Dec 20, 2015, 4:45 am

Dec 20, 2015, 4:45 am

Last edit by: wilsnunn

The FlyerTalk Lending Team on Kiva:

improving lives a small loan at a time.

Kiva.org is the not-for-profit microlending organization that networks people willing to lend to small entrepreneurs in developing nations using available technology and international networking / collaboration, and how Kiva.org had become an approved FlyerTalk charity thanks to TalkBoard's approval June 29, 2008 <link> It is listed on the FlyerTalk Cares page.improving lives a small loan at a time.

"Kiva is a grassroots project started by a team with a big idea: one-to-one, real-time lending to the poor via the Internet. Currently, we take no cut of the loan you make through our site -- 100% goes to the entrepreneur. We suggest a 10% donation, in addition to your loan, to help us cover our costs. Kiva is a 501(c)(3) nonprofit and your donation is tax-deductible for US taxpayers." (Suggested donations for administrative overhead, low though that is, are not required - you may lend 100% if you so choose.)

As of 15 May 2016 it was 607 FlyerTalk lending team who have lent $2,209,175 in 37,092 loans! And now as of 30 June 2019 it is 941 members who have lent $6,415,775 in 71,722 loans!

Our motto is: "We loan because: We want to fight global poverty while earning miles."

This is tangible evidence Flyertalk Cares! There are likely other FlyerTalkers on Kiva who have not joined - if you are one of them, do so now to show your and FT's support and involvement. If you haven't lent yet, check it out - you may want to join up. For the low-income entrepreneurs on five continents who are requesting loans, microlending is significant - and it takes a lot of drops to fill the bucket. (Read on to see updates!)

Now, we can see this sophisticated network link resources from those who can lend (no interest, sorry!) with those who are needy, worthy and screened by local NGOs and have a need to start / expand their small business to enhance their and their families' survival. And, using PayPal and your FFP/FFG linked card or account, you can earn miles or points with many loans!

FlyerTalkers are lending, and fulfilling one of FT's seminal values, that of "paying it forward."

Read more about Kiva.org, who supports and enables it (Intel, Google, Paypal, Intuit and many others,) and see if you have $25.00 (or more) you can lend someone deserving in a land you have visited and enjoyed (or not.)

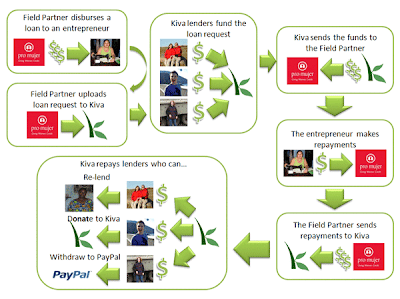

This is how it works:

Add your experiences here, or if you haven't joined... won't you consider joining the FlyerTalker Lending Team?

You can see who the latest FT borrowers are (some still possibly needing loans) here

For ease, you can click here: Subscribe to FlyerTalker Lending Team on Kiva.org

FlyerTalker Lending Team on Kiva.org!

Jan 24, 2013, 6:18 pm

#1066

Join Date: Jan 2004

Location: Louisville, KY, USA

Posts: 2,583

Maybe we need a single non-profit micro finance forum to cover both.

What patience? Us? Well maybe .... sometimes.

Feb 4, 2013, 7:04 pm

Feb 4, 2013, 7:04 pm

#1070

Join Date: May 2010

Posts: 542

Can anyone confirm what interest rate Kiva field partners charge borrowers? I just want to make sure this is not a finance company in disguise for those who can least afford it.

Another poster compared Kiva to Zidisha and implied the Kiva interest rate was 30% or more.

http://saverocity.com/blog/zidisha/

Another poster compared Kiva to Zidisha and implied the Kiva interest rate was 30% or more.

http://saverocity.com/blog/zidisha/

Feb 4, 2013, 7:20 pm

#1071

Join Date: Mar 2010

Location: mountains of western NC

Programs: Life, Love and Laughter

Posts: 8,537

Can anyone confirm what interest rate Kiva field partners charge borrowers? I just want to make sure this is not a finance company in disguise for those who can least afford it.

Another poster compared Kiva to Zidisha and implied the Kiva interest rate was 30% or more.

http://saverocity.com/blog/zidisha/

Another poster compared Kiva to Zidisha and implied the Kiva interest rate was 30% or more.

http://saverocity.com/blog/zidisha/

In my opinion it is totally inappropriate to compare the field partners Kiva works with to lending agencies

One of the primary reasons that Kiva's field partners charge higher interest rates is because they do so much more than just lend money. They provide training, financial counseling, education, a wide variety of social services, help borrowers connect with other borrowers for support and much more. Also, many of these field partners work in remote, impoverished and even war torn areas that no one else will even touch. Kiva's field partners are MUCH MUCH more than lenders. They provide an entire support system. Comparing them to someone who only provides lending is very unrealistic. You wouldn't compare Bank of America to a small, local non-profit community development agency, so Kiva's field partners shouldn't be compared to a lending agencies.

