) but then have a pretty hard target of how much credit they will extend to any one individual, so if you're at that limit it may not be indicative of any broader issue if they won't increase your credit line. They will reallocate available credit among your existing cards if that helps though.

Originally Posted by

GUWonder

4 hard inquiries drive down a score from 830 to 680? I think that 4 hard inquiries is unlikely to be a significant driver of the credit score dropping that much -- and it probably would not even amount to a third or quarter of that kind of score drop. But then there are reports like kb1992.

Credit utilization skyrocketing and high total balances are where I'd focus to get the score back up. That is after making sure the accounts and payment history on accounts on file are all solid still.

Originally Posted by

pallhedge

That's a 5th credit inquiry, fyi.

What "credit score" are you referring to? Using data from which credit report? A true FICO score is not likely to swing that wildly without a delinquency on your credit report. Have you looked over any of your current credit reports? Check your FICO 8 credit score for free using Experian or Discover Scorecard.

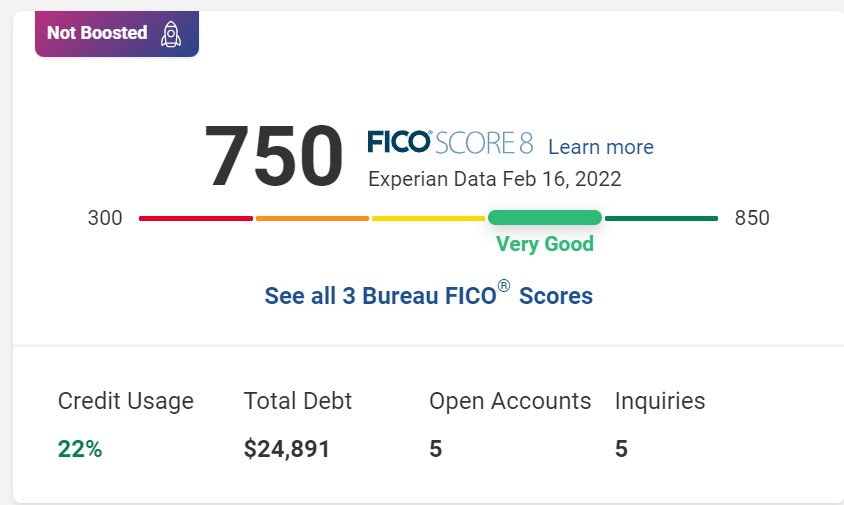

I checked my FICO 8 score which is 750. This is significantly better than Chase Credit journey score 694.

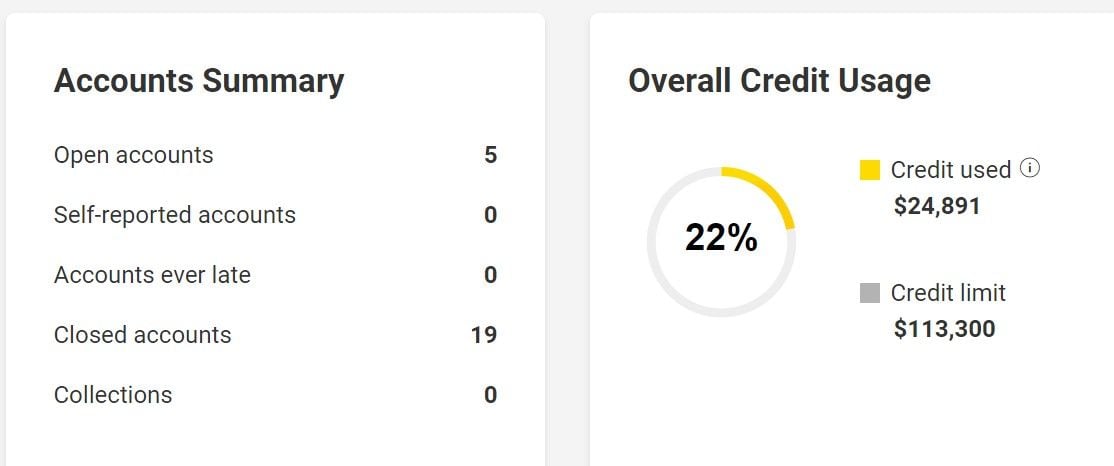

I don't see any negative factor other than 5 inquiries and a little high credit use at 22%.