Feb 5, 2013, 8:41 am

#1072

Senior Moderator and Moderator: American AAdvantage & TravelBuzz

Join Date: Nov 2007

Location: BOS

Programs: AA EXP, Marriott Titanium

Posts: 10,417

Team stats as of Dec 17, 2012:

Stats as of 2/5/2013:

Number of Team Members: 367

Number of Loans attributed to this team: 9,926

Total Amount Loaned: $375,450

Looks like we've gotten over 20 new members over the last six weeks! A hearty welcome to you all! ^

(Also looks like we'll soon hit our 10,000th loan for the team! w00t w00t! )

)

Number of Team Members: 344

Number of Loans: 9,021

Total Amount Loaned: $315,700

Number of Loans: 9,021

Total Amount Loaned: $315,700

Number of Team Members: 367

Number of Loans attributed to this team: 9,926

Total Amount Loaned: $375,450

Looks like we've gotten over 20 new members over the last six weeks! A hearty welcome to you all! ^

(Also looks like we'll soon hit our 10,000th loan for the team! w00t w00t!

)

Feb 5, 2013, 9:02 am

#1073

Join Date: Nov 2010

Location: Brooklyn

Programs: AMEX Plat, AAdvantage Gold, UA, SPG Gold, HHonors Gold

Posts: 963

Interest rates vary enormously from field partner to field partner. Each field partner does. And I am sure that interest rates vary from borrower to borrower. That specific information is not available.

In my opinion it is totally inappropriate to compare the field partners Kiva works with to lending agencies

One of the primary reasons that Kiva's field partners charge higher interest rates is because they do so much more than just lend money. They provide training, financial counseling, education, a wide variety of social services, help borrowers connect with other borrowers for support and much more. Also, many of these field partners work in remote, impoverished and even war torn areas that no one else will even touch. Kiva's field partners are MUCH MUCH more than lenders. They provide an entire support system. Comparing them to someone who only provides lending is very unrealistic. You wouldn't compare Bank of America to a small, local non-profit community development agency, so Kiva's field partners shouldn't be compared to a lending agencies.

In my opinion it is totally inappropriate to compare the field partners Kiva works with to lending agencies

One of the primary reasons that Kiva's field partners charge higher interest rates is because they do so much more than just lend money. They provide training, financial counseling, education, a wide variety of social services, help borrowers connect with other borrowers for support and much more. Also, many of these field partners work in remote, impoverished and even war torn areas that no one else will even touch. Kiva's field partners are MUCH MUCH more than lenders. They provide an entire support system. Comparing them to someone who only provides lending is very unrealistic. You wouldn't compare Bank of America to a small, local non-profit community development agency, so Kiva's field partners shouldn't be compared to a lending agencies.

Perhaps the primary reason that Kiva's field partners charge higher interest rates is BECAUSE THEY CAN.

Within the altruism there is abuse.

Not good to hide from it, best to shine a light and clean it up. Kiva is awesome, but flawed, lets make sure that the end user (who we are all trying to help) is not forced into paying these incredible rates of interest.

Awareness and Competition- that is what is needed to push Kiva to the next level.

Disclaimer- I have over 100 active Kiva loans and continue to loan to them.

Feb 5, 2013, 9:06 am

#1074

Join Date: Nov 2010

Location: Brooklyn

Programs: AMEX Plat, AAdvantage Gold, UA, SPG Gold, HHonors Gold

Posts: 963

Can anyone confirm what interest rate Kiva field partners charge borrowers? I just want to make sure this is not a finance company in disguise for those who can least afford it.

Another poster compared Kiva to Zidisha and implied the Kiva interest rate was 30% or more.

http://saverocity.com/blog/zidisha/

Another poster compared Kiva to Zidisha and implied the Kiva interest rate was 30% or more.

http://saverocity.com/blog/zidisha/

Under outside pressure, LAPO announced in 2009 that it was decreasing its monthly interest rate, Planet Rating noted, but at the same time compulsory savings were quietly raised to 20 percent of the loan from 10 percent. So, the effective interest rate for some clients actually leapt to nearly 126 percent annually from 114 percent, the report said. The average for all LAPO clients was nearly 74 percent in interest and fees, the report found.

Anita Edward says she has borrowed money three times from LAPO for her hair salon, Amazing Collections, in Benin City, Nigeria. The money comes cheaper than other microloans, and commercial banks are virtually impossible, she said, but she resents the fact that LAPO demanded that she keep $100 of her roughly $666 10-month loan in a savings account while she paid interest on the full amount.

�That is not O.K. by me,� she said. �It is not fair. They should give you the full money.�

The loans from LAPO helped her expand from one shop to two, but when she started she thought she would have more money to put into the business.

�It has improved my life, but not changed it,� said Ms. Edward, 30.

Godwin Ehigiamusoe, LAPO�s founding executive director, defended his company�s high interest rates, saying they reflected the high cost of doing business in Nigeria. For example, he said, each of the company�s more than 200 branches needed its own generator and fuel to run it.

Until recently, Microplace, which is part of eBay, was promoting LAPO to individual investors, even though the Web site says the lenders it features have interest rates between 18 and 60 percent, considerably less than what LAPO customers typically pay.

As recently as February, Microplace also said that LAPO had a strong rating from Microrate, yet the rating agency had suspended LAPO the previous August, six months earlier. Microplace then removed the rating after The New York Times called to inquire why it was still being used and has since taken LAPO investments off the Web site.

At Kiva, which promises on its Web site that it �will not partner with an organization that charges exorbitant interest rates,� the interest rate and fees for LAPO was recently advertised as 57 percent, the average rate from 2007. After The Times called to inquire, Kiva changed it to 83 percent.

Premal Shah, Kiva�s president, said it was a question of outdated information rather than deception. �I would argue that the information is stale as opposed to misleading,� he said. �It could have been a tad better.�

While analysts characterize such microfinance Web sites as well-meaning, they question whether the sites sufficiently vetted the organizations they promoted.

Questions had already been raised about Kiva because the Web site once promised that loans would go to specific borrowers identified on the site, but later backtracked, clarifying that the money went to organizations rather than individuals.

Promotion aside, the overriding question facing the industry, analysts say, remains how much money investors should make from lending to poor people, mostly women, often at interest rates that are hidden.

�You can make money from the poorest people in the world � is that a bad thing, or is that just a business?� asked Mr. Waterfield of mftransparency.org. �At what point do we say we have gone too far?�

Note - Kiva is not robbing you here, they are just working with some folk that are.

Full article: http://www.nytimes.com/2010/04/14/wo...ewanted=3&_r=0

Feb 5, 2013, 10:21 am

#1075

Join Date: Mar 2010

Location: mountains of western NC

Programs: Life, Love and Laughter

Posts: 8,537

Which one is the Bank of America in your analogy? I got confused?

Perhaps the primary reason that Kiva's field partners charge higher interest rates is BECAUSE THEY CAN.

Within the altruism there is abuse.

Not good to hide from it, best to shine a light and clean it up. Kiva is awesome, but flawed, lets make sure that the end user (who we are all trying to help) is not forced into paying these incredible rates of interest.

Awareness and Competition- that is what is needed to push Kiva to the next level.

Disclaimer- I have over 100 active Kiva loans and continue to loan to them.

Perhaps the primary reason that Kiva's field partners charge higher interest rates is BECAUSE THEY CAN.

Within the altruism there is abuse.

Not good to hide from it, best to shine a light and clean it up. Kiva is awesome, but flawed, lets make sure that the end user (who we are all trying to help) is not forced into paying these incredible rates of interest.

Awareness and Competition- that is what is needed to push Kiva to the next level.

Disclaimer- I have over 100 active Kiva loans and continue to loan to them.

I seriously doubt that the Bank of America is deserving of any social performance badges.

If you or any Kiva lender is concerned about interest rates, both the kiva.org/lend page and kivalens.org provide easy way to screen loans according to interest rates and amount of profit the field partners are making. On Kiva.org/lend, scroll down the left column and then click on advanced options. Then you will be shown these ways to screen your loans. Of course, you can also check field partner's interest rates and profitability on any individual loan.

But if you really want to understand what it is like for these field partners to operate, then I strongly recommend that you read some of the stories from the field. I also used to be very concerned about high interest rates (my father had a mortgage lending business, so I have a lifelong history with this issue) until I read some of the stories. Since then I've been amazed that interest rates are so low compared to the difficulties these field partners must face.