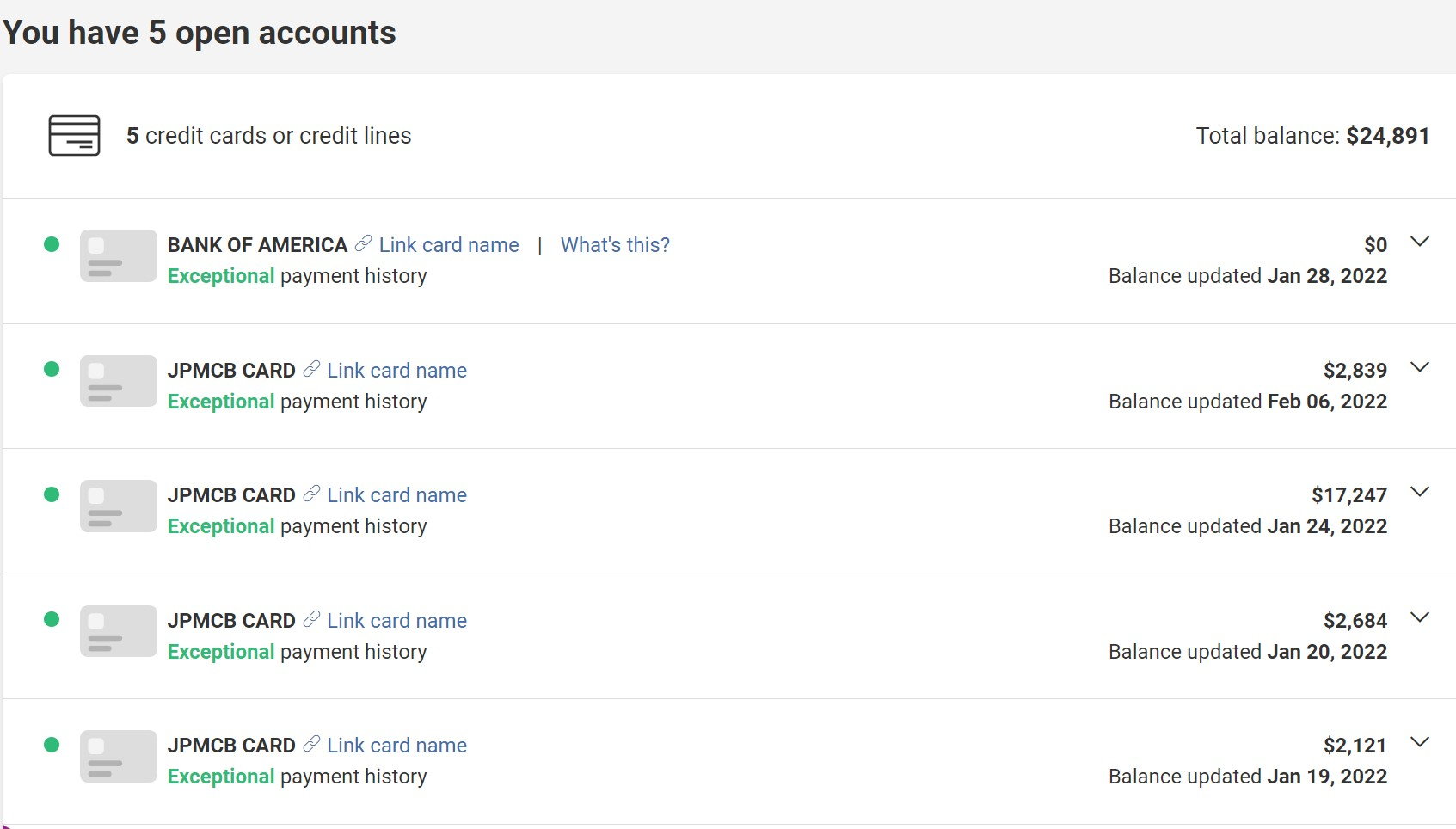

Exceptional payment history is expected because I always pay everything off.

Still surprised by such difference.