A good place to read some of these stories:

http://fellowsblog.kiva.org/

A couple of years ago some Flyertalkers helped Lina Goldberg get to Cambodia for her stint as a Kiva fellow. Some of her stories are here:

http://linakiva.blogspot.com/

Feb 5, 2013, 11:08 am

#1076

Join Date: Mar 2010

Location: mountains of western NC

Programs: Life, Love and Laughter

Posts: 8,537

A few more thoughts on "high' interest rates.

Please keep in mind that one of the reasons Kiva was founded and is continually growing is because of its dedication to providing loans to people who have little or no access to capital.

Many borrowers live in remote areas without phones, internet or good roads. Sometimes it can take field partner staff an entire day to visit one or two borrowers for assessment, due diligence, training etc. Is this cost effective? Of course not. But how else do you reach those who really need the loans?

What about field partners who are in war torn countries like Afghanistan, Iraq, Mali, Sierra Leone and others? Should they abandon their borrowers because it's not cost effective or safe to provide services and loans to them?

What about borrowers who have never been in business for themselves before? What if it takes weeks/months of training and education to properly prepare them to launch their business? Don't they deserve opportunities, too?

What if the field partner works in a country whose laws, culture, infrastructure etc. are not supportive of entrepreneurship?

What if the field partner has to provide many services which we in the developed world take for granted?

I could go on and on with examples. But the question remains should Kiva and Kiva field partners really try to reach those who are very difficult to reach or should they cut back and just provide loans to those who can safely and easily be reached (and thus keep interest rates low)?

And if a region or village is dominated by private lenders whose rates are 200-300% should Kiva's field partners not provide loans at 50%, just because we in the developed world can get loans at 5%?

And if these field partner's rates are so high (compared to what other lender's rates are), then why are the borrowers so happy to receive these loans?

And why are they paying them back more than 99% of the time?

I totally understand that Kiva is a flawed organization and so are all of its field partners. Mistakes are made all the time. But for me the real question is are Kiva and its field partners providing a real service for these borrowers?

And if these field partners did not exist, what are these borrowers alternatives? I don't like 50% interest rates. But they are a hell of a lot better than 200% interest rates.

Please keep in mind that one of the reasons Kiva was founded and is continually growing is because of its dedication to providing loans to people who have little or no access to capital.

Many borrowers live in remote areas without phones, internet or good roads. Sometimes it can take field partner staff an entire day to visit one or two borrowers for assessment, due diligence, training etc. Is this cost effective? Of course not. But how else do you reach those who really need the loans?

What about field partners who are in war torn countries like Afghanistan, Iraq, Mali, Sierra Leone and others? Should they abandon their borrowers because it's not cost effective or safe to provide services and loans to them?

What about borrowers who have never been in business for themselves before? What if it takes weeks/months of training and education to properly prepare them to launch their business? Don't they deserve opportunities, too?

What if the field partner works in a country whose laws, culture, infrastructure etc. are not supportive of entrepreneurship?

What if the field partner has to provide many services which we in the developed world take for granted?

I could go on and on with examples. But the question remains should Kiva and Kiva field partners really try to reach those who are very difficult to reach or should they cut back and just provide loans to those who can safely and easily be reached (and thus keep interest rates low)?

And if a region or village is dominated by private lenders whose rates are 200-300% should Kiva's field partners not provide loans at 50%, just because we in the developed world can get loans at 5%?

And if these field partner's rates are so high (compared to what other lender's rates are), then why are the borrowers so happy to receive these loans?

And why are they paying them back more than 99% of the time?

I totally understand that Kiva is a flawed organization and so are all of its field partners. Mistakes are made all the time. But for me the real question is are Kiva and its field partners providing a real service for these borrowers?

And if these field partners did not exist, what are these borrowers alternatives? I don't like 50% interest rates. But they are a hell of a lot better than 200% interest rates.

Feb 5, 2013, 2:30 pm

#1077

Join Date: Nov 2010

Location: Brooklyn

Programs: AMEX Plat, AAdvantage Gold, UA, SPG Gold, HHonors Gold

Posts: 963

A few more thoughts on "high' interest rates.

Please keep in mind that one of the reasons Kiva was founded and is continually growing is because of its dedication to providing loans to people who have little or no access to capital.

Many borrowers live in remote areas without phones, internet or good roads. Sometimes it can take field partner staff an entire day to visit one or two borrowers for assessment, due diligence, training etc. Is this cost effective? Of course not. But how else do you reach those who really need the loans?

What about field partners who are in war torn countries like Afghanistan, Iraq, Mali, Sierra Leone and others? Should they abandon their borrowers because it's not cost effective or safe to provide services and loans to them?

What about borrowers who have never been in business for themselves before? What if it takes weeks/months of training and education to properly prepare them to launch their business? Don't they deserve opportunities, too?

What if the field partner works in a country whose laws, culture, infrastructure etc. are not supportive of entrepreneurship?

What if the field partner has to provide many services which we in the developed world take for granted?

I could go on and on with examples. But the question remains should Kiva and Kiva field partners really try to reach those who are very difficult to reach or should they cut back and just provide loans to those who can safely and easily be reached (and thus keep interest rates low)?

And if a region or village is dominated by private lenders whose rates are 200-300% should Kiva's field partners not provide loans at 50%, just because we in the developed world can get loans at 5%?

And if these field partner's rates are so high (compared to what other lender's rates are), then why are the borrowers so happy to receive these loans?

And why are they paying them back more than 99% of the time?

I totally understand that Kiva is a flawed organization and so are all of its field partners. Mistakes are made all the time. But for me the real question is are Kiva and its field partners providing a real service for these borrowers?

And if these field partners did not exist, what are these borrowers alternatives? I don't like 50% interest rates. But they are a hell of a lot better than 200% interest rates.

Please keep in mind that one of the reasons Kiva was founded and is continually growing is because of its dedication to providing loans to people who have little or no access to capital.

Many borrowers live in remote areas without phones, internet or good roads. Sometimes it can take field partner staff an entire day to visit one or two borrowers for assessment, due diligence, training etc. Is this cost effective? Of course not. But how else do you reach those who really need the loans?

What about field partners who are in war torn countries like Afghanistan, Iraq, Mali, Sierra Leone and others? Should they abandon their borrowers because it's not cost effective or safe to provide services and loans to them?

What about borrowers who have never been in business for themselves before? What if it takes weeks/months of training and education to properly prepare them to launch their business? Don't they deserve opportunities, too?

What if the field partner works in a country whose laws, culture, infrastructure etc. are not supportive of entrepreneurship?

What if the field partner has to provide many services which we in the developed world take for granted?

I could go on and on with examples. But the question remains should Kiva and Kiva field partners really try to reach those who are very difficult to reach or should they cut back and just provide loans to those who can safely and easily be reached (and thus keep interest rates low)?

And if a region or village is dominated by private lenders whose rates are 200-300% should Kiva's field partners not provide loans at 50%, just because we in the developed world can get loans at 5%?

And if these field partner's rates are so high (compared to what other lender's rates are), then why are the borrowers so happy to receive these loans?

And why are they paying them back more than 99% of the time?

I totally understand that Kiva is a flawed organization and so are all of its field partners. Mistakes are made all the time. But for me the real question is are Kiva and its field partners providing a real service for these borrowers?

And if these field partners did not exist, what are these borrowers alternatives? I don't like 50% interest rates. But they are a hell of a lot better than 200% interest rates.

I agree they are doing great work, but is someone getting too big a slice of the pie over there? That is the thing to keep an eye on.

Don't forget, all that stuff about their extra duties and educating in the field:

1. Does not apply to all borrowers - one guy I just lent to on Zidisha has an MBA and a business already, he knows what he wants and needs a capital injection. He doesn't need a 50% interest rate and a story about how much good work the field partners are doing, he needs liquidity in lending at a competitive rate.

2. We aren't assessing the waste in this, we are making an excuse for whatever high number they give us rather than drill down.

So, my take on it is lets give to Kiva, lets give to Zidisha, lets pressure and educate about any potential exploitation of our altruistic efforts and make sure that the people we care about (the borrowers) get a fair deal, not a 'this is the best your gonna get' deal.

In ways I feel bad about talking like this on here since I don't want to discourage people from giving, but it is clear that many folk don't know about this factor and it shouldn't be glossed over.

Feb 6, 2013, 4:12 pm

#1079

Join Date: Mar 2010

Location: mountains of western NC

Programs: Life, Love and Laughter

Posts: 8,537

Feb 7, 2013, 6:38 am

#1080

Join Date: Jan 2004

Location: Louisville, KY, USA

Posts: 2,583

With over 1200 loans, I have had two partially repaid loans default. My default rate is just 0.16% meaning my payback has been 99.84%.

Kiva's delinquency rate is 2.48%. Mine is slightly higher but many of my loans are less than $1 behind. Usually delinquencies improve as the month nears the end and those a few days late get their dollars in.

Kiva's delinquency rate is 2.48%. Mine is slightly higher but many of my loans are less than $1 behind. Usually delinquencies improve as the month nears the end and those a few days late get their dollars in.